Smart Home IoT Sensors Driving Personalized Comfort

Other |

2026-02-16 06:00:19

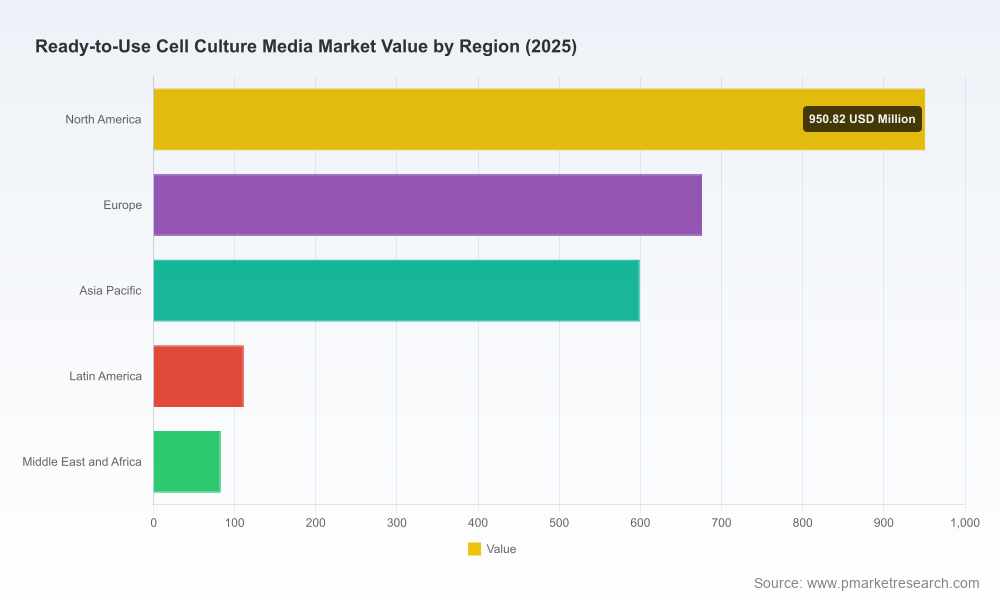

PW Consulting’s Ready To Use Cell Culture Media Market study positions this segment as a robust, mid-sized life sciences vertical that is entering a new phase of commercial and operational complexity. The market reached approximately USD 2.42 billion (USD Million basis) in 2025 and is projected to expand to roughly USD 2.64 billion in 2026, with a 2026–2032 compound annual growth rate (CAGR) of 7.3%, driving an estimated market approaching USD 4.0 billion by 2032. For corporate strategists planning investments, portfolio pivots, or M&A in 2026, this report translates growth trajectories into executable choices—while intentionally withholding granular segment values here to encourage direct access to the full dataset and modeling tools provided in the report.

Ready To Use Cell Culture Media Market

Buy-side and sell-side choices in 2026 must account for more than topline expansion. Biopharma process maturation (e.g., viral vectors, cell and gene therapies), renewed emphasis on vaccine manufacturing capacity, and scaling of translational research investments are changing the product and service expectations for ready-to-use media providers. PW Consulting’s analysis highlights five actionable strategic levers for executives:

Ready To Use Cell Culture Media Market

The drivers behind the mid-single-digit-plus CAGR are multifold and persistent into 2032. Commercial biologics and advanced therapies are increasing demand for high-quality, validated media that support scale-up and regulatory submission. Simultaneously, research throughput—particularly translational and stem cell workflows—continues to demand off-the-shelf, reproducible formulations, supporting both classical and specialty portfolios.

Ready To Use Cell Culture Media Market

Regulatory and quality developments are accelerating commercialization complexity. Notably, industry-first certifications and expanded cGMP recognition for media manufacturers have shifted supplier selection from cost-first to compliance- and traceability-first mindsets. At the same time, the raw-material and formulation trend toward chemically defined, animal component-free solutions reduces process risk but requires investment in formulation science and supplier qualification. Finally, logistics—especially temperature-controlled shipping and single-use packaging strategies—are now front-line constraints that affect both time-to-market and margin management.

The market structure reflects an industry where established life sciences suppliers and specialized vendors coexist. Top-tier organizations offer deep portfolios across classical, chemically defined, serum-free, and specialty media, and they compete on product breadth, regulatory pedigree, global manufacturing, and channel reach. A number of niche and mid-sized companies differentiate on primary cell media, stem-cell and immune cell solutions, or by bundling media with cell kits and services.

Recent corporate moves illustrate how competition is evolving: major suppliers have extended GMP-level capabilities and introduced room-temperature-stable or bench-stable product variants to ease logistic burdens; a specialist supplier expanded into GMP custom media services and launched combined cell + media kits to accelerate primary cell workflows; and an incumbent achieved an industry-first EXCiPACT cGMP certification across multiple production sites—evidence that compliance credentials and niche service offerings are increasingly decisive in buyer selection.

PW Consulting’s report includes a supplier scorecard and strategic heatmap that evaluate vendors on manufacturing footprint, regulatory certifications, product innovation, and commercial model—but to preserve strategic value this public preview omits the detailed scorecard rankings. Clients will find the complete competitive assessments, including partner-fit matrices and deal-readiness checklists, in the full report package.

Manufacturing and supply chain choices made in 2026 will materially influence 2027–2030 performance. Key operational priorities identified in the report include:

We advise companies to adopt differentiated commercial plays depending on scale and capability:

Our revenue-mapping framework in the report shows how channel mix, pricing architecture, and service intensity drive realized margin under multiple adoption scenarios—insight that is often decisive in board-level allocation decisions.

Given the market’s moderate concentration, strategic M&A in 2026 can be highly accretive if it targets capability gaps rather than market share alone. Recommended transaction archetypes include:

PW Consulting’s proprietary M&A screening tool included in the report ranks targets by technical fit, regulatory posture, and integration risk—an essential resource for deal teams crafting 100-day plans.

The full report is built as a decision-support toolkit for executives making 2026 resource and portfolio choices. Key deliverables include:

To honor the “trailer” principle, we summarize these capabilities here but withhold granular regional, application, and segment-level tables—these are available in full to subscribers and clients who access the report portal.

Beyond the report, PW Consulting provides tailored services to convert insight into action:

The Ready To Use Cell Culture Media market presents a clear growth runway, but the nature of that growth rewards technical credibility and operational discipline more than broad commercial reach. Executives planning 2026 investments must prioritize regulatory-ready manufacturing, differentiated product platforms (chemically defined and serum-free solutions), and supply-chain resilience—especially temperature control and traceability. Strategic M&A and partnerships that close capability gaps (not just expand product lists) will produce the most durable returns.

PW Consulting’s Ready To Use Cell Culture Media Market report converts these imperatives into executable roadmaps. For a complete view of the segment-level forecasts, regional dynamics, supplier rankings, and downloadable financial models, please refer to the full report available via our research portal.

For detailed analysis of this topic, please visit the official page:Ready To Use Cell Culture Media Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com