Candida Infections Drugs Market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-06-02 05:37:47

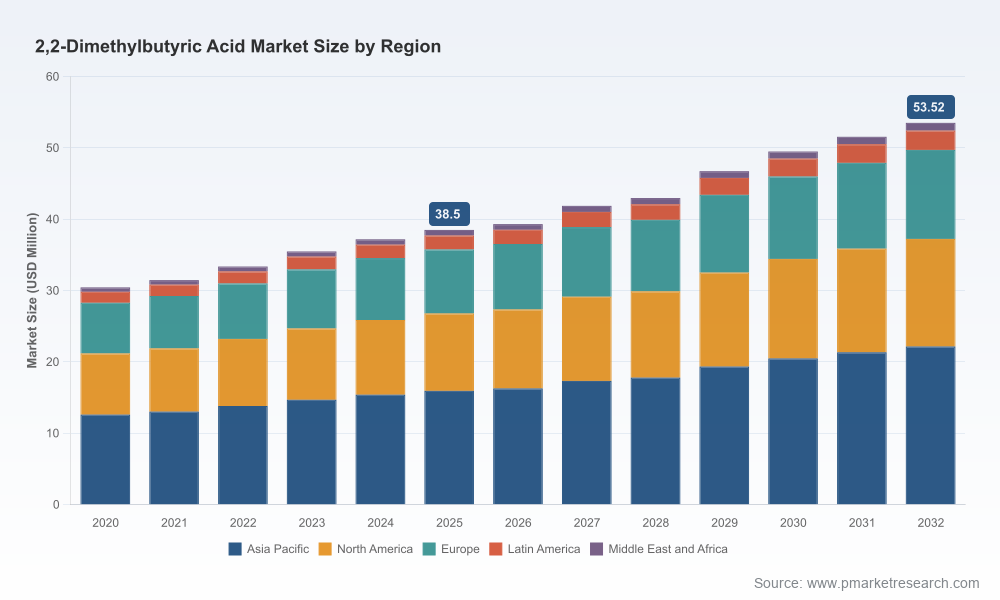

PW Consulting’s latest market study on 2,2‑Dimethylbutyric Acid (DMBA) provides an operationally focused, decision‑grade perspective for industry leaders preparing for the pivotal 2026 planning cycle. The global market is on a steady ascent — expanding from a measured base in 2020 through 2025 and forecast to continue growing through 2032 at a compounded annual growth rate (CAGR) of approximately 4.82% (USD, Million). Our base year is 2025, and the model projects robust year‑on‑year enlargement of the addressable market into the early 2030s. While this release highlights the principal dynamics, competitive posture, and actionable implications, core segmented figures and granular regional/application splits are intentionally reserved for the full report to support commercial confidentiality and to drive targeted engagement.

22 Dimethylbutyric Acid Market

PW Consulting’s model quantifies the DMBA market using a demand‑side top‑down approach validated against supply inventories, trade flows, and company filings. From the 2025 baseline, our central case projects continued expansion through 2032, with incremental acceleration driven by upstream supply rationalization and sustained demand from pharmaceutical intermediates and select specialty chemical applications. The market’s compound growth of ~4.82% over the forecast period indicates predictable, investment‑grade demand — an environment where disciplined players can capture outsized returns by aligning capacity, quality, and route economics.

22 Dimethylbutyric Acid Market

Our technical review traces multiple commercially relevant synthesis routes, each with distinct raw material, impurity, and capital expenditure footprints. Two process archetypes currently observed in patent literature and supplier disclosures are especially notable:

22 Dimethylbutyric Acid Market

Choice of route materially affects working capital, yield profile, and environmental footprint. The full report contains comparative process economics and a matrix mapping capital intensity versus achievable assay and impurity spectrum — necessary inputs for mid‑cycle capex decisions.

Trade policy remains a practical determinant of landed cost and time to market. DMBA is classified in global tariff nomenclature under the saturated acyclic monocarboxylic acids categories used by customs authorities. For example, recent tariff and supervision regimes in major producing jurisdictions introduce both an ad valorem component and documentary inspection requirements for imports and exports — a combination that can add weeks to lead times and create working capital drag. Procurement teams should incorporate tariff timing and certification lead times into reorder point calculations rather than treating them as static percentages.

The DMBA market exhibits a concentrated supplier structure. The top three manufacturers account for a majority share of global supply capacity, and the top five consolidate a significant portion beyond that — a structure that creates both supply resilience risks and opportunities for premium pricing for differentiated quality. The CR3 and CR5 metrics in our study quantify this clustering and are central to our supply risk heatmaps.

Key industrial participants profiled in the PW Consulting study include regional producers and specialty suppliers with differing commercial strategies:

PW Consulting’s profiles synthesize capacity footprints, certification status, and go‑to‑market arrangements. For example, one established manufacturer reports annual capacity for related dimethylbutyric derivatives at industrial scale — an important indicator of potential export supply dynamics and contract‑manufacturing opportunities. The full profiles in the report include supplier scorecards and negotiation playbooks tailored to buyer size and technical requirements.

For executives building 2026 plans, PW Consulting recommends a prioritized set of actions framed around three commercial objectives: secure quality supply, optimize unit economics, and preserve strategic optionality.

Executives should treat the PW Consulting DMBA study as a decision‑support toolkit for three boardroom questions likely to dominate 2026 planning: (1) Where should we allocate incremental capital in specialty chemistries? (2) How do we restructure procurement to balance cost and regulatory risk? (3) Which M&A or alliance options create defensible scale and technical differentiation?

Our condensed executive dashboards enable scenario testing within minutes, while the full technical annexes provide the evidentiary basis for capital appropriation and contract negotiation. Organizations that adopt a systematic, data‑driven approach — combining supplier scorecards with process economics — will gain negotiating leverage and reduce execution risks.

DMBA represents a stable and strategically important specialty chemical category with clear pathways for value creation through supply optimization, targeted capex, and smart commercial contracting. The market’s measured CAGR and concentration profile create an environment where disciplined players can capture durable margins, provided they act on the technical, trade, and commercial levers identified in this study. PW Consulting’s full 22‑page operational report (plus technical annexes and interactive models) contains the proprietary segmentation, supplier scores, and numeric detail necessary to convert insight into execution — information we intentionally withhold from this preview to preserve client value and encourage direct engagement.

For access to the full dataset, supplier scorecards, and the 2026 scenario workbook, please visit the official PW Consulting market page or contact our industry desk to schedule a briefing.

For detailed analysis of this topic, please visit the official page:22 Dimethylbutyric Acid Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com