Cellulose Fibers Market Industry Expansion and Outlook

Other |

2026-05-22 12:33:12

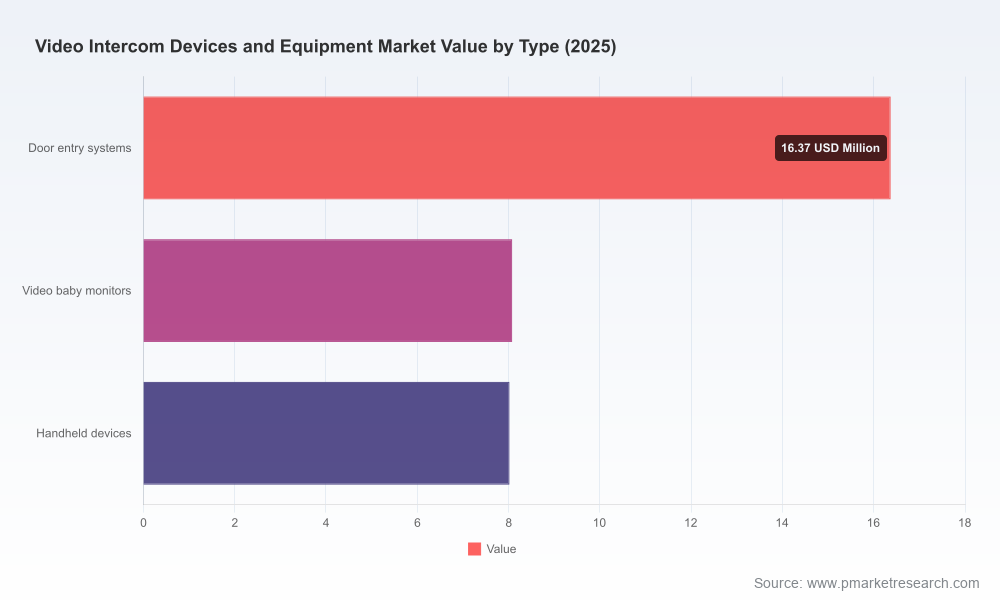

PW Consulting’s new market intelligence brief offers a high‑value executive preview of the Video Intercom Devices and Equipment Market, framed to support boardroom decisions and investment priorities heading into 2026. Built on a base year of 2025 and a historical dataset covering 2020–2025, our analysis quantifies a robust growth trajectory — the market expands at a compound annual growth rate (CAGR) of 12.45% through the forecast window (2026–2032). To illustrate scale: the global market grew from an estimated USD 18.06 million in 2020 to USD 32.47 million in 2025, and PW Consulting’s model projects continued acceleration toward the end of the forecast, signaling a materially larger market by 2032.

Video Intercom Devices and Equipment Market

Capital allocation: Procurement officers and CFOs need a concise picture of adoption curves and total addressable market growth to prioritize CAPEX vs. OPEX investments in access control and tenancy management systems.

Video Intercom Devices and Equipment Market

Product roadmap alignment: Vendors must reconcile AI, cloud, and low‑power design pathways against evolving regulations and data‑center energy constraints to preserve margins and meet buyer requirements.

Video Intercom Devices and Equipment Market

M&A and partnerships: Investors and corporate development teams require a defensible view of market concentration, competitive moats, and whitespace — not only to value targets, but to structure integration plays.

Market sizing and validated demand curves (base year 2025; historical 2020–2025; forecast 2026–2032), with scenario modelling that stress‑tests adoption under alternative macroeconomic and regulatory assumptions.

Go‑to‑market playbooks for vendor and integrator segments, including channel enablement, pricing frameworks, and three archetypal buyer journeys (residential, commercial, multi‑tenant).

Technology roadmaps for device OEMs and platform providers addressing AI inferencing at the edge, cloud orchestration, and secure firmware lifecycles.

Total cost of ownership (TCO) models and procurement scorecards that quantify, for any deployment size, the tradeoffs between on‑prem, hybrid, and fully cloud‑native intercom architectures.

Regulatory impact scenarios and compliance playbooks covering U.S. federal procurement constraints, European energy‑reporting mandates, and state‑level data‑center energy rules.

Competitive diagnostic with vendor scorecards, capability matrices, and a prioritized list of strategic bets for incumbents and challengers.

Risk matrices and mitigation strategies covering supply‑chain volatility, components pricing, and cyber‑supply‑chain exposure.

Cloud and SaaS adoption: The market continues its migration toward cloud‑managed intercom platforms that reduce on‑site maintenance and enable centralized tenant and facilities workflows. This shift affects procurement models (subscription vs. capital purchase), drives demand for resilient connectivity, and places a premium on vendor cloud SLAs.

AI and embedded intelligence: AI‑driven features — from voice and video analytics to automated visitor verification and deterrence — are becoming table stakes for higher‑end deployments. Our forecast accounts for rapid uptake of selective AI features that materially increase average selling prices for platform subscriptions and advanced devices.

Regulatory pressure and compliance costs: Policy changes are already re‑shaping procurement and sourcing strategies. For example, recent U.S. procurement rules restrict certain vendors from federal projects, and European energy reporting requirements for data centers impose new operational overheads for cloud providers that support intercom services. State‑level legislation addressing data‑center energy sourcing further complicates vendor cost models.

Component cost volatility: Downstream device economics are sensitive to commodity swings. Our sector analysis finds fluctuations in LCD panels, camera modules, and plastics driving component cost variability in the mid‑teens on a periodic basis — a non‑trivial risk for fixed‑price contracts and thin‑margin hardware lines.

Market concentration: Competition is moderate — the three largest players do not dominate the entirety of demand, and the top five collectively hold a meaningful, but not prohibitive, share. This structure creates room for both scale advantages and nimble challengers.

The market is rich with diversified vendor archetypes: established industrial OEMs, cloud‑native disruptors, surveillance platform integrators, and specialized access control firms. Below are strategic profiles of companies that exemplify the major competitive vectors.

Aiphone (Nagoya): A heritage intercom manufacturer modernizing through cloud management and IP‑native product lines that target multi‑tenant commercial deployments with remote administration capabilities.

ButterflyMX (Denver): A cloud‑first challenger with mobile‑centric UX and simplified installation models that have gained traction in multifamily and retrofit commercial projects.

Verkada (San Francisco): Integrates cameras, access control, and AI features into a single platform; recent product updates add advanced voice translation and AI deterrence capabilities, underscoring the convergence of security and communications functionality.

AXIS (Lund): Leverages deep expertise in network video to offer IP intercoms optimized for integration into broader security architectures.

European specialists — companies such as DoorBird, 2N, Comelit, and Zenitel — emphasize SIP or IP interoperability and are often selected in projects where voice quality, integration standards, or critical communications are priorities.

Large surveillance OEMs — regional heavyweights with end‑to‑end surveillance and access portfolios continue to field competitively priced intercom offerings, but face procurement headwinds in certain geographies due to regulatory constraints.

Specialist integrators and audio/video firms — firms focused on broadcast, event, and campus communications provide differentiated matrix and wireless intercom systems tailored to professional use cases.

Enterprise vendors continue to layer AI into intercom experiences — product updates launched in early 2026 introduce live translation and AI directories that reduce friction in mixed‑language environments.

Integration‑centric upgrades — such as modules that enable third‑party access control compatibility — are emerging, signaling that interoperability is a key procurement criterion for building operators.

Cloud‑mobile offerings for multi‑tenant properties continue to expand the addressable market by lowering installation complexity and enabling remote management at scale.

For buyers: Adopt a compliance‑first procurement scorecard that integrates regulatory exposure, cloud energy impact, and TCO under multiple scenarios. Negotiate pricing clauses that hedge for component‑cost swings and require clear firmware update commitments.

For vendors: Prioritize cloud economics and flexible licensing while investing in lightweight edge AI that reduces bandwidth and cloud compute fees. Build interoperability toolkits to accelerate enterprise integrations.

For investors and M&A teams: Focus on targets that combine software recurring revenue with hardware synergies — companies that can move customers from device sales to subscription platforms will command premium multiples.

For integrators and channel partners: Expand service bundles around lifecycle management and compliance reporting to capture new recurring revenue streams as customers shift to managed models.

PW Consulting’s full study synthesizes primary interviews, vendor financials, transaction data, component cost indices, and regulatory texts. The brief above highlights directional insights and strategic recommendations; however, consistent with our “trailer” approach, we have intentionally omitted granular regional, type‑level, and application‑level splits from this press release. These subsegment tables, provider scorecards and downloadable Excel models are included in the flagship report and the associated client deliverables.

Decision‑makers preparing capital plans or go‑to‑market strategies for 2026 should engage PW Consulting for a tailored briefing. Our full report delivers the detailed splits, vendor benchmarking, and executable playbooks referenced above — the operational intelligence your procurement, product, and M&A teams will depend on to act with conviction.

To request the complete report or schedule a bespoke executive workshop, please contact PW Consulting’s Industry Practice. The detailed models and vendor matrices are available to subscribing clients and will materially shorten your path from insight to implementation.

For detailed analysis of this topic, please visit the official page:Video Intercom Devices and Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com