Critical Care Diagnostics Innovation Accelerating the Blood Gas and Electrolyte Market

Networking |

2026-06-17 09:42:38

PW Consulting’s latest market study on T Dodecyl Mercaptan (TDM) provides a focused strategic compass for corporate leadership, procurement teams, and investors preparing for 2026. Built on a 2020–2025 historical base and a 2026–2032 forecast horizon, the report synthesizes demand drivers, supply dynamics, regulatory shifts, and competitive positioning into actionable guidance. The market exhibits steady expansion from a mid‑2020s baseline and is forecast to grow at a compound annual growth rate (CAGR) of roughly 4.21% through the 2026–2032 period. Market concentration is meaningful, with the three largest suppliers controlling a clear majority of capacity and the top five suppliers representing a dominant share — dynamics that materially affect sourcing, pricing leverage, and M&A strategy.

T Dodecyl Mercaptan Market

Procurement optimization: The market’s modest but sustained growth and concentration create a supplier landscape where long‑lead contracts, dual‑sourcing strategies, and quality specifications (purity/grade) are decisive in cost and reliability outcomes.

T Dodecyl Mercaptan Market

Product portfolio planning: TDM’s role as a chain transfer agent and specialty intermediate ties its demand to polymer markets and lubricant additive formulations; understanding where polymer demand is accelerating will shape investment priorities.

T Dodecyl Mercaptan Market

Regulatory compliance and de‑risking: Stringent chemical safety frameworks and increasing scrutiny on sulfur compounds mean that compliance costs and handling requirements must be folded into 2026 capex and operating budgets.

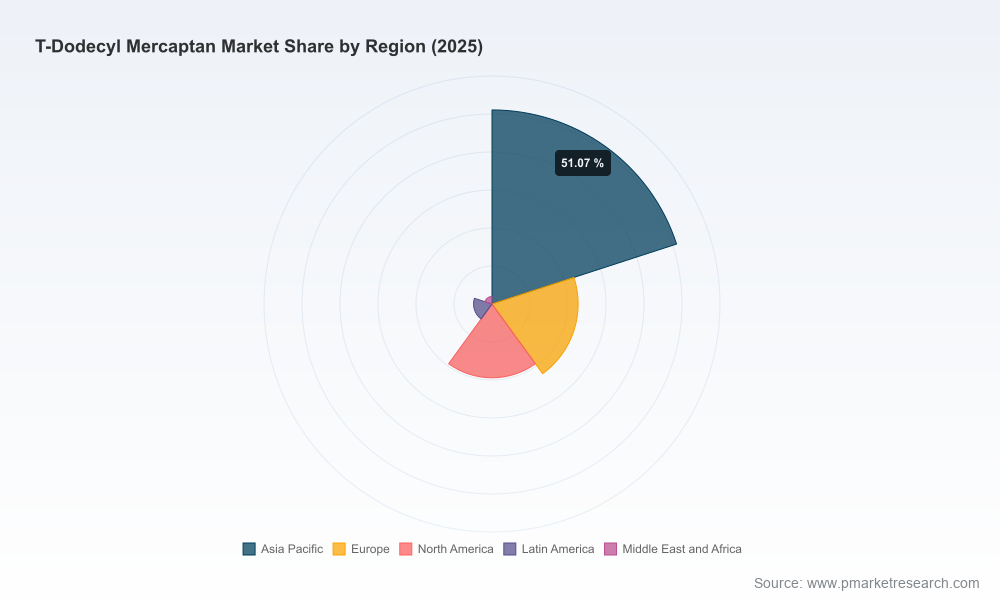

Using 2025 as the base year, the TDM market shows a trajectory of steady expansion into the early 2030s. PW Consulting’s top‑line model indicates the industry is set to continue growing at an approximate mid‑single digit CAGR across the forecast window, driven by incremental demand from emulsion polymerization processes, rubber and ABS polymers, and specialty additives. Importantly, this growth is not uniform; pockets of accelerated demand are tied to region‑specific polymer investments and shifts in lubricant formulation requirements. The combination of moderate demand growth and above‑average market concentration creates scenarios where localized supply disruptions or feedstock price shocks can transmit quickly through regional supply chains, producing outsized commercial impacts.

Comprehensive market model: A transparent, drill‑down financial model covering historical volumes and values (2020–2025) and a scenario‑based forecast (2026–2032) with sensitivity levers for feedstock cost, downstream polymer demand, and substitution risk.

Supply‑side mapping: Facility and capacity overlays (primary producers, specialty players, and geographic footprints), plus a supplier reliability matrix that scores purity capability, scale, lead times, and packaging/handling options.

Procurement playbook: Negotiation levers, contract constructs (take‑or‑pay, floor/ceiling pricing), and a recommended dual‑sourcing approach calibrated to supplier concentration and purity requirements.

Pricing and margin analytics: Rolling price decks and margin impact models that show how Q3 2025 feedstock moves might cascade into feedstock‑sensitive products like TDM under different pass‑through regimes.

Quality & application matrix: Practical checklists for selecting grade (high purity vs standard), compatibility testing protocols for polymer and additive applications, and mitigation steps for odor and emissions at formulation plants.

Regulatory compliance toolkit: An actionable checklist mapped to REACH and TSCA expectations, including labeling, storage, emissions controls, and audit priorities for 2026 inspections.

M&A and partnership screening: A short‑list methodology for identifying bolt‑on targets and JV partners, including valuation stress tests that account for capacity flexibility and regulatory remediations.

The TDM producer set combines large chemical majors with dedicated specialty manufacturers. Each archetype brings distinct strategic implications for buyers and investors:

Integrated majors (example profile): Large petrochemical firms supplying TDM often leverage scale, established distribution networks, and multi‑product contracts. Their strategic advantage lies in price stability and logistical reach, but buyer leverage can be limited where capacity is constrained.

Specialty producers (example profile): Firms focused on ultra‑high purity grades or tightly controlled production processes are attractive partners where performance and regulatory conformance are prioritized. They command premium pricing but offer lower risk for sensitive formulations.

Regional suppliers (example profile): Domestic or regionally focused manufacturers provide shorter lead times and nimble packaging/logistics options; however, their exposure to local feedstock pricing and tighter capacity utilization can introduce volatility.

Notable industry names exemplify these archetypes. Some players emphasize broad industrial scale and multi‑use product portfolios, while others focus on ultra‑high purity and specialty packaging tailored for emulsion polymerization and fine chemical uses. Recent capacity moves and public product positioning underscore a market where quality differentiation and proximity to downstream polymer hubs are critical competitive levers. One leading specialty chemical firm completed a capacity expansion in mid‑2025 to address growing polymer and specialty chemical demand — a development that has implications for lead‑time risk and regional price dynamics.

TDM production is rooted in a well‑defined chemical route that couples sulfur chemistry with propylene oligomers. Consequently, feedstock economics — notably propylene tetramer (dodecene) and upstream naphtha/propane/propylene pricing — directly influence manufacturing cost and spot availability. In Q3 2025, upward pressure on naphtha, propane, and propylene costs materially increased producer input costs, tightening margins for merchant suppliers without integrated feedstock positions. For 2026 planning, buyers should model multiple feedstock scenarios, prioritize contractual protections for price pass‑through, and evaluate buffer inventory and regional sourcing options to mitigate short‑term spikes.

Regulatory regimes in core markets are intensifying oversight of sulfur‑containing intermediates. Steps to comply with frameworks such as REACH in Europe and TSCA in the United States now routinely include enhanced labeling, more stringent handling protocols, tighter emission controls, and higher expectations for supplier traceability. Companies should anticipate increased compliance costs and potential delays for new product introductions unless supply partners demonstrate documented controls and audit readiness. Our report includes a compliance roadmap to quantify likely capex and operating expenditures associated with expected 2026 regulatory audits and reformulated handling requirements.

Reassess supplier segmentation: Classify suppliers not only by price and capacity but also by grade capability, regulatory readiness, and proximity to critical polymer hubs. Treat high‑purity capability as a strategic attribute for products destined to sensitive applications.

Secure flexible contracts: Negotiate contracts that include explicit feedstock pass‑through mechanisms, price collars, and volume flex to protect against the observed upstream volatility.

Invest in compliance and handling: Allocate near‑term capex to odor control, emissions mitigation, and storage upgrades to align with tightened regulatory expectations and to avoid downstream shutdown risk.

Pursue targeted partnerships: Evaluate minority equity stakes or JVs with specialty producers that bring high‑purity capabilities or regional manufacturing presence to lock in quality and shorten lead times.

Scenario test product portfolios: Use our provided sensitivity models to stress‑test margins and go/no‑go decisions for new formulations that require TDM, prioritizing those with higher margin memory under adverse feedstock scenarios.

In keeping with the “teaser” design of this release, PW Consulting intentionally omits detailed split tables and proprietary segmentation figures (regional and application shares, grade‑level revenue breakdowns, and per‑supplier volume statistics). These data sets and the underlying Excel models are included exclusively in the full report and accompanying data package available through our website. The withheld details are essential for transaction diligence, procurement negotiations, and capital allocation modeling; accessing them is the recommended next step for teams making binding commitments in 2026.

The TDM market in 2026 presents a mix of opportunity and complexity: steady top‑line expansion, meaningful supplier concentration, feedstock‑linked cost exposure, and tightening regulatory expectations. PW Consulting’s report turns these market realities into operational playbooks — from procurement frameworks to compliance toolkits and M&A screening processes. For organizations that need to convert market insight into defensible 2026 decisions, the full report (with data models and supplier scorecards) is the indispensable resource.

To obtain the full study, data models, and supplier benchmarking tools, please consult the PW Consulting report portal. Access to the complete dataset will enable you to perform the tailored scenario analysis and commercial negotiations that the 2026 planning cycle demands.

For detailed analysis of this topic, please visit the official page:T Dodecyl Mercaptan Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com