Global Rocking Chairs Market Size, Share & Growth Forecast (2026–2034)

Other |

2026-07-03 10:03:26

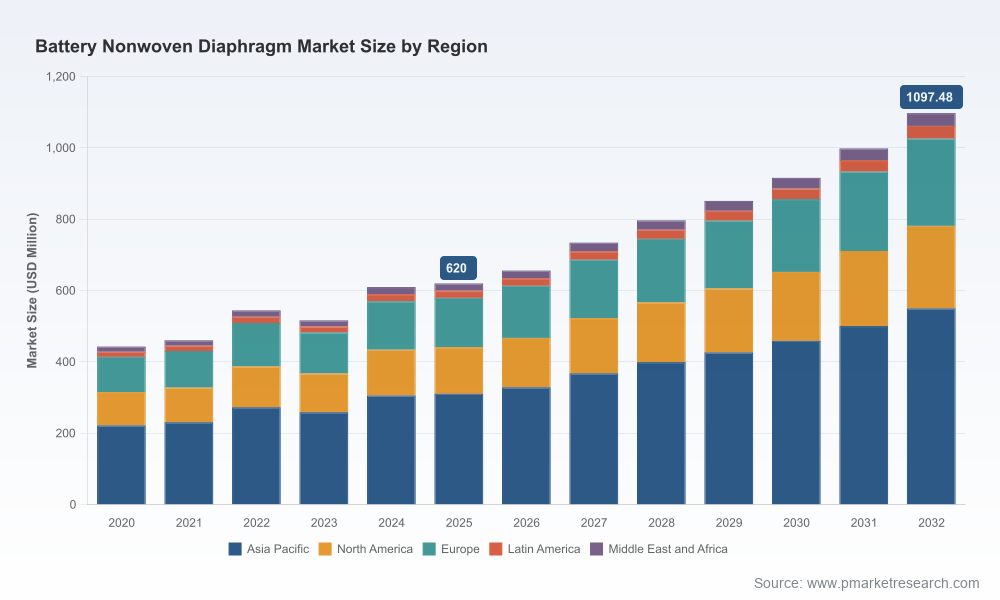

PW Consulting’s latest market study on the Battery Nonwoven Diaphragm Market provides a commercially actionable roadmap for executive teams preparing 2026 strategies. The market has expanded materially from an estimated USD 443 million in 2020 to roughly USD 620 million in 2025 (revenue in Million USD), and our base-case forecast projects continued momentum into 2026 and beyond — with the market moving to the mid‑600s Million USD in 2026 and a compound annual growth rate (CAGR) of 8.5% across the 2026–2032 forecast window. That trajectory reflects accelerating electrification, energy storage deployments, and technology shifts in separator architectures that are reshaping supplier economics and buyer priorities.

Battery Nonwoven Diaphragm Market

Investment timing: With the market growing at a high single‑digit CAGR, capacity additions announced today have a multi‑year revenue runway. Our analysis identifies when incremental capacity will meaningfully affect pricing dynamics and utilization rates.

Battery Nonwoven Diaphragm Market

Technology differentiation: Thermal stability, porosity control and surface coatings are migrating from R&D advantages to procurement must‑haves. Firms must decide whether to buy, co‑develop or build in‑house based on projected cell formats and regulatory thresholds.

Battery Nonwoven Diaphragm Market

Supply‑chain resilience: Raw material volatility and trade policy shifts are driving margin risk and sourcing complexity. The report quantifies exposure to feedstock price swings and provides mitigation playbooks for procurement and commercial teams.

Regulatory alignment: New regulatory baselines in major markets create compliance cliffs for some separator formulations; the report maps those cliffs to product roadmaps and identifies low‑cost compliance pathways.

We built the report to be execution‑oriented. Key components include:

Granular market sizing and a seven‑year forecast (2026–2032) with scenario modelling (base, upside and downside) that links demand trajectories to EV adoption curves, consumer electronics cycles and grid‑scale storage procurement waves.

Supply‑side mapping and manufacturing economics: plant‑level capacity, typical CAPEX/OPEX ranges, step‑cost profiles for wet and dry production routes, and a unit‑cost model you can plug your inputs into.

Technology and product taxonomy, including polyolefin‑based nonwovens, polyester variants and cellulose‑based alternatives — with an assessment of performance envelopes, manufacturability and likely upgrade paths through 2032.

Regulatory and standards matrix that translates multi‑jurisdictional requirements into product specifications and compliance timelines.

Commercial playbooks: procurement contracting templates, hedging and pass‑through mechanisms for feedstock price swings, and margin protection strategies for suppliers and OEMs.

M&A and partnership heatmap: target profiles for bolt‑on acquisitions, licensing candidates, and JV partners by capability and geography (note: the full report includes ranked candidate lists and valuation heuristics).

Client‑ready deliverables — slide decks, model extracts, and due‑diligence checklists to accelerate board and investor discussions.

Several near‑term dynamics should be priced into 2026 plans:

Feedstock pressure: Polypropylene, a common feedstock for many nonwoven diaphragms, experienced material cost inflation; industry reports show a ~12% year‑on‑year increase into late 2025. This has immediate implications for input cost pass‑through, supplier margin management and the attractiveness of alternative polymer or cellulose chemistries.

Policy and standards: The EU’s battery regulation establishes minimum ionic conductivity thresholds for automotive separators by 2027, which raises the bar for thermal and electrochemical performance across the supply chain. Simultaneously, Chinese standards now limit certain fluorinated additives — forcing reformulation decisions for suppliers targeting the domestic market.

Trade friction: Elevated tariff measures on imports from specific origins have altered landed cost calculations for many buyers. Where earlier models assumed free cross‑border flows, planners must now model effective cost with tariffs and evaluate near‑market capacity expansion as a strategic hedge.

Consolidation pressure vs. niche innovation: Market concentration at the top end of the value chain is meaningful, but pockets of specialised, safety‑focused entrants (notably in cellulose‑based separators) are progressing through certification and pilot stages, creating partnering or disruption scenarios.

We assessed the competitive positioning of leading global suppliers and innovators. Highlights that materially affect 2026 planning:

Asahi Kasei — strategic scale and capacity cadence: Asahi’s expansions to meet EV demand indicate a deliberate push to secure share in high‑power segments. Their investments in wet process Hipore production signal an approach that balances performance and scale economics.

Toray Industries — product performance focus: Recent launches targeting larger cylindrical formats underline a product strategy oriented to next‑generation cell formats and thermal stability enhancements — a clear answer to OEM demands for higher energy density and safety.

Sumitomo Chemical — integrated chemical‑to‑separator capability: Their upstream chemical expertise supports differentiated coatings and additive strategies that can compress supplier switching costs for customers seeking tailored separator solutions.

SEMCORP & Chinese players — scale and cost competitiveness: Large wet‑laid capabilities are being leveraged for high‑power applications. However, international buyers must factor tariff and compliance exposures into procurement frameworks.

Smaller innovators (e.g., cellulose‑based developers) — risk mitigation and product differentiation: Certification achievements by cellulose‑separator developers increase the optionality for safer chemistries in application niches where flame retardancy and environmental profile are prioritized.

Specialty nonwoven firms — advanced materials and process know‑how: Companies focused on tailored fiber architectures and coatings are positioned to win specification upgrades as OEMs push for higher thermal and mechanical resilience.

Market concentration metrics indicate the top few firms control a substantive portion of the market, but significant capacity remains distributed across regional players and newcomers. That split creates both consolidation opportunities and competitive threats depending on a buyer’s sourcing strategy.

Run a short‑cycle supplier stress test: Model supplier exposure to a 15%–25% spike in feedstock prices and to tariff scenarios. Translate results into contractual minimums and indexation clauses.

Define a modular sourcing playbook: Combine short‑term buy strategies (hedged contracts, spot coverage) with medium‑term options (capacity leases, toll manufacturing) and long‑term localization where tariffs and standards justify investment.

Invest in performance‑led R&D: Prioritize separator properties that map directly to regulatory thresholds and OEM cell formats (e.g., ionic conductivity and thermal integrity). Consider co‑development agreements with market leaders to accelerate qualification cycles.

Pursue selective M&A and JV routes: Acquire niche technology or secure downstream access in markets where tariffs and standards make imports expensive or uncertain.

Operationalize regulatory surveillance: Create a standards‑to‑specification pipeline so product development and procurement decisions are proactively aligned with compliance deadlines.

Prepare commercial hedges: Embed raw‑material pass‑throughs, formulaic price adjustments and service‑level protections into supplier contracts to stabilize margins across the supply chain.

For boards and executive committees, the study offers a concise evidence base linking market growth trajectories to investment and procurement choices. The report’s cost models enable rapid valuation of greenfield capacity versus contract manufacturing; its scenario outputs inform capital allocation and M&A prioritization; and its supplier scorecards accelerate due diligence. In short, this is designed as a decision support pack for 2026 — not an academic exercise.

This release serves as a strategic preview. To obtain the full dataset, ranked supplier lists, model extracts and the client toolkit (including slide decks and contract templates), please consult the PW Consulting Battery Nonwoven Diaphragm Market report page. The full report contains the granular regional and application breakouts, unit economics by process route, and the proprietary scenario models that we intentionally omit from this public summary to preserve analytical value for subscribers and clients.

PW Consulting combines sector‑specific industry analysis with transaction‑grade financial modelling. Our team of senior advisors and industry engineers is available to brief executive teams, run bespoke scenario workshops, and co‑develop supplier transition plans to support your 2026 strategy execution.

For detailed analysis of this topic, please visit the official page:Battery Nonwoven Diaphragm Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com