Bluetooth Audio IC Market Outlook 2026: Strategic Imperatives from PW Consulting’s New Market Study

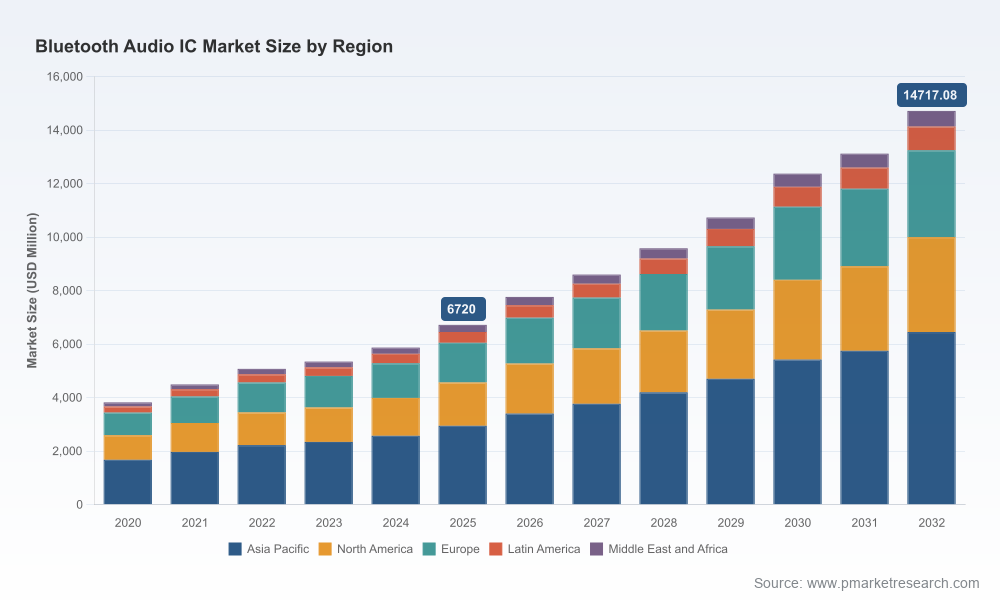

PW Consulting’s latest Bluetooth Audio IC Market report (base year 2025; forecast 2026–2032) provides a decision-grade view for executives planning investments, product roadmaps, and supply-chain reconfigurations in 2026. The study traces an established growth trajectory—anchored by a compound annual growth rate (CAGR) of 11.85%—and quantifies the transition of the market into a multi-billion-dollar opportunity. This release is a strategic “preview trailer”: it surfaces high-confidence signals, risk vectors, and actionable playbooks while intentionally withholding the granular split tables that drive transactional decisions. Readers seeking the complete datasets, model assumptions, and downloadable appendices are invited to access the full report on our website.

Bluetooth Audio Ic Market

Market Trajectory: What the Macros Tell Us

The Bluetooth audio IC market is entering a phase of structural expansion driven by new wireless audio standards, rising premiumization of hearables, and the steady upgrade cycle in smart consumer audio devices. Our model shows the market consolidating around multi-billion-dollar revenue levels by the 2025 base year and accelerating into 2026, consistent with an 11.85% CAGR over the forecast window. That growth is not uniform—technology inflections (LE Audio, LC3), product consolidation (dual-mode ICs), and adjacent demand from automotive and smart-home ecosystems create pockets of higher-than-average expansion that are covered in depth in the full report.

Bluetooth Audio Ic Market

Why This Matters for 2026 Decision-Makers

- Capital allocation and product prioritization: With sustained double-digit CAGR, R&D and capex decisions made in 2026 will materially affect market share through 2030. Firms that prioritize LE Audio and dual-mode roadmaps will be better positioned to capture the premium segment.

- Supplier and contract strategies: Longer design cycles and lead-time normalization for mature nodes require procurement teams to re-evaluate multi-year supply arrangements and qualification timelines.

- M&A and partnership timing: The market concentration metrics indicate meaningful scale benefits; selective acquisitions and strategic partnerships can accelerate route-to-market for advanced codecs and IP.

Competitive Landscape: Who Matters and Why

The market remains oligopolistic at the technology-leading tiers while still offering differentiated entry points for regional specialists. PW Consulting’s competitive assessment combines product roadmaps, silicon IP strengths, go-to-market capabilities, and recent execution signals to produce a pragmatic view for 2026 planning.

Bluetooth Audio Ic Market

- Qualcomm (San Diego, CA, USA) — Retains leadership through high-performance SoC families and broad ecosystem initiatives (e.g., Snapdragon Sound and aptX variants). Recent launches expanding LE Audio and Matter support signal a concerted push into IoT audio verticals.

- Realtek Semiconductor (Hsinchu, Taiwan) — Competes on price/performance and integration for mass-market TWS and consumer audio, with strong relationships across Asian OEMs.

- Airoha Technology (Zhubei City, Taiwan) — Focused on premium TWS silicon with AI-enabled ANC and Ultra-Low Latency capabilities; certification wins indicate traction in higher-margin segments.

- BES Technic (Shanghai, China) — Advances on audio fidelity and power optimization; product samplings for ultra-low-power chips point to wearables and long-run-time hearables demand.

- Nordic Semiconductor (Trondheim, Norway) — Strategically positioned around LE Audio adoption and LC3 codec enablement; strong IP for low-power designs used in hearables and smart speakers.

- Espressif Systems (Shanghai, China) — Competes where embedded Wi‑Fi/Bluetooth integration delivers differentiated price-performance for IoT audio devices.

- Texas Instruments (Dallas, TX, USA) & STMicroelectronics (Geneva, Switzerland) — Playbooks centered on industrial-grade integration, low-power audio processing, and cross-domain silicon reuse for gateways and automotive applications.

These vendor profiles—and a sanitized supplier scorecard—are included in the public summary. The full competitive appendix in the report includes capability heat maps, product-to-application fit matrices, and scenario-based supplier tiering that are essential for sourcing, product management, and corporate development teams.

Recent Industry Signals: Tactical Inputs for 2026

- Product rollouts and samplings across multiple vendors demonstrate the market’s pivot to LE Audio and related features (e.g., Matter connectivity). Notable examples are new SoC introductions and sampling programs from major and regional players.

- Standard and ecosystem shifts—Bluetooth 5.4 and the LC3 codec—are already altering design requirements and bandwidth/quality trade-offs.

- Supply-chain and geopolitical headwinds persist: export controls, tariff regimes, and equipment restrictions are reshaping risk profiles for RF IC sourcing and qualification timelines.

- Manufacturing node dynamics have stabilized lead times for mature CMOS processes, but capacity competition for specialty nodes and packaging remains a near-term constraint.

Strategic Playbook for 2026: Recommendations by Function

Below are high-conviction moves for different enterprise roles. These recommendations prioritize optionality, speed to market, and defensible positioning given the market’s projected growth and concentration trends.

- For Chipmakers

- Prioritize dual-mode and LC3-capable IP to address both legacy device compatibility and LE Audio adoption waves.

- Invest in cross-license and software ecosystems (codec stacks, ANC frameworks) to raise switching costs for OEMs.

- Secure long-lead manufacturing capacity and diversify packaging/OSAT partners to mitigate single-point supply risks.

- For OEMs and ODMs

- Adopt modular reference designs and maintain parallel qualification tracks for at least two silicon suppliers to avoid supplier-driven bottlenecks.

- Differentiate via UX and ecosystem interoperability (shareability, multi-device audio), not just raw codec claims.

- Use PW Consulting’s scenario cost-models to stress-test ASP resilience under faster-than-expected premiumization.

- For Component Suppliers & OSATs

- Target services that accelerate qualification (turnkey RF test benches, pre-certified modules), since time-to-market is now a strategic lever.

- Prioritize certification support (Bluetooth SIG, regulatory) as a value-add for smaller OEMs.

- For Investors and Corporate Development

- Lean into M&A opportunities that deliver complementary IP (e.g., codec patents, ANC algorithms) and steady OEM relationships.

- Evaluate bolt-on acquisitions where integration timelines are sub-12 months; look for technology scarcity rather than volume plays.

Risk Matrix: What Keeps Us Up at Night

Risk is asymmetric across technical, regulatory, and commercial vectors. Principal risks highlighted in the report include:

- Regulatory and trade restrictions that could re-route supply chains and increase landed costs.

- Standards fragmentation and multi-codec complexity that inflate BOM and integration labor.

- Concentrated market share among top suppliers creating pricing and feature-leverage risks for smaller players.

- Potential bottlenecks in packaging and test capacity for audio-grade RF solutions during peak adoption cycles.

What’s Inside the Full Report (Practical, Executable Content)

PW Consulting’s full study is engineered for immediate operationalization by product leaders, procurement heads, and M&A teams. Key deliverables include:

- Financial-grade market model (2020–2032) with baseline/alternative scenarios and sensitivity levers for ASP, adoption rates, and node constraints.

- Playbooks for silicon selection, integration timelines, and supplier qualification with templated RF test plans.

- Competitive matrices mapping product features to application fit, and vendor SWOTs with programmatic recommendations.

- Risk/mitigation frameworks covering regulatory, supply chain, and standards-related exposures with prioritized countermeasures.

- Investor-oriented M&A screens, valuation comparables, and integration checklists for tuck-in and scale-up opportunities.

Conclusion: How PW Consulting’s Insights Should Shape Your 2026 Agenda

The Bluetooth audio IC market’s growth profile—supported by an 11.85% CAGR and a multi-billion-dollar revenue base—creates a narrow window in 2026 to lock in technological differentiation and supply resilience. Firms that combine selective capex, strategic supplier diversification, and software-enabled differentiation will capture disproportionate upside. Conversely, delaying investments in LE Audio readiness, ecosystem integrations, or supplier qualification will translate into longer-term share loss and margin pressure.

This article is a high-level briefing designed to orient corporate leaders and investors. For the precise datasets, segmented forecasts, supplier scorecards, and the executable templates referenced above, please consult the full PW Consulting Bluetooth Audio IC Market report available on our website. The comprehensive appendices contain the granular splits, model drivers, and downloadable tools necessary to operationalize strategy in 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Bluetooth Audio Ic Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com