Advanced AI SEO Strategies Helping Businesses Grow in Singapore

Other |

2026-03-08 19:18:39

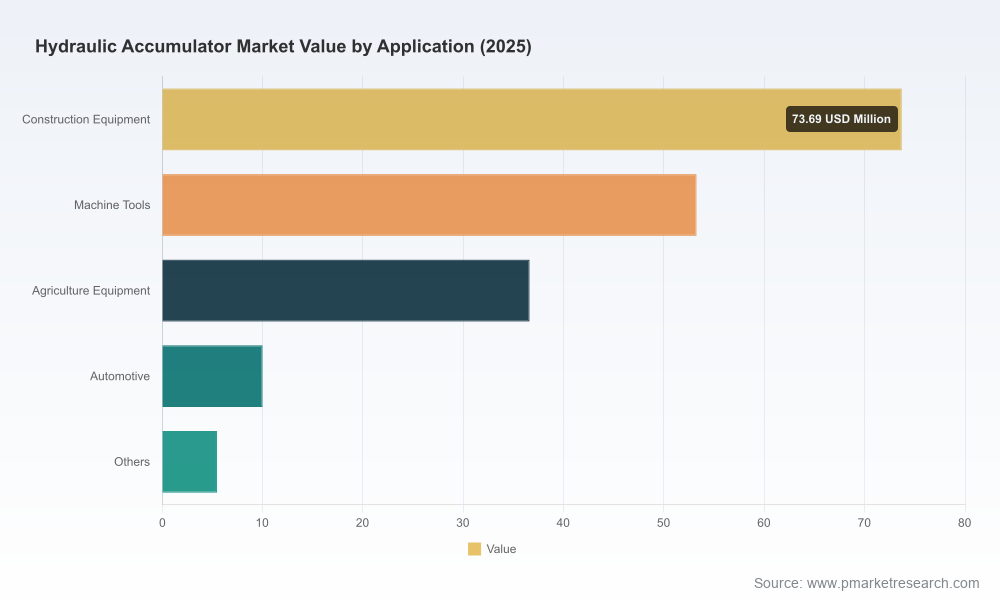

PW Consulting’s Hydraulic Accumulator Market study (base year: 2025; historical window: 2020–2025; forecast window: 2026–2032) synthesizes quantitative trajectories and qualitative dynamics that will shape winning strategies through 2026 and beyond. The market we track is denominated in USD (Million). From an overall market value of USD 130.0 Million in 2020 the sector expanded to USD 179.0 Million in 2025 and, under our baseline forecast, is projected to reach USD 262.0 Million by 2032 — implying a compound annual growth rate (CAGR) of 5.6% across 2026–2032. This preview highlights the strategic implications of those trends for executive teams, product leaders, and corporate development groups preparing decisions in 2026.

Hydraulic Accumulator Market

Validated growth trajectory: The sector’s steady expansion through 2020–2025 and the forecasted mid-single-digit CAGR into the next decade confirm that hydraulic accumulators will remain a growth market for both industrial and mobile hydraulics. That trajectory alters how executives should prioritize R&D, capacity planning, and aftermarket investments.

Hydraulic Accumulator Market

Regulatory and standards inflection points: Changes in transport authorization and persistent harmonized safety standards mean product compliance and certification strategies are now commercial levers — not just cost items. The report translates the practical impact of regulatory updates into timeline-driven requirements for product redesign, testing, and market entry.

Hydraulic Accumulator Market

Supply-chain and materials risk embedded in demand: Volatility in specialty steels and elastomers materially affects total cost of ownership and margin management. Our study quantifies sensitivity and lays out operational levers that firms can employ in 2026 to protect margins while remaining competitive on price and lead time.

The macro picture is decisive: growth is predictable but not uniform. The market rose from USD 130.0 Million in 2020 to USD 179.0 Million in 2025, reflecting recovery and investment cycles across construction, machine tools, agricultural and mobile platforms. With a 5.6% CAGR projected for 2026–2032, management teams should plan for a steady expansion of both OEM and aftermarket demand rather than a single, short-lived spike. That steadiness favors investments in reliability, certification, and service models that compound revenue over multiple equipment life cycles.

Note: this executive preview deliberately abstracts away granular regional and application splits — the full report includes the complete breakdown and time series for every major subsegment and region.

Regulatory developments become competitive differentiators. In November 2025, a substantive revision authorized seamless steel accumulators containing compressed nitrogen for commercial transport, easing certain logistics constraints for compliant products. Concurrently, international standards (EN 14359; DIN EN ISO 4413; PED 2014/68/EU) continue to govern essential design and safety attributes. Result: certification turnarounds, test-lab access, and documentation workflows will determine near-term market access and time-to-revenue.

Materials and TCO volatility. High-grade steel alloys and specialty elastomers have shown intra-year price swings of 15–25%, directly affecting bill-of-materials and aftermarket part economics. Companies that institute hedging, multi-sourcing, modular designs, or pass-through pricing models will have a measurable margin advantage.

Shifts in demand composition. End-market investments (e.g., mechanization of construction and agriculture, automation in machine tools) change product feature priorities: response time, energy recovery, lifecycle cost, and serviceability. These shifting priorities call for differentiated product roadmaps rather than one-size-fits-all portfolios.

Aftermarket and service as growth engines. With stable platform replacements and longer equipment lifecycles, aftermarket sealing kits, refurbishment programs, and predictive maintenance are prime levers for revenue growth and margin stabilization.

Validated historical market sizing (2020–2025) and a granular forecast (2026–2032) with scenario alternatives that stress-test commodity shocks, regulatory shifts, and macro slowdowns.

Segment-level analysis by technology type, application, and region with growth drivers, risk factors, and near-term inflection points. (Note: this preview omits the proprietary granular splits; they are contained in the full dataset.)

Detailed competitive landscape with profiles, capability maps, and an M&A scorecard for potential targets based on technology fit, channel access, and certification status.

Unit-cost and margin models that capture raw-material exposure, scale effects, and aftermarket economics — enabling pricing and contract negotiations under multiple cost scenarios.

Practical go-to-market playbooks for OEMs, component manufacturers, distributors, and service providers — including channel optimization, service bundling, and certification roadmaps.

Regulatory impact matrix outlining compliance timelines, testing requirements, and revenue risk for non-compliant SKUs.

The industry is populated by global OEMs, specialized regional manufacturers, materials suppliers, and independent testing houses. The firms profiled in our study include hydraulic incumbents and specialist players with complementary assets. Below is a synthesized view of core competitors and their strategic positions:

HYDAC International GmbH (Sulzbach, Germany) — broad product breadth across bladder, piston and diaphragm technologies with deep OEM relationships in industrial and mobile hydraulics. Strengths: engineering depth and global aftermarket footprint.

Parker Hannifin Corporation (Cleveland, Ohio, USA) — global scale and strong service and repair ecosystem; extensive product coverage and brand recognition make Parker a go-to partner for system integrators.

Danfoss Power Solutions (Nordborg, Denmark) — leverages Vickers-branded legacy with strong industrial positioning; notable for modular system offerings and OEM integration capabilities.

Bosch Rexroth AG (Korb, Germany) — engineering-led supplier of hydro-pneumatic accumulators with systems-level integration strengths, especially for automated factories and large-scale industrial systems.

Accumulators, Inc. (Houston, Texas, USA) — US-based specialist; recent regulatory development (transport authorization revision, Nov 2025) demonstrates the commercial value of regulatory engagement and certification leadership.

Freudenberg Sealing Technologies (Weinheim, Germany) — vertical strength in materials and sealing technologies; competitive advantage in certifications and materials engineering.

STAUFF AG, NOK Corporation, Eaton Corporation, Roth Hydraulics, SFP Hydraulics, Airline Hydraulics, Teutonic Engineering — a mix of regionally important manufacturers and material specialists whose strengths range from cost leadership and ISO-certified production to niche high-performance applications.

SGS Group — independent testing, inspection and certification provider whose services are increasingly critical as regulatory and transport authorizations become commercial differentiators.

Strategic takeaway: competition is defined less by who owns a single technology and more by who can combine product quality, certification velocity, materials sourcing, and aftermarket capability. For mid-market players, aligning with independent labs and securing transport and pressure-vessel authorizations can unlock distribution advantages.

Prioritize certification-led product roadmaps. Turn regulatory approvals into go-to-market advantages by integrating certification timelines into product launch planning and R&D budgets.

Hedge material exposure and redesign for modularity. Implement dual-sourcing for critical alloys and elastomers, and accelerate modular product variants to reduce retooling costs when raw-material costs spike.

Shift from one-time sales to service platforms. Bundle refurbishment, predictive maintenance, and certification renewals to capture lifetime value and soften cyclical demand fluctuations.

Use M&A selectively to buy certification and channel access. Acquire targets that deliver immediate regulatory clearances, testing capacity, or aftermarket logistics rather than only technology patents.

Commercialize regulatory expertise. Offer compliance-as-a-service to OEMs and end-users so that certification becomes a revenue-generating capability instead of a cost center.

Invest in digital twins and predictive diagnostics for accumulators. Operational transparency enables premium aftermarket pricing and reduces warranty expense.

For leadership teams mapping 2026 priorities, the central implication is clear: this market offers predictable growth, but competitive advantage will be determined by operational resilience, regulatory speed-to-market, and aftermarket capture. The full PW Consulting report provides the proprietary regional and application-level breakdowns, sensitivity modeling tied to material-price scenarios, and actionable M&A targets that will allow your organization to convert the forecasted 5.6% CAGR into sustained competitive returns.

To access the definitive dataset, scenario matrices, and company-level scorecards referenced in this executive preview, please consult the full Hydraulic Accumulator Market report on our site or contact your PW Consulting account lead. This preview is designed to orient 2026 decisions; the full analysis supplies the granular inputs required to translate that orientation into executable plans.

For detailed analysis of this topic, please visit the official page:Hydraulic Accumulator Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com