Rosin Resin Market: Strategic Imperatives for 2026 — PW Consulting Executive Brief

Executive summary

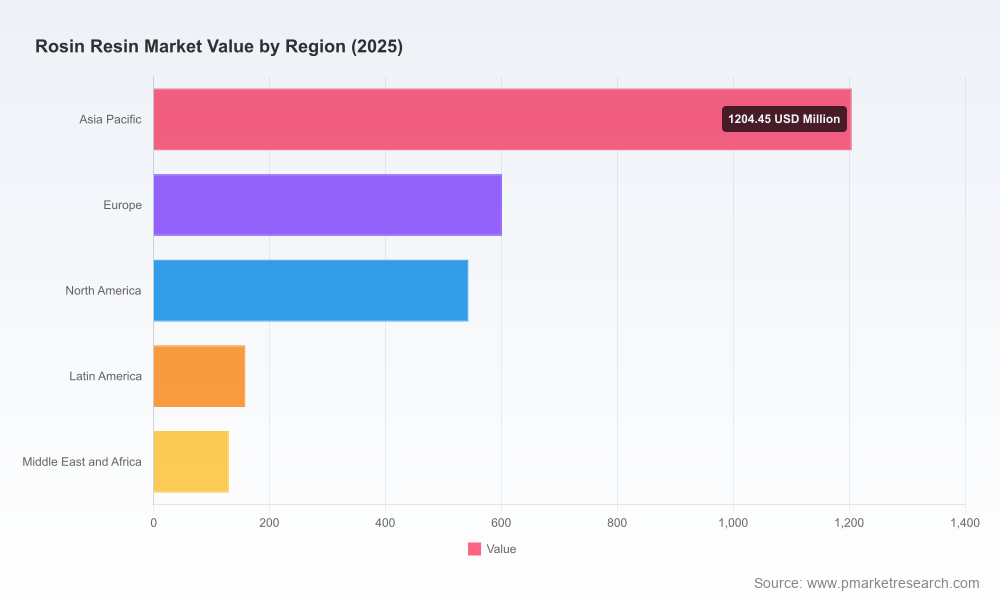

The global rosin resin market has entered a phase of steady expansion and selective consolidation. Our new market model — anchored on a 2025 base year and projecting across 2026–2032 — shows the industry expanding from approximately USD 2.64 billion in 2025 toward a multi‑billion dollar opportunity by the end of the forecast horizon, at an expected compound annual growth rate (CAGR) of roughly 4.4% through 2032. This trajectory reflects a blend of demand resilience in traditional end‑uses (adhesives, inks, rubber compounding) and accelerating adoption where rosin derivatives offer low‑VOC or bio‑based regulatory advantages.

Rosin Resin Market

As PW Consulting’s senior strategy and industry analysis team, we prepared this executive brief to highlight the specific kinds of strategic decisions where our report delivers immediate, operational value for 2026 planning cycles — from portfolio prioritization and commercial expansion to supply‑chain hedging and M&A scouting. This is a curated preview: we show the analytic lenses and actionable paths but intentionally withhold granular segment tables and proprietary subsegment metrics to preserve research exclusivity and drive readers to the full report for the source datasets, financial models, and supplier scorecards.

Rosin Resin Market

Why this matters for 2026 decision-makers

- Resource allocation. The near‑term environment will reward companies that reallocate R&D and commercial spend toward formulations that leverage rosin’s sustainability attributes — particularly in jurisdictions tightening VOC and bio‑content rules.

- Supply continuity & margin protection. Volatile upstream pricing for pine resins and trade policy shifts mean procurement strategies, including strategic inventory, diversified sourcing, and indexed contracts, will materially affect 2026 margin outcomes.

- M&A and partnership timing. Moderate market concentration and pockets of specialization create acquisition windows for buyers seeking adhesive‑grade or bio‑based rosin platforms; 2026 is likely to be an inflection year for bolt‑on consolidation versus greenfield capacity builds.

Market dynamics: drivers, risks and leading indicators

Three structural forces are shaping the market outlook:

Rosin Resin Market

- End‑market demand mix. Traditional segments (adhesives & sealants, printing inks, rubber compounding) remain the backbone of demand. Simultaneously, regulatory and formulation shifts — especially in packaging, construction sealants, and specialty coatings — are elevating rosin derivatives that meet low‑VOC and bio‑sourcing criteria.

- Raw material volatility. Pine resin feedstock shows regional price differentials and historic volatility driven by production cycles and climatic/tapping activity. Market participants must treat resin pricing as a high‑impact input risk for 2026, with near‑term indicators including plantation tapping rates, Q‑on‑Q inventory movements at major producers, and freight cost spreads.

- Trade and regulatory context. Recent policy moves, including reciprocal tariff measures and tightening VOC regulations in key export markets, are reshaping trade flows and reformulation imperatives. Companies with flexible supply chains and formulation capability will have a clear advantage.

Selected market facts that shape commercial strategies

- Historical momentum: the market expanded materially during the early 2020s and stabilized into mid‑decade growth, reinforcing the viability of continued investment in rosin‑based chemistries.

- Raw material pricing snapshots and volatility are acute: pine resin price benchmarks in late‑2025 demonstrated meaningful regional spreads, while 2023–2024 experienced double‑digit percentage swings linked to reduced tapping in several supply provinces. These movements are the most reliable leading indicators for short‑term margin pressure and procurement opportunity.

- Competitive structure: the industry exhibits moderate fragmentation with a cluster of global producers and many regionally specialized manufacturers. This structure supports both niche specialization plays and roll‑up strategies by mid‑sized chemical platforms.

Competitive landscape — playbooks and implications

Our company‑level analysis synthesizes corporate positioning, product portfolios, channel access and recent commercial actions. Highlights include:

- Eastman Chemical Company (Kingsport, TN). Deep formulation expertise and recent product introductions focused on heat‑activated and specialty adhesives position Eastman to capture packaging and sanitary adhesive upgrades. Strategy implication: competitors should evaluate defensive co‑development or differentiated pricing structures where Eastman’s technical advantage shortens time‑to‑market.

- Harima Chemicals Group (Japan). Strong upstream integration in pine chemicals and a clear pivot to eco‑friendly adhesive lines make Harima a bellwether for sustainable rosin formulations. Strategy implication: licensing, joint development, or selective distribution partnerships could accelerate market access in eco‑differentiated segments.

- Arakawa Chemical Industries (Japan) and Lawter (Harima subsidiary). Focus on tackifiers and printing inks — companies with heavy exposure to printing must monitor product improvements that could substitute conventional binders.

- Kraton Corporation (Houston, TX). Tall oil and bio‑based rosin derivatives form part of Kraton’s bio‑portfolio. For downstream players targeting sealants and rubber applications, Kraton is a strategic supplier and potential co‑innovation partner.

- DRT (Dax, France) and European specialty players. These firms are strong in rosin derivatives for adhesives, coatings and fragrances; they are adept at navigating EU regulatory regimes and can be preferred partners for companies seeking compliant formulations.

- Regional producers and suppliers (China, Indonesia, Brazil, Portugal, etc.). Several Asia‑ and Latin America‑based manufacturers supply core gum rosin and derivatives at competitive cost points. Strategy implication: prioritize supplier qualification and capability audits to mitigate quality and logistics risk while leveraging cost arbitrage.

Recent industry moves — implications for 2026

- New product launches from established chemicals companies are accelerating product substitution opportunities in adhesives and heat‑activated systems. These launches increase competitive intensity in higher‑margin specialty applications.

- Bio‑based product introductions and eco‑positioning underscore an industry tilt toward sustainability claims that are increasingly required by procurement teams in packaging and construction end markets.

- Tariff actions and selective trade exemptions are introducing complexity to cross‑border sourcing strategies; near‑term winners will be firms that can quickly re‑route flows or leverage local production footprints to avoid tariff impacts.

What the full PW Consulting Rosin Resin Market report delivers

For decision makers executing 2026 plans, the full report is organized to convert insight into action through:

- Proprietary market sizing and scenario forecasts (base 2025; detailed 2026–2032 projections) with sensitivity testing for pricing, feedstock shocks and policy changes.

- Commercial playbooks for suppliers, formulators and manufacturers — including go‑to‑market prioritization frameworks, channel economics, and SKU rationalization matrices.

- Supplier benchmarking and a curated M&A radar with acquisition targets, earn‑out valuation scenarios and integration risk scoring.

- Regional supply‑chain maps and trade‑flow analytics (including tariff sensitivity and freight volatility modelling) to support sourcing/hub decisions.

- Raw material price models and hedging templates informed by plantation tapping, production cycles and short‑term market indicators.

- Regulatory impact assessments and formulation pathways to meet low‑VOC and bio‑content standards across major regulatory regimes.

- Excel models and data packs for corporate planners: downloadable datasets, unit‑economics templates and scenario dashboards for board‑level briefings.

Actionable recommendations for 2026

- Rebalance R&D towards sustainability‑enabled differentiation. Prioritize projects that reduce VOC or improve bio‑content while protecting cost competitiveness; these investments pay off when combined with certification and co‑marketing programs.

- Implement dynamic procurement and hedging strategies. Use short‑term inventory levers and indexed supply contracts to smooth input cost volatility; target diversified feedstock pools and alternative chemistries as contingency corridors.

- Assess bolt‑on M&A for capability gaps. Given moderate market concentration and specialized niches, prioritize targets that offer formulation IP, customer contracts in high‑value end markets, or local production that neutralizes tariff exposure.

- Upgrade commercial analytics. Invest in customer profitability and route‑to‑market models to identify where premium rosin derivatives can command price premiums versus volume plays.

- Prepare compliance and go‑to‑market playbooks for changing trade rules. Scenario‑plan for tariff permutations and maintain alternative regional supply options to avoid abrupt margin erosion.

How to use this brief and next steps

This briefing is intended to orient leadership teams and strategy planners for 2026 budget cycles and to highlight where the full research package adds decisive tactical value. If your team is preparing capital allocation, product roadmaps, or a shortlist of acquisition targets, the full PW Consulting report contains the datasets, models and supplier scorecards required to finalize those decisions with confidence.

We have deliberately positioned this note as a strategic preview: the full report contains the granular subsegment tables, regional and application level breakouts, and downloadable financial‑model templates that underpin investment cases for 2026 and beyond.

Conclusion

The rosin resin market offers a blend of steady baseline growth and targeted pockets of high strategic value for firms that can marry formulation capability with supply‑chain flexibility. For 2026, the companies that win will be those that (a) act decisively on sustainability‑differentiated product development, (b) de‑risk upstream feedstock exposure, and (c) selectively pursue acquisitions or partnerships that fill technical or regional gaps. PW Consulting’s full Rosin Resin Market report provides the operational blueprints and quantitative backing to execute these moves — from scenario‑tested investment cases to supplier due diligence checklists.

To obtain the full dataset, models and company scorecards referenced here, contact PW Consulting or visit our report page for Rosin Resin Market — 2026 Strategic Edition.

For detailed analysis of this topic, please visit the official page:Rosin Resin Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com