PW Consulting Release: IoT in Energy Market — Strategic Playbook for 2026 Decision-Makers

As global energy systems accelerate digital transformation, PW Consulting’s new Internet of Things (IoT) in Energy Market report provides the tactical intelligence senior executives, investors, and program leads need to make high-stakes decisions in 2026. The market’s trajectory is clear: after rising from approximately USD 17.5 billion in 2020 to USD 32.4 billion in 2025, PW Consulting’s base-year analysis projects the market to reach roughly USD 37.2 billion in 2026 and to expand to nearly USD 76.8 billion by 2032 — an implied compound annual growth rate of 13.08% across the forecast window. These headline figures frame a strategic agenda: where to deploy capital, which capabilities to in-source or outsource, and how to build resilient IoT architectures that unlock value while containing risk.

Internet Of Things Iot In Energy Market

Why this report matters for 2026 strategy

- Decision clarity in a fast-moving market. The IoT-for-energy landscape is moving from pilots to scale. Our forecast quantifies the addressable opportunity and, more importantly, translates it into decision-relevant scenarios for utilities, asset owners, and energy service firms.

- Operational playbooks, not just slides. This is a practitioner-first product: the report includes deployment frameworks, procurement scorecards, and a vendor evaluation matrix designed to be used directly in RFPs, board discussions, and capital planning cycles.

- Risk-aware growth planning. With regulatory shifts, renewables integration, and pro-security executive orders influencing procurement and design, executives will find a roadmap to balance growth, compliance, and resilience.

Market trajectory: what the numbers mean for corporate plans

Two insights emerge from PW Consulting’s modeling. First, the IoT in energy market is maturing into a meaningful industry segment rather than a collection of point solutions. The nearly two-fold increase observed between 2020 and 2025 illustrates strong adoption across utilities, grid operators, and distributed energy participants. Second, the sustained 13.08% CAGR through the forecast period implies a long runway for investments that prioritize platformization, edge intelligence, and integrated operational analytics.

Internet Of Things Iot In Energy Market

For 2026 planning cycles, this has three immediate implications:

Internet Of Things Iot In Energy Market

- Prioritize cross-domain platforms. Growth favors organizations that bundle hardware, secure connectivity, and analytics into repeatable offerings that reduce integration cost and accelerate time-to-value.

- Design for scalability and modularity. Pilots that cannot be cost-effectively scaled will be stranded; capital allocation should favor modular architectures and vendor ecosystems that enable phased rollouts.

- Quantify TCO over lifecycle horizons. Rapid market growth hides differences in total cost of ownership — our scenario models show that architecture choices and connectivity stacks materially change long-term economics.

Industry dynamics shaping 2026 decisions

Several converging forces are reshaping outcomes for IoT projects in energy:

- Connectivity scale and standards. Low-power wide-area networks and cellular IoT deployments continue to expand rapidly — an industry report from the LoRa Alliance shows mass deployment momentum that keeps utilities among the largest adopters. That scale opens new options for network economics, but also raises interoperability and governance questions.

- Capital flows into energy infrastructure. With global energy investment rising into the trillions, much of the incremental spend is directed toward grids, storage, and renewables — the exact infrastructure that benefits from IoT-enabled visibility and control.

- Policy and reliability mandates. National-level policies aimed at grid reliability and security (including recent executive actions) are elevating requirements for resilience and for the assessment of impacts from intermittent resources. These mandates increase the value of grid-aware IoT platforms and advanced distribution management capabilities.

- Edge and cloud coexistence. Deployments are increasingly hybrid: edge computing for deterministic control and cloud-native analytics for cross-asset optimization. LF Edge initiatives and related projects demonstrate the practical value of secure, distributed measurement architectures for sustainability and compliance reporting.

Competitive landscape — how to interpret vendor strengths

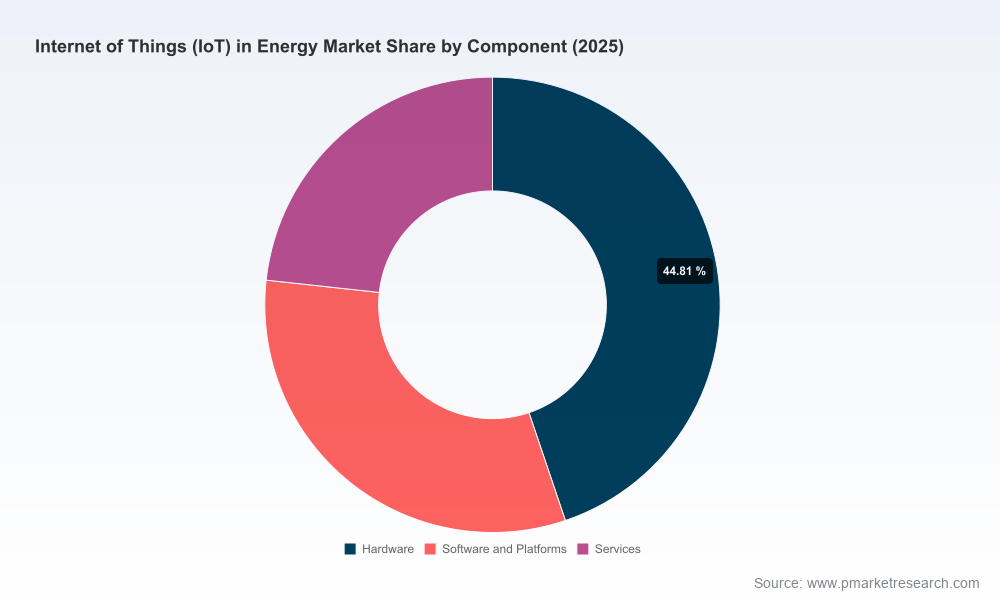

The market remains fragmented — our concentration analysis shows a low-to-moderate concentration with the three largest suppliers occupying under a fifth of the market and the top five below roughly a quarter — indicating ample room for specialized players and platform consolidation. For procurement teams, this fragmentation both complicates vendor selection and opens opportunities to build differentiated partnerships. Key strategic positions observed across vendor types include:

- Platform incumbents with industrial scale (Siemens AG, ABB, GE Vernova). These firms combine OT pedigree, digital twin capabilities, and deep system integration experience. Their value proposition centers on end-to-end solutions for generation, transmission, and distribution with strong integration into existing utility control systems.

- Energy management and building specialists (Schneider Electric, Honeywell). These vendors offer IoT-enabled architectures optimized for energy efficiency, building-grid interactions, and microgrid controls, often emphasizing modularity and enterprise energy management use cases.

- Network and edge infrastructure providers (Cisco, Semtech). Connectivity and secure edge compute are key bottlenecks as deployments scale. Cisco’s strengths in networking and security and Semtech’s device-level communications expertise make them strategic partners for utility-grade rollouts.

- Metering and grid-edge specialists (Itron, Landis+Gyr). With deep domain knowledge in metering and AMI, these players are essential for mass rollouts at the grid edge and for capturing high-frequency operational telemetry needed for analytics.

- Regional and systems integrators (Hitachi Energy). Companies that combine local execution capability with platform offerings help de-risk large modernization programs by bundling grid automation, digital substations, and implementation services.

Recent industry developments support these strategic distinctions: Hitachi Energy’s recognition as a major player in industrial IoT platforms underscores the competitive salience of grid automation; LF Edge deployments show measurable sustainability and compliance value from edge frameworks; and continued LoRaWAN scale lends credibility to future-proof connectivity choices. Procurement teams should treat vendor selection as a capability-mapping exercise, not a price-only competition.

What’s inside the report — operational deliverables for teams

Beyond market sizing and vendor profiles, the PW Consulting IoT in Energy Market report is intentionally designed to be applied directly to 2026 planning and 2027 implementation. Key deliverables include:

- Comprehensive market model and downloadable spreadsheets calibrated to supplier adoption curves and investment scenarios — usable for board-level and investment committee briefings.

- Implementation playbooks covering pilot design, scale-up triggers, vendor integration sequencing, and runbook templates for operations teams.

- Procurement toolkit: RFP templates, feature-priority matrices, and scoring rubrics to harmonize legal, security, and technical evaluations.

- Total cost of ownership (TCO) models with sensitivity analyses across connectivity, edge compute, cloud analytics, and maintenance.

- Security and compliance checklists tuned to recent regulatory milestones and executive directives affecting grid reliability and cyber resilience.

- Case studies and ROI benchmarks drawn from utility and industrial deployments, plus a common metric set for cross-project comparisons.

We deliberately do not disclose our full segmentation tables and granular regional/application splits in this preview; those datasets and the underlying assumptions are provided in full to clients who access the report package and licensing options. This “trailer” approach preserves the actionable intelligence that clients rely on while ensuring the integrity of our proprietary modeling.

How to use these insights in 2026 planning cycles

- Align funding to scaling milestones. Fund pilots with explicit scale-up gates — technical interoperability, unit economics, and vendor co-investment thresholds — and tie larger investments to verified outcomes.

- Prioritize platform partnerships, not point products. Favor vendors that can demonstrate cross-functional integration across hardware, connectivity, and analytics to reduce lock-in and integration cost.

- Embed cybersecurity and compliance early. Given rising regulatory focus on grid reliability and the scale of device deployments, embed security architecture and auditability into design specifications from day one.

- Design for hybrid operations. Deploy edge compute to support low-latency control and cloud analytics for cross-asset optimization; ensure data governance covers both layers.

- Use market intelligence to negotiate commercial terms. Leverage our vendor scoring and market sizing to negotiate outcomes-based contracts, volume discounts, and performance SLAs tied to operational KPIs.

Conclusion — the strategic edge for 2026

For 2026, IoT in energy is no longer an adjacent technology play; it has become central to operational resilience, emissions reduction, and the economics of an increasingly decentralized power system. PW Consulting’s report frames the financial opportunity, the competitive topology, and the tactical steps needed to convert pilots into enterprise value. With the market projected to more than double from mid-decade to 2032 and with connectivity and policy drivers accelerating adoption, the next 12–18 months are critical for establishing durable advantage.

To access the full dataset, granular segmentation, vendor scorecards, and the downloadable tools described here, visit PW Consulting’s report page or contact our advisory team for a tailored executive briefing and scenario workshop. The public snapshot in this press note is intended to guide strategic priority-setting; the full report supplies the detailed analytics and operational artifacts necessary to execute confidently.

For detailed analysis of this topic, please visit the official page:Internet Of Things Iot In Energy Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com