Embolization Particle Market: Strategic Briefing for 2026 Decision-Makers

As healthcare providers, device manufacturers, investors and payers prepare strategy for 2026, the Embolization Particle market demands a recalibrated playbook. Our PW Consulting market study (base year 2025) synthesizes clinical, commercial, regulatory and supply-chain signals into actionable intelligence. This briefing highlights why the market’s macro trajectory and competitive inflection points should be central to boardroom deliberations — while intentionally holding back granular segment matrices and price-sensitive splits to preserve the full report’s strategic value.

Embolization Particle Market

Market trajectory at a glance

Between 2020 and 2025 the embolization particle market expanded materially, reflecting accelerating adoption across interventional oncology and other vascular therapies. In 2025 (base year) global revenues reached a multi‑billion USD milestone (reported in USD Million), and our forecast sees continued momentum through 2032. The market is projected to grow at a compound annual growth rate of approximately 9.8% over the 2026–2032 forecast period, more than doubling aggregate revenues by the end of the horizon. Market concentration metrics show meaningful consolidation at the top: the three largest suppliers account for a plurality of revenue, while the top five capture a clear majority — a structure that both creates barriers and surfaces partnership opportunities for challengers.

Embolization Particle Market

Why this matters for 2026 choices

- Timing of investment: The combination of strong forecast CAGR and recent regulatory approvals makes 2026 a pivotal year to decide on capacity expansion, product launches, or selective acquisitions.

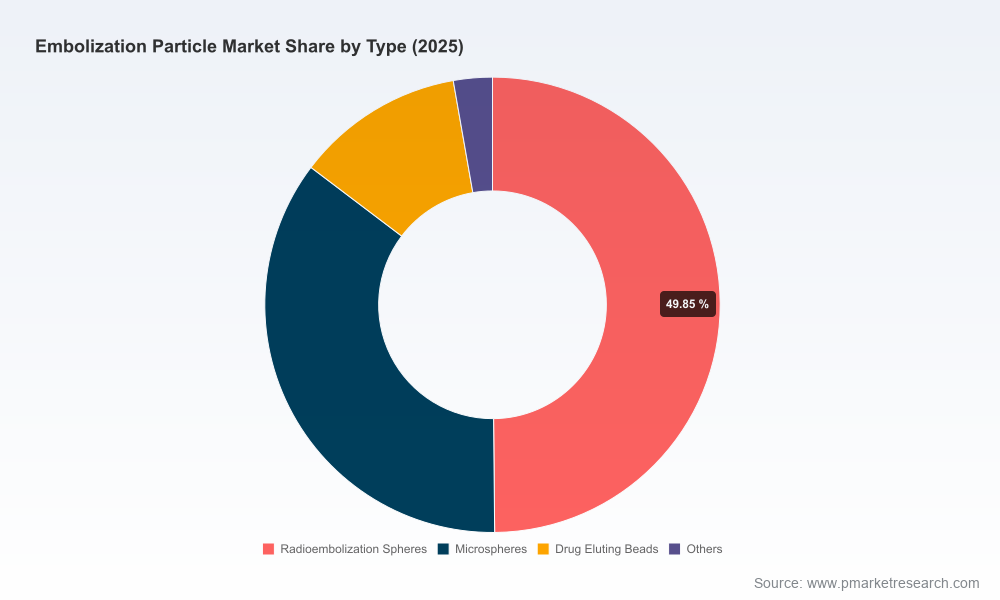

- Portfolio prioritization: Diverse technology stacks — radioembolization, microspheres (including drug‑eluting), PVA-based particles and resorbable gelatin platforms — require clear asset prioritization tied to clinical differentiation and reimbursement pathways.

- Regulatory arbitrage: Recent and pending device approvals reshape addressable markets and influence go‑to‑market sequencing for new entrants versus incumbents.

- Commercial models: With concentration among leading vendors, market access strategies (hospital contracting, OEM partnerships, KOL-led adoption) will determine share shifts more than incremental pricing.

What our full report delivers (practical, operational content)

- Market sizing and validated forecast (2026–2032) with scenario modelling and sensitivity to clinical adoption and reimbursement dynamics.

- Clinical & technology mapping: efficacy, safety profiles, and procedure‑level economics across particle types and delivery systems.

- Regulatory and reimbursement roadmaps by jurisdiction, including milestone timelines, likely approval headwinds, and coding implications.

- Supply‑chain and raw‑material risk assessment, including supplier concentration, sterilization standards and manufacturing scale considerations.

- Commercial playbooks: customer segmentation, decision criteria for hospitals and interventional suites, channel strategies and tendering behaviour.

- M&A and partnership screen: strategic targets, valuation multiples observed in adjacent interventional-device transactions, and integration playbooks.

- Competitive landscaping with capability matrices and battleground maps — deliberately presented to guide negotiations and counter‑positioning.

- Actionable 90‑, 180‑ and 365‑day plans tailored to manufacturers, distributors and new entrants.

Competitive landscape — synthesis and implications

The market is dominated by a mix of established medtech firms and specialized interventional oncology players. The competitive dynamic blends legacy product strength, IP around particle chemistry and delivery, and increasingly, regulatory momentum that changes addressable indications.

Embolization Particle Market

- Merit Medical Systems, Inc. — Strengths include a diversified portfolio across non‑resorbable PVA, microspheres and gelatin platforms. Product depth and a broad clinician install base create cross‑sell opportunities for adjunct devices and consumables. Strategic implications: incumbents with wide portfolios can leverage bundled procurement and training services to raise switching costs.

- Boston Scientific Corporation — A blend of PVA and advanced microspheres with established reimbursement resources; strong commercialization channels and EDUCARE platforms support clinician adoption. Strategic implications: scale and cross‑division synergies enable accelerated market penetration for newly cleared devices.

- Terumo Corporation — Noted for microsphere platforms with drug‑eluting options and CE‑marked products for multiple indications. Strategic implications: strong regulatory and distribution footprint in select regions makes Terumo a formidable regional partner or competitor.

- Sirtex Medical Limited — Focused leadership in radioembolization, with high‑impact trial results and regulatory wins that materially expand indication coverage. Strategic implications: clinical evidence (large trials with favourable endpoints) can rapidly reconfigure referral patterns and payer willingness to reimburse high‑value therapies.

- BTG plc / legacy LC Bead technology (now integrated with a major medtech portfolio) — Institutionalized microsphere technology that remains influential in drug‑eluting bead applications. Strategic implications: legacy IP and installed base are attractive for companies seeking rapid entry into drug‑eluting embolics.

- NextBioMedical Co., Ltd. — Emerging supplier with fast‑resorbable gelatin microspheres and targeted approvals that enable entry into new clinical indications. Strategic implications: nimble innovators with differentiated bioresorbable chemistries can capture niche segments and become attractive bolt‑on targets.

Recent regulatory and competitive events underscore these dynamics. Notable approvals and clearances in 2025–2026 have reshaped near‑term market access:

- Mid‑2025 FDA approval for a leading radioembolization Y‑90 resin microsphere program, supported by strong trial endpoints, heightens the clinical imperative to consider radioembolization as a first‑line locoregional option in select hepatic cancers.

- Late‑2025 510(k) clearances for PVA microsphere families expand the pool of devices available for AVMs and hypervascular tumors, increasing competition but also enlarging the procedural pie through broader adoption.

- Early‑2026 Health Canada approvals for novel fast‑resorbable gelatin platforms create a Canadian entry case study for regulatory strategy and early commercial rollout.

Regulatory, clinical and raw‑material realities to factor into 2026 plans

- Sterilization & standards: Key products adhere to established sterilization standards (e.g., NF EN ISO guidance) — a non‑negotiable for procurement and tender compliance. Manufacturers must validate sterile packaging and process controls early in product development to avoid launch delays.

- Raw materials: Polyvinyl alcohol (PVA) derivatives and novel hydrogel chemistries underpin most particle technologies. Supplier continuity, quality control and synthetic route intellectual property are strategic levers — shortages or quality events can cascade into capacity constraints.

- Reimbursement channels: Training and clinician education programs from leading vendors are paired with reimbursement support materials; this combination materially affects hospital adoption curves and procedure coding outcomes.

Practical strategic moves for 2026

- Portfolio triage: Immediately assess your product roadmap through a short‑list filter: clinical differentiation, reimbursement probability within 12 months, and manufacture‑to‑market lead time. Delay or spin out non‑core assets to conserve R&D spend.

- Evidence prioritization: Invest in one robust, indication‑specific clinical trial rather than multiple small studies. High‑quality evidence yields outsized commercial returns in reimbursement negotiations and KOL advocacy.

- Regulatory sequencing: Use early approvals (e.g., country‑specific 510(k)/MD/CE pathways) as beachheads to test commercial models and de‑risk larger jurisdiction launches.

- M&A & partnerships: Target bolt‑ons that fill material gaps (e.g., resorbable chemistries, Y‑90 delivery know‑how, or manufacturing scale). Leverage earn‑outs tied to regulatory milestones to align valuation to execution.

- Supply chain resilience: Secure multiple suppliers for critical polymers and secure sterilization capacity; negotiate long‑dated supply agreements with volume tiers and quality guarantees.

How to use the full PW Consulting report

Consider the full study as a decision‑support toolkit: it provides scenario decks for executive committees, a playbook for commercialization teams, a due‑diligence checklist for M&A, and a regulatory timeline that can be integrated into product launch calendars. The report intentionally omits public disclosure of granular segmentation splits in this preview — those slices are available in the full deliverable, where we present proprietary segment matrices, price curves, and region‑to‑indication flow models that underpin the forecasts.

Next steps

- For leadership teams assessing capital allocation in 2026: use the macro growth profile and concentration metrics to size investment thresholds and return hurdles.

- For commercial leaders: request the battleground maps and value‑selling playbooks to accelerate adoption within targeted hospital systems.

- For investors and corporate development: obtain the M&A target screen and financial comparables to inform bidding strategies and integration planning.

PW Consulting’s Embolization Particle Market study combines rigorous market modelling (historical 2020–2025, forecast 2026–2032), competitive forensic analysis and practical execution templates. For the full set of segment‑level data, appendices and downloadable decision tools, please visit our report page and engage with our practice leads to tailor the findings to your 2026 strategic roadmap.

For detailed analysis of this topic, please visit the official page:Embolization Particle Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com