Safety Switch Market: Growth Opportunities and Forecast

Other |

2026-07-08 09:30:24

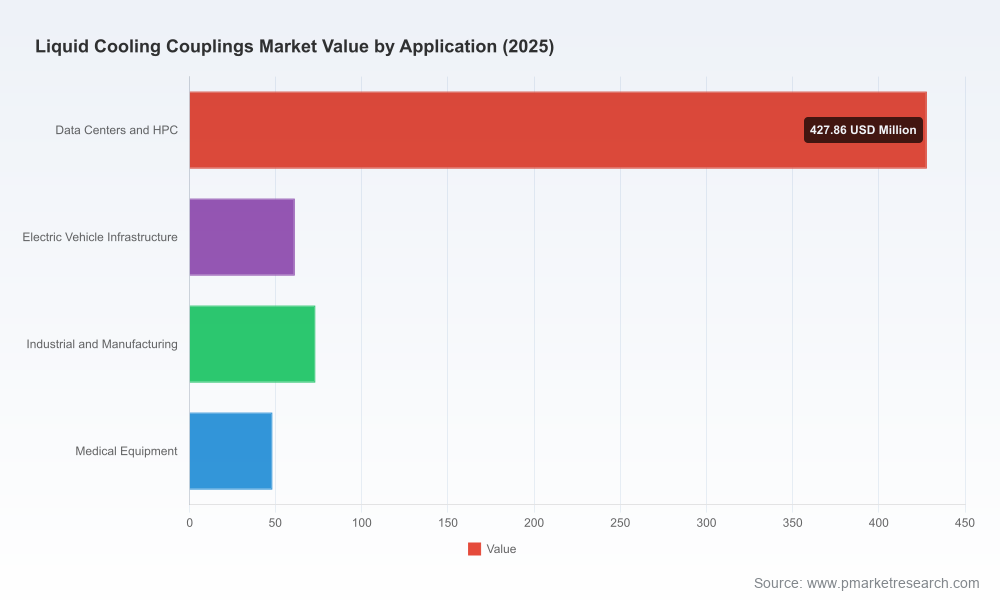

PW Consulting’s newest market study on Worldwide Liquid Cooling Couplings establishes a clear, actionable roadmap for enterprises planning thermal‑management investments in 2026 and beyond. The market has moved from a niche operational concern to a strategic infrastructure lever: our analysis values the market at USD 610.15 Million in the base year (2025) and models a rapid expansion at a compound annual growth rate (CAGR) of 18.52% through the forecast window. By 2032, the market is expected to exceed USD 2.0 Billion under the central scenario. These headline numbers are only the starting point—this report is designed to transform headline growth into concrete decisions for sourcing, product development, test & validation, and M&A strategy.

Worldwide Liquid Cooling Couplings Market

Enterprises face three converging pressures that elevate liquid cooling couplings from component selection to strategic risk and opportunity:

Worldwide Liquid Cooling Couplings Market

This study goes beyond high‑level forecasting. It is a decision‑grade toolkit for procurement teams, system architects, and corporate strategists. Key practical deliverables include:

Worldwide Liquid Cooling Couplings Market

The market shows mounting consolidation at the top: the combined share of the three largest vendors reflects a meaningful concentration that affects pricing dynamics, design influence on standards, and supplier negotiation leverage. Our CR3 and CR5 concentration metrics underscore that strategic supplier engagement—and contingency planning—are not optional. The report provides a vendor matrix that maps commercial, technical and standards positions for manufacturers active in liquid cooling couplings.

Highlights from our vendor intelligence:

Vendor product launches, show calendar activity, and the OCP UQD v2 release have reshaped supplier selection criteria over the past 12 months. Notable developments captured in the report include Stäubli’s late‑2025 Mini‑QD launch and its role in the UQD v2 update; CPC’s strategic presence at major industry events to showcase Everis UQD systems; Parker’s mid‑2025 product advancements aligned to OCP; and Danfoss’s regional engagements on data center thermal solutions. These events matter because they accelerate interoperability testing and shorten qualification cycles for early adopters.

From a component engineering perspective, common practice relies on stainless steels (303/304) and elastomeric seals such as EPDM to balance corrosion resistance and coolant compatibility. The report translates these raw‑material realities into procurement tactics: long‑lead agreements for high‑grade stainless, dual‑sourcing strategies for critical elastomers, and inventory policies that reflect the higher throughput and failure‑mode costs of liquid‑cooled environments.

Our analysis yields five prioritized actions for enterprises moving from pilots to production scale in 2026:

The report provides tailored playbooks for four archetypal buyers—hyperscalers and cloud providers, enterprise data centers upgrading for AI loads, colocation operators, and OEMs building server trays and CDUs. Each playbook outlines procurement timelines, validation budgets, and the minimal set of interoperability tests required to move from pilot to production. We also offer an executive dashboard that quantifies the marginal ROI of transitioning from air cooling to direct liquid architectures when coupling reliability and maintenance windows are modeled explicitly.

Many market studies stop at sizing and growth trajectories. PW Consulting’s study is engineered to be operational: we deliver a dynamic forecast model, supplier engagement templates, and test matrices that teams can adopt directly within procurement and engineering workflows. Our primary research spans supplier interviews, lab accreditation sources, and event intelligence gathered from 2024–2026 trade activity, resulting in practical, executable guidance rather than abstract prescriptions.

For teams tasked with deployment planning in 2026, the immediate priorities are supplier qualification and standard compliance. PW Consulting’s report equips decision‑makers to accelerate these steps while protecting operational availability and capital efficiency. The full study includes downloadable models, editable RFP templates, and a gated vendor database with granular scoring—data intentionally omitted here to preserve the value of the primary research and to direct practitioners to the full deliverable for procurement and engineering use.

PW Consulting is publishing the full report and accompanying toolkits through our research portal. Corporations, system integrators, and component manufacturers preparing for scaled liquid cooling deployments will find the report’s combination of market forecasting, supplier analysis, test protocols, and tactical playbooks indispensable for 2026 planning cycles.

For detailed analysis of this topic, please visit the official page:Worldwide Liquid Cooling Couplings Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com