The Role of PSIRF Independent Investigations in Improving Patient Safety

Other |

2026-04-11 05:59:01

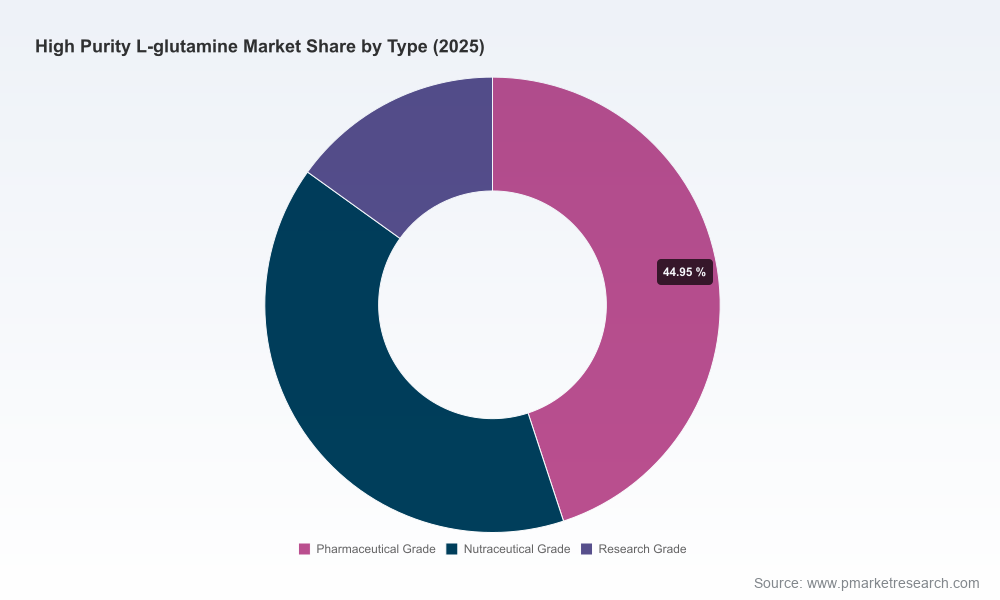

PW Consulting’s latest High Purity L‑Glutamine Market report (base year 2025) offers a forward‑looking, actionable intelligence package designed to inform C‑suite and procurement strategy throughout 2026. The market has expanded from roughly USD 172 Million in 2020 to an estimated USD 245.5 Million in 2025, and our scenario‑anchored forecast points to continued expansion at a 7.91% CAGR through 2032, when global revenues are modeled to approach USD 418 Million. These headline metrics frame a market that is maturing in scale yet remains strategically fragmented across quality tiers, application end‑uses, and regional supply chains—making 2026 a pivotal year for positioning.

High Purity L Glutamine Market

Executives face a short and decisive window to align sourcing, manufacturing investments, and regulatory hedges. The compound growth rate and the multi‑year revenue trajectory signal sustained demand across biologics, clinical nutrition and specialty supplements, but beneath that macro growth lie supply sensitivities (feedstock cyclicalities, concentrated cGMP capacity) and rising regulatory scrutiny. Our report translates those complexities into board‑ready recommendations: where to de‑risk supplier portfolios, when to accelerate qualification of secondary suppliers, and which vertical integration moves are justified by demand visibility and margin dynamics.

High Purity L Glutamine Market

These aggregate markers justify medium‑term investments but necessitate a disciplined supplier strategy to manage concentration and quality risk.

High Purity L Glutamine Market

For commercial teams, the implication is clear: market access and margin capture will increasingly favor suppliers and customers that can credibly demonstrate regulatory traceability, consistent low‑impurity supply, and multi‑jurisdictional filings (e.g., USDMF/CEP/JDMF). Procurement playbooks must reflect that quality certification is a primary selection filter—not a secondary checkbox.

Fermentation‑based manufacture accounts for the overwhelming majority of global production. This model ties L‑glutamine output to agricultural feedstock dynamics (e.g., glucose and starch), which in turn creates episodic cost volatility and inventory swings. Industry sources show upstream glutamic acid and related feedstock pricing remain a margin lever for producers; a recent softening in feedstock pricing is already being reflected in producer inventory strategies.

Concurrent with raw material volatility, we observe targeted capacity expansions among major players seeking to secure high‑spec output. Notable recent developments include accelerated overseas capacity investment by large Chinese producers and new high‑purity product introductions by regional manufacturers. These moves will influence the available pool of cGMP‑grade and low‑endotoxin material over the next 12–24 months and will be central to supply planning in 2026.

The market comprises a blend of global specialty chemical and amino‑acid leaders, regional scale producers, and niche cGMP specialists. Key strategic archetypes include:

Company‑level differentiation is driven by certifications (cGMP, low‑endotoxin/low‑metals designations), regulatory filings, geographic risk exposure, and the ability to guarantee lot‑to‑lot consistency for cell culture and injectable applications. For decision‑makers, supplier selection should weight certification depth and logistics resilience above headline price.

Regulatory measures and trade policy are shaping procurement calculus. Ongoing US trade measures and investigations relating to pharmaceutical imports introduce tariff and classification uncertainty for amino acids and associated intermediates. In parallel, exemptions and carve‑outs for certain dietary supplements have been signaled, but final outcomes remain fluid.

Companies should treat regulatory trajectory as a scenario planning variable in 2026: model landed cost under differing tariff regimes, evaluate onshoring or nearshoring for critical grades, and prioritize suppliers with multiple qualified manufacturing sites and clean compliance histories.

The market displays moderate concentration: leading suppliers control a meaningful share of high‑spec capacity, especially for pharmaceutical and cell culture grades. This structural reality amplifies the impact of single‑site outages, quality holdbacks, and regulatory detentions. Conversely, it creates opportunities for strategic entrants or contract manufacturers who can credibly certify quality and scale.

Operationally, the primary risk vectors for buyers and producers in 2026 will be:

The report is a hands‑on toolkit for strategy teams and procurement heads. It includes:

In keeping with our “trailer” approach, this press summary highlights the strategic contours and practical utility of our work; detailed segment tables, supplier rankings and transaction targets are intentionally reserved for readers of the full report.

High‑purity L‑glutamine sits at the intersection of growing therapeutic demand and supply‑chain complexity. Our 2026 guidance is straightforward: treat quality and regulatory pedigree as the primary contract levers, stress‑test supply under trade policy scenarios, and pursue supplier diversification early in the year. PW Consulting’s full report provides the granular segmentation, supplier rankings and transaction playbooks to execute those recommendations with precision. For procurement, manufacturing strategy and M&A teams preparing 2026 budgets and roadmaps, this intelligence should form a core input to capital allocation and supplier risk mitigation plans.

Access to the full dataset, supplier scorecards and executable 12‑month roadmaps is available through the PW Consulting report portal; readers seeking to operationalize these findings for 2026 planning should consult the full report for the proprietary segment tables and supplier‑level detail that are withheld from this public summary.

For detailed analysis of this topic, please visit the official page:High Purity L Glutamine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com