Fat melting injection in Dubai: The Science of Injectable Lipolysis

Health |

2026-05-07 07:12:09

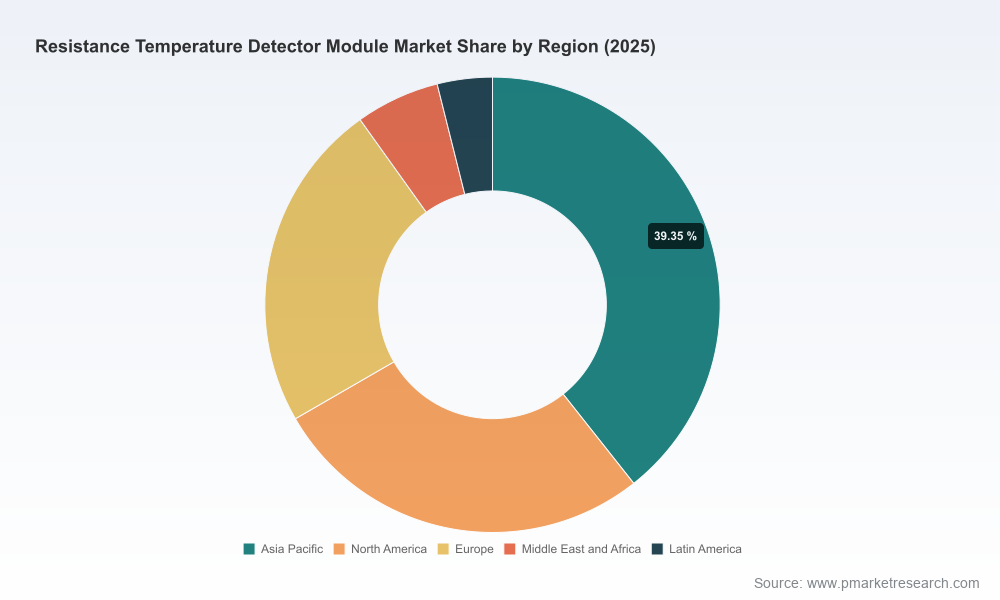

As industrial automation and process control systems deepen their reliance on precision temperature sensing, the Resistance Temperature Detector (RTD) Module market has moved from niche instrumentation to a strategic component of digital transformation roadmaps. PW Consulting’s latest market research positions the RTD module landscape as a resilient, steadily expanding sector — a market estimated at roughly USD 751 million in 2025 and forecast to grow at a compound annual growth rate (CAGR) of 5.18% through 2032, reaching approximately USD 1.07 billion by the end of the forecast window. For executives planning capital allocation, product roadmaps, or M&A activity in 2026, this research provides the prioritized intelligence required to convert ambiguity into advantage.

Resistance Temperature Detector Module Market

Actionable foresight, not just numbers: Beyond headline growth, the report extrapolates the demand vectors (automation upgrades, retrofit cycles, and new-build process plants) and maps them to measurable supplier and channel risks, giving procurement and product teams a tactical view of where to deploy scarce resources in 2026.

Resistance Temperature Detector Module Market

Risk-adjusted scenarios for supply and input costs: With platinum-based thin-film elements and Pt100 sensors remaining critical inputs to RTD modules, companies need scenario models that quantify the impact of raw-material shifts and standards-driven redesign. Our forecast embeds sensitivity analyses so decision-makers can stress-test capex and pricing strategies.

Resistance Temperature Detector Module Market

Competitive and regulatory posture: The market is neither perfectly fragmented nor oligopolistic — leading vendors capture a material share of value — meaning that moves by tier-one suppliers (product launches, platform partnerships, or standard compliance efforts) will have outsized influence. The report synthesizes competitor positioning and regulatory touchpoints to guide strategic countermoves.

Proprietary market model: An interactive base-year model (2025) with annualized revenue trajectories for 2026–2032, including scenario toggles for demand shocks, raw-material price swings, and accelerated automation adoption. This is designed for CFOs and strategy leads to re-run forecasts under corporate assumptions.

Deliverable playbook for procurement and product teams: Supplier scorecards, a standardized RFQ template focused on RTD module critical-to-quality metrics, and a seven-point checklist for platinum-element sourcing to reduce NPI lifecycle risk.

Commercial engagement frameworks: Recommended pricing bands and channel strategies for product managers entering adjacent markets (e.g., HVAC, food & beverage instrumentation). These frameworks are accompanied by customer-value maps that translate measurement accuracy, response time, and stability into ROI for end customers.

M&A and partnership shortlists: A prioritized list of targets and integration archetypes (technology tuck-ins, geographic expansion, and channel acquisition). Each target is scored against defensibility metrics, integration complexity, and expected time-to-value.

Standards and compliance checklist: Practical guidance to align product development with IEC 60751 and ASTM 3711 requirements, along with a roadmap for certification testing and documentation best practices.

Supply-risk heatmaps and mitigation playbooks: Supplier concentration analysis for critical inputs, single-source exposure flags, and three-tiered mitigation strategies (redundant sourcing, design substitution, and hedging tactics).

Input-material pressures and substitution economics: Platinum thin-film elements remain central to performance and interchangeability. The broader thin-film platinum sensor market is measured in the multi-billions and exerts upward pressure on module bill-of-material costs when cycle-driven metal supply imbalances occur. Companies that can engineer packaging and conditioning solutions that reduce platinum mass without compromising accuracy will unlock durable margin advantage.

Standards-driven differentiation: IEC 60751 (alongside ASTM 3711 for certain implementations) continues to define interchangeability and accuracy classes. Vendors who align early with these standards — and who can demonstrate robust linearization and stability in signal-conditioning modules — will gain both OEM trust and aftermarket traction.

System-level integration: Growth is less about raw sensing and more about integration into PLC/DCS ecosystems and edge controllers. RTD modules that offer deterministic behavior, isolation, and compatibility with prevalent I/O architectures are seeing preferential selection by systems integrators and end users focused on uptime and data quality.

The competitive field includes long-established sensor specialists, industrial automation giants, and niche module designers. Key strategic observations from our vendor review:

Specialist sensor manufacturers (e.g., companies with deep RTD probe and element portfolios) maintain advantage on component quality and customization. Their offering strength lies in Pt100/PT-series expertise and the ability to deliver assemblies tailored for high-reliability sectors such as aerospace, defense, and pharmaceutical manufacturing.

Industrial automation incumbents (large PLC/DCS vendors) compete on system compatibility and channel reach. Their RTD input modules are optimized for rapid integration into control architectures and benefit from bundled procurement by large end users and EPC firms.

Signal-conditioning and isolation specialists focus on linearization, surge protection, and electromagnetic robustness. These suppliers are winning specification-level decisions where signal integrity under harsh electrical or thermal environments is a priority.

Niche module designers and ruggedized scanner makers differentiate by enabling RTD deployment in harsh and mobile environments, such as engine monitoring and field-test rigs — a niche with different reliability and form-factor imperatives than factory automation.

Across these archetypes, the market exhibits a recognizable concentration dynamic: a set of well-resourced incumbents capture a sizeable portion of value while a long tail of specialized players competes on differentiation, customization, and service. For 2026, this implies that strategic choices — whether to compete on low-cost commoditized modules, to pursue higher-margin integrated system offerings, or to pursue bolt-on technologies — must be informed by clear answers on channel reach, engineering capabilities, and service economics.

Align R&D to standards-driven performance: Prioritize investments in linearization algorithms, isolation techniques, and calibration processes that demonstrate measurable improvements against IEC 60751 classes. These are defensible features that translate to premium positionings.

De-risk platinum exposure: Where possible, pursue design strategies that lower platinum mass or allow for validated alternative element types while preserving interchangeability. Negotiate medium-term offtake or hedging arrangements with critical-material suppliers to protect gross margins.

Prioritize system-compatibility partnerships: If you are a sensor or module provider, forming certified integrations with major PLC/DCS platforms accelerates enterprise adoption. Conversely, automation OEMs should consider selectively acquiring sensor specialists to internalize margin and secure supply.

Layer aftermarket services onto hardware: Calibration-as-a-service, lifecycle monitoring, and expedited replacement programs are routes to recurring revenue and customer stickiness in an otherwise product-centric market.

When evaluating M&A, favor targets with documented test-rig assets, repeatable qualification procedures, and engineering talent capable of compressing NPI cycles — assets that reduce time-to-market for standards-aligned modules.

In line with our “trailer” principle, this press release showcases the strategic depth and practical utility of PW Consulting’s RTD Module Market report while deliberately withholding granular regional and application-level splits and proprietary supplier financials. Those granular breakdowns are embedded in the full report’s interactive model and are essential for transactional diligence, site-level procurement planning, and precise target prioritization. If you are a corporate strategy, procurement, or product leader preparing decisions in 2026, accessing the full dataset will enable you to translate the broad recommendations above into executable initiatives with quantified impact.

Month 1 — Diagnostic: Use the market model to map your current product and revenue exposure against baseline and downside scenarios. Flag immediate supply risks and single-source dependencies impacting 2026 shipments.

Month 2 — Tactical alignment: Execute prioritized sourcing conversations with alternative suppliers, validate calibration and certification processes against IEC 60751, and issue an RFQ using our standardized template.

Month 3 — Strategic moves: Finalize a go/no-go list for M&A or partnership targets, align R&D sprints to high-impact product enhancements, and commit to a pilot aftermarket calibration program to drive recurring revenue.

PW Consulting’s RTD Module Market report is engineered to be both a strategic compass and a practical toolkit for companies preparing to make consequential moves in 2026. To obtain the full interactive model, supplier scorecards, and the segmented forecasts that underpin our recommendations, request the full report and data package through PW Consulting’s market intelligence portal.

For detailed analysis of this topic, please visit the official page:Resistance Temperature Detector Module Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com