Home Pet Deworming Medicine Market — Strategic Outlook for 2026: Key Takeaways from PW Consulting’s New Study

Executive snapshot

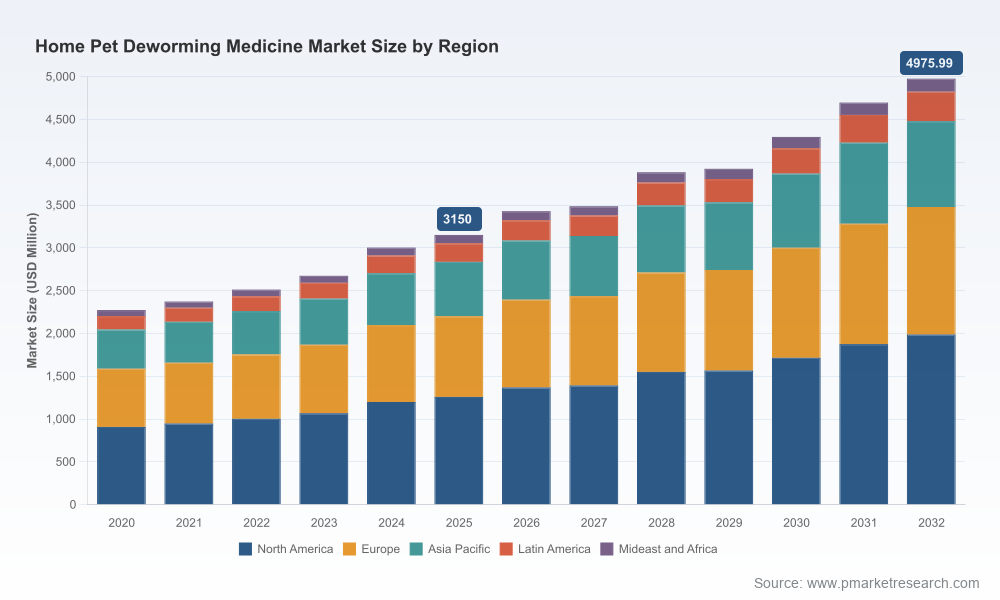

PW Consulting’s latest market study on Home Pet Deworming Medicine synthesizes five years of historical data (2020–2025) and delivers a seven-year forecast (2026–2032) designed specifically to inform executive decision-making in 2026. The global market has demonstrated resilient expansion, driven by rising pet ownership, increasing preventative care adoption, and expanded retail and e-commerce channels. Our base-year sizing (2025) places the market in the multi-billion USD range, and the study projects a steady compound annual growth rate (CAGR) of 6.75% across the 2026–2032 forecast window, culminating in near-term and medium-term opportunity pools that merit strategic action now.

Home Pet Deworming Medicine Market

Why this study matters for 2026 planning

- Actionable, finance-grade sizing. The report provides enterprise-ready topline forecasts and demand-driver decomposition that feed directly into FY-26 revenue targets, investment cases, and valuation modeling.

- Operational playbooks, not just charts. Beyond market figures, we translate insights into executable initiatives — go-to-market blueprints, SKU rationalization matrices, pricing-sensitivity models, channel pilots, and supply-chain risk mitigations — that are ready for immediate deployment.

- Scenario-based decision support. Given accelerating generic entry and regulatory variability, our scenario simulations let executives stress-test portfolio strategies under differing price erosion, raw-material volatility, and channel-disruption assumptions.

Market trajectory and what it implies

From our historical baseline to the 2025 benchmark, the home pet deworming market has expanded materially and is forecast to continue a steady climb through 2032. Total market value grew meaningfully over the 2020–2025 period and, under our central case, will advance at a CAGR of 6.75% in 2026–2032. That growth supports several immediate implications for corporate strategy:

Home Pet Deworming Medicine Market

- There is room to pursue both expansion and efficiency: revenue pools are expanding, yet cost pressures from API sourcing and generics require disciplined margin management.

- Medium-term value creation will be concentrated not only in volume growth, but in value-added product differentiation (formulation, palatability, combined active ingredients) and channel optimization (vet-prescribed vs. OTC vs. e-commerce).

- Regulatory and generics dynamics will compress time-to-action windows; delaying a response to generic approvals or supply shifts will materially affect branded market share and pricing power.

Competitive landscape — what the numbers conceal and what matters

The market exhibits moderate concentration: our concentration metrics indicate that the top three players hold a meaningful but not dominant share of the market, while the top five firms control a clear majority. This structure produces a competitive environment where leading incumbents can influence pricing and channel access, yet opportunities remain for agile challengers and private-label entrants.

Home Pet Deworming Medicine Market

Key companies profiled in the study include legacy animal-health leaders and specialized veterinary players — firms with different strategic postures and portfolio focuses. Highlights:

- Zoetis — a broad companion-animal player with liquid and oral dewormer offerings; strength lies in brand recognition and vet-channel relationships.

- Merck Animal Health — entrenched in broad-spectrum chemotherapies with an emphasis on clinical efficacy and veterinarian trust.

- Elanco — leverages chewable formulations and combination products; active in both prescription and OTC pathways.

- Virbac, Boehringer Ingelheim, Ceva, Dechra — diversified portfolios and regional strengths that matter for targeted partnerships and licensing plays.

- PetIQ, Central Garden & Pet (Farnam), Durvet — important vectors for over-the-counter and retail distribution, often leading on price and shelf presence.

Our competitive analysis goes beyond listing product names: for each rival we map R&D pipelines, SKU-level pricing bands, promotional elasticity, channel footprints, and patent expiry timelines — all structured to help you evaluate offensive and defensive options for 2026.

Recent industry developments and regulatory context

- Early-2026 regulatory activity has tangible market consequences. The January 2026 FDA approval of a generic fenbendazole oral suspension (Defendazole by Norbrook) signals accelerated genericization risk for certain formulation classes and will pressure pricing and branded margins in segments built around fenbendazole-based products.

- In late 2025, an Emergency Use Authorization for a cat product underscores how regulatory pathways can create episodic demand spikes and unique market access windows. Such events also highlight the need for companies to keep regulatory contingency playbooks current.

- Raw material concentration matters: fenbendazole API production is heavily concentrated in the Asia Pacific region (notably India and China). Companies that fail to secure diversified API sources or hedging arrangements may face input-cost and availability shocks.

- Over-the-counter products — particularly those containing pyrantel pamoate and praziquantel — are subject to strict labeling and safety instructions under the FDA framework. Compliance and consumer-education investments are therefore non-negotiable.

What the report contains — practical modules for 2026 execution

The PW Consulting study is organized to accelerate action. Key operational modules include:

- Robust market-sizing methodology and an interactive financial model (Excel) that lets teams re-run forecasts under custom assumptions (price erosion, adoption curves, channel shift scenarios).

- Demand-driver decomposition: pet population dynamics, preventative-care adoption rates, vet-prescription vs. OTC conversion, e-commerce penetration, and seasonality effects.

- Supply-chain and raw-material analysis: API sourcing maps, supplier concentration risk scoring, cost-levers, and a procurement playbook for single-ingredient and combination formulations.

- Competitive profiling: 10+ company deep dives with go-to-market positioning, SKU economics, patent timelines, recent M&A activity, and potential white-space opportunities.

- Commercial playbooks: SKU rationalization templates, pricing elasticity tests, trade-promo optimization, private-label opportunity assessments, and channel-partner negotiation guides.

- Regulatory & compliance toolkit: labeling checklists, OTC-to-prescription transition scenarios, and a regulatory-impact matrix tied to revenue and margin outcomes.

- M&A and partnership evaluation: target-screening criteria, valuation benchmarks, and an integration checklist tailored to pet-health assets.

- Risk heatmap and mitigation plans: scenario matrices covering generic entry, API disruption, and rapid regulatory changes — each linked to recommended tactical responses.

Strategic playbook — eight priorities for 2026

- Secure API diversity and hedging: migrate beyond single-source dependencies for fenbendazole and other key actives; evaluate toll-manufacturing partnerships in multiple geographies.

- Prioritize SKU and channel profitability: decouple volume-driven SKUs from margin-enhancing differentiated offerings (e.g., palatable chewables, combination therapies).

- Design for generics pressure: proactively plan life-cycle management for branded formulations — consider line extensions, bundling, and service-based differentiation (tele-vet consultations, adherence programs).

- Invest in regulatory readiness: maintain up-to-date FDA labeling compliance and build rapid-response teams for EUA-like contingencies.

- Leverage e-commerce and subscription models: capture recurring demand through auto-refill programs and pet-health subscriptions that increase lifetime customer value.

- Execute targeted M&A or licensing in mid-market niches: the market’s concentration profile leaves openings for bolt-on acquisitions that can scale quickly via incumbent distribution networks.

- Strengthen retail and vet-channel partnerships: tailor assortments and co-marketing to channel economics rather than one-size-fits-all product deployments.

- Build consumer trust through education: invest in clear, compliant labeling and multi-channel consumer education to reduce misuse risks and elevate brand preference.

How executives should use this research

Leaders should treat the report as both a strategic compass and an operations manual. Use the topline forecasts and scenario tools to set FY-26 targets, allocate R&D and commercial funding, and prioritize supply-chain investments. Deploy the playbooks to run 90-day pilots (e-commerce subscription, SKU rationalization, API dual-sourcing) and translate pilot results into scaled rollouts in H2 2026.

Next steps and access

This article provides a strategic preview of PW Consulting’s full Home Pet Deworming Medicine Market report. The full deliverable contains the proprietary segment-level detail, interactive models, and confidential appendices that we intentionally omit here to preserve research value and to direct in-depth inquiries through our client channels.

For executive briefings, access to the full financial model, or tailored workshops to convert these insights into a 100‑day plan for 2026, contact PW Consulting’s Companion Animal Health Practice. Our analysts will walk your leadership team through the data, validate scenario assumptions against your internal KPIs, and co-create the tactical roadmap needed to capture the expanding opportunities in the home pet deworming market.

For detailed analysis of this topic, please visit the official page:Home Pet Deworming Medicine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com