North America Single Use Medical Devices Reprocessing Market Size, Share, Current Trends, and Forecast by 2033

Other |

2026-06-22 10:07:25

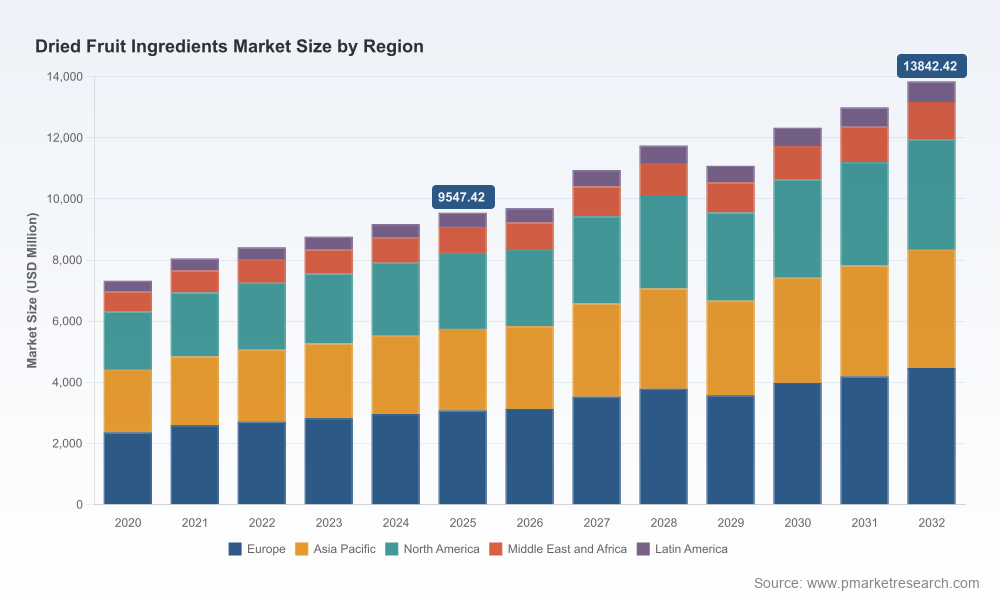

PW Consulting's latest Dried Fruit Ingredients Market report (base year 2025; historical 2020–2025; forecast 2026–2032) translates market complexity into executable strategy for manufacturers, ingredient suppliers, private equity investors, and brand owners preparing to act in 2026. The global dried fruit ingredients market has shown resilient expansion — from roughly USD 7.32 billion in 2020 to about USD 9.55 billion in 2025 — and is projected to continue on an upward trajectory to approximately USD 13.84 billion by 2032, implying a compound annual growth rate (CAGR) of 5.45% over the forecast window. This briefing explains why these headline numbers matter, what they hide, and how our report converts them into practical moves that preserve optionality and accelerate value creation.

Dried Fruit Ingredients Market

Defensive growth potential: As global consumers pursue cleaner labels, higher-fiber snacks, and convenient baking ingredients, dried fruit remains a core input that bridges indulgence and perceived health. The steady mid-single-digit CAGR through 2032 signals demand durability rather than a speculative spike — a foundation for portfolio allocation but not a guarantee of outperformance.

Dried Fruit Ingredients Market

Structural fragmentation: Market concentration metrics reveal a highly fragmented supplier base (CR3 ≈ 22.4%; CR5 ≈ 34.15%). That fragmentation creates multiple tactical opportunities — from bolt-on consolidation to capability-centric acquisitions — while elevating execution risk for buyers unable to integrate disparate supply chains and quality systems.

Dried Fruit Ingredients Market

Value-chain sensitivity: Raw material dynamics (grower returns, weather-driven crop swings, and region-specific tariff developments) and regulatory moves (labeling and sugar disclosure) materially influence margin mechanics and product positioning. 2026 will be a year where commercial agility and procurement sophistication separate winners from laggards.

Integrated demand model: A dynamic forecast engine that converts headline market growth into demand curves by use-case and channel under alternative scenarios (consumer premiumization, sugar-reformulation wave, and macro-economic slowdown). The model supports rapid re-forecasting around 2026 input-price shocks or trade-policy shifts.

Supplier heatmaps and due-diligence templates: We map processing capabilities, product form specializations (diced, pureed, low-moisture blends), food-safety track records, and export footprint across the supplier base — turning qualitative supplier intel into a procurement playbook for secure 2026 sourcing.

Margin and cost-to-serve diagnostics: A modular cost curve that isolates raw-material volatility, processing differentials (dehydration vs. low-moisture technologies), and logistics drivers so commercial teams can quantify the P&L impact of alternate sourcing or specification changes within weeks.

Regulatory and quality risk matrix: Actionable checklists aligned to current FDA labeling requirements and common recall scenarios. The module includes mitigation steps and communication templates adapted from recent industry cases.

Go-to-market playbooks for 2026: Product launch frameworks addressing clean-label positioning, sugar-reduced formulations, and co-manufacturing partnerships — each supported by consumer test designs and margin simulations to speed decision-making.

M&A prioritization and integration plan: A scored universe of strategic targets (scale processors, value-added ingredient specialists, and regional consolidators), plus an integration checklist that emphasizes traceability, SKU rationalization, and channel acceleration opportunities.

The supply side combines legacy cooperative brands and agile private processors. Several firms illustrate the set of strategic postures we see across the market:

Sun‑Maid Growers of California remains synonymous with large-scale raisin supply for food manufacturers — a brand-led scale player that benefits from deep grower ties and category recognition. Its position highlights the defensibility of integrated grower-to-processor models when managing raw-material volatility.

Sunsweet Growers demonstrates a successful product-innovation route to premiumization: recent launches focused on differentiated prune formats illustrate how heritage ingredient suppliers can create higher-margin, application-ready SKUs for baking and functional nutrition.

Ocean Spray Cranberries and Mariani Packing Company exemplify brand and quality plays into bakery, trail mix, and dairy adjacencies — underlining two pathways to commercial resilience: branded ingredient solutions and white-label specialty provision.

Regional processors such as Graceland Fruit, Traina Foods, and Monterey Bay Foods (Valley Fig Growers) showcase the competitive edge of capability specialization (e.g., diced low-moisture blends, sun-dried varietals, mission-fig processing). Their recent trade-show activity, certification updates, and targeted product launches indicate a market where incremental capability investments can unlock new customer relationships quickly.

Raw-material volatility: Grower economics and crop yields continue to matter. For example, recent reporting shows meaningful variation in per-ton grower returns and a decline in prune output tied to weather. These factors are likely to translate to concentrated price movements in 2026 unless manufacturers hedge or diversify their sourcing.

Regulation and labeling: The continued enforcement of nutrition-label updates (notably added-sugar disclosures) shifts product formulation calculus. Companies considering reformulation in 2026 should plan for a six-to-nine-month commercialization runway to align recipes, sensory testing, and claims substantiation.

Food-safety sensitivity: Recent recalls and enforcement actions in the category increase the value of rigorous upstream quality systems. Investors and acquirers should price potential remediation and certification investments into target valuations.

Trade policy and logistics: Tariff measures and evolving trade stances can re-route sourcing economics faster than production adjustments. Strategic inventory and flexible supplier networks are non-negotiable for 2026 resilience.

Procurement: Lock in tiered contracts with priority volumes but preserve optionality via indexed pricing clauses tied to key agricultural benchmarks. Begin test contracts for low-moisture processed blends to evaluate supply stability and cost impact.

R&D and reformulation: Initiate parallel reformulation tracks — one focused on sugar-reduction via ingredient substitution, another on premiumization (functional inclusions, clean-label preservation). Run pilot production under manufacturing control to stress-test shelf-life and sensory alignment.

Commercial: Deploy a channel segmentation exercise to map which accounts will value price stability vs. product differentiation, and craft tailored commercial terms for each cohort.

M&A and partnerships: Prioritize targets that offer either processing capability gaps (e.g., low-moisture dicing, puree integration) or footprint benefits in logistics-constrained corridors. Embed a post-acquisition integration checklist centered on traceability and SKU rationalization.

Risk & compliance: Update recall-response playbooks and accelerate certification roadmaps for suppliers with weaker food-safety track records. Consider third-party audits upfront to shorten integration timelines.

Speed: Our interactive forecast and cost models cut scenario assessment time from months to days, enabling rapid re-pricing of bids or bids for acquisition targets.

Precision: The report synthesizes supplier capability mapping with validated market sizing — empowering procurement and commercial teams to quantify trade-offs between cost, flexibility, and quality.

Practicality: Templates, checklists, and integration playbooks included in the deliverable are designed to be operational the week after purchase — not theoretical appendices to be interpreted months later.

This briefing intentionally highlights the strategic contours and actionable implications without releasing the full segment-level tables, regional shares, or application-by-application breakouts contained in the complete report. Those detailed splits, supplier scorecards, and the interactive scenario workbook are proprietary elements that materially affect commercial and M&A valuations. For procurement teams, R&D leads, and investors preparing to move in 2026, accessing the full report grants the exact inputs and templates required to convert the market’s steady growth into measurable margin expansion and risk mitigation.

To receive the full Dried Fruit Ingredients Market report — including the supplier heatmaps, full segmentation tables, interactive demand model, and prioritized M&A targets — contact PW Consulting. Our analysts are available to walk through the forecast engine and tailor the deliverable to your 2026 decision calendar.

For detailed analysis of this topic, please visit the official page:Dried Fruit Ingredients Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com