Centrifugal Axial Flow Pump Market Expansion Driven by Industrial Development

Causes |

2026-07-06 16:30:04

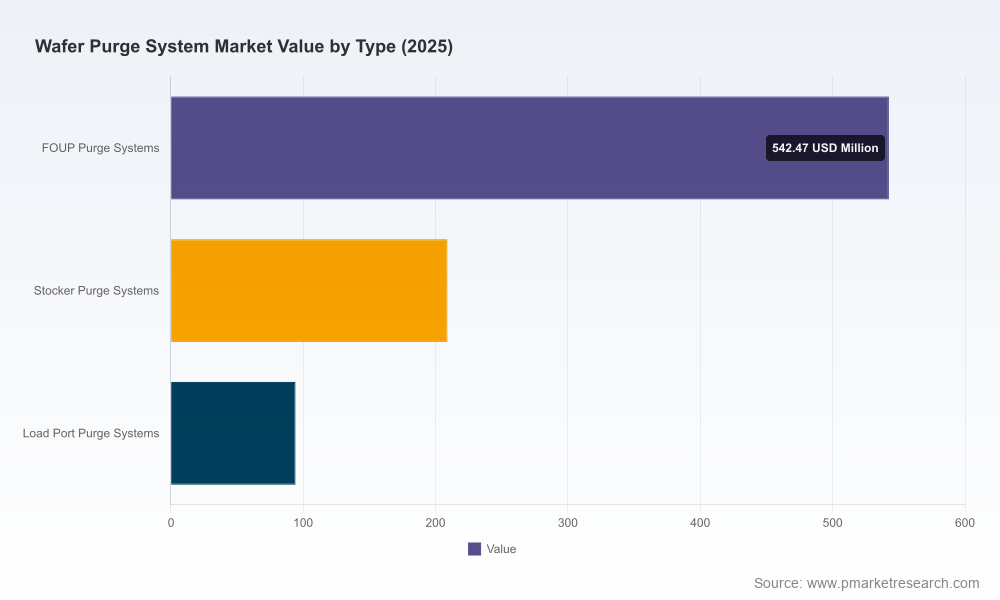

PW Consulting today publishes an executive briefing drawn from our forthcoming Wafer Purge System Market Research report (base year: 2025; historical coverage: 2020–2025; forecast: 2026–2032). Built as a decision-support dossier for semiconductor fabs, OEMs, and capital equipment investors, this briefing explains why the wafer purge equipment market is a strategic battleground in 2026 — and how senior leaders should translate emerging signals into capital and operational choices. Our model shows the total addressable market expanding from roughly USD 535 million in 2020 to USD 845.5 million in the 2025 base year, accelerating into the forecast horizon (2026–2032) at a 9.5% CAGR and reaching around USD 1.6 billion by 2032.

Wafer Purge System Market Research

Node scaling, higher-value 300 mm flow lines, and more aggressive defect budgets are putting purge strategy squarely into process control and yield management conversations. As lithography and etch steps tighten oxide/humidity tolerances, purge systems shift from a peripheral utility to a direct contributor to yield preservation.

Wafer Purge System Market Research

Simultaneously, energy and gas consumption economics, combined with rising input costs for stainless steel and precision sensors, are changing TCO math. Buyers can no longer treat purge systems as a commoditized ancillary purchase; procurement must evaluate lifetime operating expense alongside initial CAPEX.

Wafer Purge System Market Research

Regulatory and trade dynamics add complexity. Compliance frameworks such as SEMI S2 and evolving export licensing rules for front-end equipment affect supplier selection, qualification timelines, and the feasible destination markets for some classes of purge-capable modules.

The full report has been created to support 2026 decisions with operational rigor rather than high-level observation. Key deliverables include:

Validated market sizing and a granular forecast model (USD Million basis; base year 2025) with scenario toggles for adoption rates, retrofit penetration, and node mix.

TCO and OPEX models that isolate gas consumption, energy, maintenance, and consumable costs — enabling side-by-side comparisons of retrofit vs new-install strategies over multi-year horizons.

Retrofit feasibility playbooks that map mechanical, software, and cleanroom-interface requirements for FOUP/SMIF pod purging, stocker integration, and load-port upgrades.

Supplier scorecards and procurement templates tailored to risk appetites: quick-buy spares strategy, multi-sourcing thresholds, and qualification test plans aligned to SEMI S2 compliance and typical fab acceptance protocols.

Operational case studies and field-validated best practices that illustrate yield-impact pathways and real-world deployment sequences — presented as executable checklists for engineering and fab operations teams.

Regulatory and export-control mapping for buyers and exporters: compliance checkpoints, documentation pathways, and implications for geographic rollout strategies.

The market shows clear technology differentiation and supplier specialization. Rather than disclosing sensitive share-by-segment figures in this briefing, we summarize strategic postures and capability differentials that matter in procurement and partnership decisions.

Fabmatics (Germany) — Position: retrofit specialist. Strengths lie in modular pod-purge solutions that enable continuous inert-gas purging in overhead buffers and retrofittable storage racks. Strategic implication: ideal partner for fabs seeking short-cycle yield protection without wholesale stocker replacement.

Murata Machinery (Muratec, Japan) — Position: integrator with thin-unit retrofits. Known for mass-flow control and nozzle design that prioritize flow efficiency and pre-purge strategies. Strategic implication: strong fit where low operating gas volumes and precise flow control are procurement priorities.

Rorze Corporation (Japan) — Position: equipment OEM with product lines spanning stockers and bottom-purge load ports. Emphasis on nozzle mechanisms and cleanliness performance. Strategic implication: attractive for fabs seeking vertically integrated material handling with embedded purge capability.

Palbam Class (Israel) — Position: FOUP/SMIF-centric purging and ultraclean cabinet solutions. Strengths in automation and desiccator-style storage. Strategic implication: solution partner for facilities focused on long-dwell storage control in cleanroom settings.

Daifuku (Japan) — Position: AMHS integrator. Offers purge-enabled stockers and storage systems that integrate with fab material flows. Strategic implication: best-in-class when purge must be embedded into material-handling workflows.

Sinfonia Technology (Japan) — Position: load-port specialists with movable nozzles and EFEM integration options. Strategic implication: key supplier for equipment OEMs specifying load-port-level purge without stocker replacement.

Kostek Systems (South Korea) — Position: modular LPM vendors focused on MFC control and host communications. Strategic implication: flexible implementations for testbeds and pilot lines.

Santa Phoenix Technology (Taiwan) — Position: fab-focused N2 charging and carrier storage, with deployments at major foundries. Strategic implication: local-market advantage where close foundry partnerships and rapid field support are decisive.

SEMI-TS (South Korea) — Position: system exhibitor/integrator combining purge modules into AMHS and clean conveyor ecosystems. Strategic implication: watch for ecosystem plays bundling purge with high-level material flow automation.

Innovations in low-energy flow control are material. Recent valve developments lower purge consumption meaningfully, changing payback dynamics for retrofit projects and shifting the buyer conversation toward operational savings as the primary ROI.

Supply-side cost pressure on precision metals and sensors tightens procurement windows and increases the value of long-lead supplier relationships. Buyers should bake material-cost escalation scenarios into three- to five-year CAPEX planning.

Regulatory compliance is non-negotiable and must be designed-in early. SEMI S2-related validation steps and export control screenings introduce schedule risk that can extend qualification lead times — an often overlooked source of schedule slippage in 300 mm capex projects.

Mitigation for input-cost inflation: adopt staged procurement contracts with indexed pricing floors/caps, and prioritize suppliers with near-term capacity guarantees or vertical sourcing control over critical components.

Compliance and export risk mitigation: include export-clearance gating in supplier selection, and plan alternative procurement scenarios for restricted destinations.

Operational risk mitigation: run pilot installations under production-like dwell cycles to validate purge dynamics and integrate O2/humidity monitoring into existing fab MES telemetry before full rollouts.

Start with the objective: define whether your program is CAPEX-led (new builds) or OPEX-led (retrofit yield lift). The report provides a decision checklist that maps objective to supplier archetype and contract terms.

Leverage the TCO models: run sensitivity analyses for gas pricing, valve efficiency gains, and material-cost inflation to set realistic payback thresholds for upgrades.

Shortlist suppliers by capability cluster (retrofit, integrated AMHS, load-port specialists) and require vendor-supplied qualification packages mapped to SEMI S2 and your fab acceptance criteria.

Time procurement to avoid both component lead-time risks and regulatory windows; a staged procurement approach reduces schedule exposure while preserving optionality.

With the wafer purge equipment market growing from half-a-billion-dollar scale in 2020 to an USD 845.5 million base in 2025 and projected growth at a 9.5% CAGR into a market approaching USD 1.6 billion by 2032, purge strategy is no longer peripheral. For 2026 capital planners, operations leaders, and procurement heads, the right mix of retrofit capability, flow-efficiency technology, regulatory foresight, and supplier alignment will determine both near-term yield outcomes and multi-year TCO. PW Consulting’s full market report is designed to convert this high-level trendline into executable programs — from vendor selection to field qualification, from compliance gating to OPEX optimization.

To access the full dataset, detailed scenario tables, supplier scorecards, and the operational playbooks referenced in this briefing, please visit the report landing page or contact PW Consulting’s semiconductor practice lead for a briefing session.

For detailed analysis of this topic, please visit the official page:Wafer Purge System Market Research

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com