OpenStack Service Market 2026: Strategic Priorities for Decisions that Scale

As PW Consulting’s Senior Strategy Advisor and Head Industry Analyst, I am pleased to introduce our latest market brief — the OpenStack Service Market 2026 Research Report. In an era where infrastructure strategy is increasingly the fulcrum of competitive advantage, this study synthesizes market dynamics, vendor positioning, operational playbooks, and scenario-driven forecasts to equip CIOs, cloud architects, and procurement leaders with the context they need to act in 2026.

Openstack Service Market

Market snapshot: momentum, scale, and the next growth phase

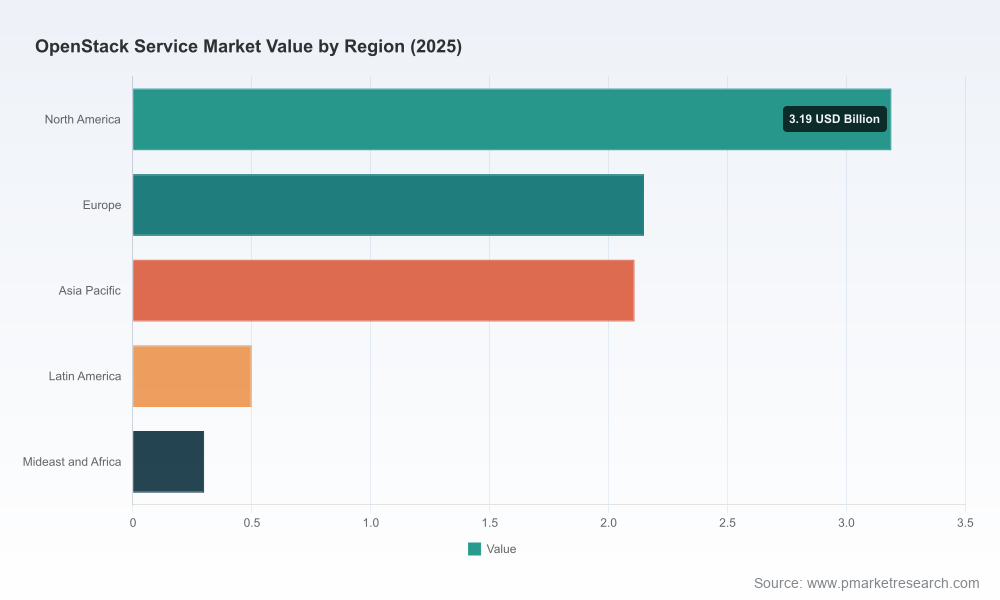

OpenStack services have moved beyond niche experiments to a measurable market with broad commercial traction. Our analysis, using 2025 as the base year, documents a recovery and growth trajectory: the market grew from approximately USD 4.8 billion in 2020 to USD 8.25 billion in 2025 and is projected to continue expanding at a compound annual growth rate (CAGR) of 10.78% through our forecast window (2026–2032). By 2032 the market is expected to approach USD 16.9 billion, driven by renewed interest in open-source private/hybrid stacks, edge-enabled architectures, and migration projects that prioritize control and cost predictability.

Openstack Service Market

Concentration metrics indicate a moderately fragmented vendor landscape: the top three vendors account for a meaningful but not overwhelming share of revenue (CR3 ~35.4%), while the top five approach parity with larger legacy cloud partners (CR5 ~46.2%). This structure fosters competitive services innovation while leaving room for specialized providers to capture vertical or regional niches.

Openstack Service Market

Why this report matters for 2026 decision-making

- Decision framing under uncertainty: The report translates macro growth and adoption signals into decision-ready frameworks — when to buy managed services versus in-house build, how to size phased migration programs, and how to prioritize investment across private, hybrid and edge deployments.

- Vendor selection that mitigates risk: We provide comparative service archetypes and negotiation playbooks tailored to 2026 commercial terms, security expectations, and operational SLAs — enabling procurement teams to compress vendor evaluation cycles without sacrificing diligence.

- Operational cost discipline: With infrastructure energy and capacity becoming board-level issues, our playbooks focus on TCO levers that matter today: right-sizing compute and storage, choosing efficient networking topologies, integrating container strategies, and operational automation to reduce run-cost creep.

- Regulatory and grid-aware planning: The report embeds recent energy and grid developments into strategic planning. Practitioners will find guidance on aligning data center deployments with evolving utility constructs, emergent ratepayer initiatives, and regional transmission changes that affect availability and cost.

Key industry drivers and near-term shocks

- Open-source product evolution: The release of OpenStack 2026.1 (Gazpacho) introduces operational automation, improved workload migration tooling, and expanded hardware enablement — changes that materially reduce integration friction and shorten time-to-value for new deployments.

- Operational footprint and energy dynamics: Data center electricity demand remains a strategic input for cloud planning. Recent analyses underscore continued growth in data center energy consumption globally and concentrated U.S. demand that influences site selection, colocation economics, and sustainability reporting.

- Public-private coordination on grid capacity: New industry pledges and transmission interventions announced through early 2026 introduce both opportunities and obligations for large-scale deployments. These developments make energy procurement strategy and on-site resiliency part of core cloud economics.

- Security and compliance cadence: Enterprise customers should factor vendor security update practices and integration with broader platform security stacks into vendor selection — a consideration underscored by high-profile vendor advisories in 2025–2026.

Competitive landscape: who to watch and why

The market comprises established enterprise software firms, pure-play OpenStack specialists, infrastructure OEMs, and regional integrators. Our competitive analysis highlights strategic positioning rather than raw share numbers, looking at product breadth, delivery models, and service innovation capacity.

- Red Hat (USA) — Offers a full enterprise OpenStack platform with deep integration into hybrid cloud stacks and proven consulting and migration tooling. Well suited for organizations seeking a broad enterprise support model tied to existing Red Hat ecosystems.

- Mirantis (USA) — A pure-play OpenStack provider that emphasizes managed services and build-operate-transfer models, strong for telco and production-grade cloud deployments where operations expertise is a gating factor.

- Canonical (UK) — Combines automated deployment (Charmed OpenStack) with fixed-price consulting and fully-managed offerings, attractive to buyers seeking predictable commercial constructs and rapid time-to-deploy on Ubuntu stacks.

- Rackspace Technology (USA) — Positions OpenStack services within hybrid managed cloud portfolios and Elastic Engineering pods; a fit for enterprises that want vendor-managed operations with multi-cloud orchestration.

- VEXXHOST (Canada) — Specialist in hosted private clouds and migration tooling, often selected by customers that need turnkey private cloud hosting with migration accelerators.

- StackHPC (UK) — Focused on research and scientific computing, offering design consultancy optimized for HPC and containerized workloads in academic and research institutions.

- SUSE (Germany) — Provides enterprise-grade OpenStack support with emphasis on scalable private clouds and long-term maintenance commitments.

- IBM (USA) — Leverages integration expertise and enterprise consulting to deliver hybrid OpenStack solutions, often in conjunction with larger transformation programs.

- HPE (USA) — Offers OpenStack-compatible infrastructure and edge-to-cloud integrations, suitable for customers that want vendor-aligned hardware and services bundles.

- Ultimum Technologies (Czech Republic) — A European contender offering hosted and on-site private cloud solutions with end-to-end implementation services for regional customers.

Across these vendors, the practical differentiators tend to be delivery model (managed vs. professional services), automation maturity, vertical specialization (telco, research, enterprise), and commercial design (fixed-price vs. time-and-materials). Our vendor scorecards in the full report map these attributes to buyer personas and decision triggers.

What’s inside the PW Consulting report (practical deliverables)

The report is engineered as an operational toolkit rather than an academic exercise. The contents include:

- Executive decision frameworks to align OpenStack investments with business imperatives (cost, control, compliance, performance).

- Build-versus-buy financial models with sensitivity scenarios for energy, labor, and migration timelines to inform 3–5 year TCO planning.

- Vendor evaluation matrices and RFP templates tailored to managed services, fixed-price deployments, and build-operate-transfer engagements.

- Migration and coexistence playbooks that cover lift-and-shift, replatforming to cloud-native stacks, and phased hybrid architectures.

- Operational run-books with automation checklists inspired by recent upstream releases that accelerate secure and repeatable ops.

- Energy, resiliency and site-selection checklist aligned to contemporary utility and transmission developments.

- Risk register and compliance checklists tied to 2026 security advisories, governance expectations, and data residency constraints.

- Industry case studies and vendor negotiation tactics drawn from live deals and procurement engagements.

Importantly, the report surfaces prescriptive recommendations but intentionally omits granular segmentation payloads in this public summary. Readers who require the full dataset — including regional, service-type, and enterprise-size splits, as well as the detailed financial annexes — will find them in the full report package available from PW Consulting.

Actionable recommendations for 2026

- Start with the use-case, not the stack: Map workloads to migration archetypes and choose service models that shorten risk-bearing phases. The fastest path to value is often a hybrid staging pattern that isolates stateful services during cutover.

- Incentivize automation at procurement: Embed automation maturity and measurable run-rate reductions into contracts. That creates alignment on outcomes and reduces long-term ops cost.

- Factor energy and grid risk into capital decisions: Energy-backed incentives and new transmission arrangements materially affect site economics — model these scenarios in your TCO analysis.

- Use vendor diversity strategically: A multi-vendor approach can reduce supplier risk, but it should be governed by a clear platform integration strategy to avoid operational sprawl.

- Leverage upstream improvements: Recent OpenStack releases materially reduce migration friction. Plan pilot projects to validate automation and workload migration capabilities before committing to large-scale rollouts.

Next steps and how to access the full intelligence

For organizations preparing capital and operational plans in 2026, this report offers the market context, practical tools, and vendor mappings necessary to move from analysis to procurement. To preserve strategic leverage for our clients, this public summary showcases the insights and frameworks; the full report contains the granular segmentation, financial models, and appendices that operational teams require to execute.

Contact PW Consulting or visit our OpenStack Service Market 2026 report page to download the complete dataset, vendor scorecards, and the RFP toolkit designed for immediate application in 2026 procurement cycles.

For detailed analysis of this topic, please visit the official page:Openstack Service Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com