Milled FerroSilicon Market — Strategic Preview for 2026 Decision-Makers

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present an executive preview of our latest Milled FerroSilicon Market research. This piece is designed as a high-value “trailer”: it demonstrates the analytical depth and strategic line-of-sight our full report offers for 2026 corporate planning, while intentionally withholding granular segment-level figures to encourage access to the full study for tactical execution.

Milled FerroSilicon Market

Market snapshot: a stable, disciplined growth story

Our analysis uses 2025 as the base year and covers historical performance from 2020–2025, with forecasts through 2032. The milled ferrosilicon market strengthened through the mid-decade, growing from an estimated USD 85.0 Million in 2020 to a USD 100.0 Million base in 2025. Against a backdrop of cyclical end-use demand and raw-material volatility, we forecast a compound annual growth rate (CAGR) of 3.3% over the 2026–2032 period, with the market climbing to roughly USD 125.6 Million by 2032 under the central case.

Milled FerroSilicon Market

Two points are critical for strategic planning in 2026:

Milled FerroSilicon Market

- Growth is steady, not explosive. The market’s trajectory supports conservative capacity investments, targeted product-positioning, and efficiency plays rather than broad capex expansions.

- Near-term variability is driven more by input-cost dynamics and trade policy than by abrupt demand shocks—meaning risk stack management (input, trade, regulatory) yields higher ROI than pure volume chasing.

Drivers and dynamics shaping 2026 strategy

We identify three structural forces that will shape strategic choices in 2026 and beyond:

- Input-price and cost-channel volatility: Raw-material and benchmark ferrosilicon pricing showed notable softening in 2025 across several hubs. These movements compress margins for producers that lack flexible sourcing or value-added product differentation, while advantaging producers with integrated feedstock access or advanced milling/quality control that command price premia.

- Trade and regulatory frictions: Recent regulatory actions — including country-specific tariff-rate quotas and anti-dumping determinations in major markets — are reconfiguring trade flows and elevating the premium on compliance-ready supply chains. Firms that proactively map tariff exposure and construct alternative logistics corridors will protect margin and delivery reliability.

- Concentration and competitive positioning: The market exhibits meaningful concentration at the top of the value chain. Aggregate concentration metrics indicate that the leading producers command a dominant share of available commercial supply. For challengers and mid-tier players, this reality focuses strategic options on niche specialization, cost leadership, or regional defensive plays rather than head-on capacity replication.

What this means for 2026 corporate decisions

For executive teams preparing budgets and strategic plans in 2026, the milled ferrosilicon market presents opportunities that reward precision. Below are the practical decision levers our research recommends prioritizing:

- Supply-chain resilience over capacity expansion: Given moderate CAGR and regulatory uncertainty, the best near-term investments are in supply-chain flexibility — multiple freight corridors, secured long-term feedstock contracts, and contractual clauses that account for duty changes — rather than large greenfield mills.

- Product and application differentiation: Margin expansion will come from differentiated milled grades and services (e.g., tighter particle-size control, specialty packaging, and technical support for dense media separation or inoculation applications). Those capabilities reduce price elasticity of demand for suppliers.

- Regulatory playbooks and market access hedges: Firms must maintain a live regulatory dashboard. Recent policy moves affecting import quotas and anti-dumping outcomes demonstrate that market access can change rapidly; building parallel sourcing and tariff-mitigation strategies will be decisive.

- M&A and alliance scouting: With high market concentration among the top players, strategic acquisitions and technical partnerships can be an efficient route to scale or capability acquisition—especially for firms seeking rapid entry into geographically protected or technically demanding niches.

- Pricing and contracting sophistication: Given raw-material price swings, transitioning from spot-only sales to hybrid contracts (index-linked with collars, partial fixed-price agreements, and value-based premiums for certified grades) will stabilize revenue and protect margins.

Competitive landscape — what to watch in 2026

Our study profiles an extensive set of market participants, from specialized powder suppliers to vertically integrated ferrosilicon producers. Key archetypes and representative names include:

- Specialists serving niche applications: Companies focused on dense media separation and powder technologies typically compete on product consistency, particle distribution control, and customer service. Their strategic playbook centers on technical partnerships with mineral processors and foundries.

- Regional producers with integrated feedstock: Larger, vertically integrated firms leverage captive raw-material access and scale economics to undercut competitors on delivered cost while maintaining broader customer reach and contractual stability.

- Major industrial groups and diversified metals players: These players incorporate milled ferrosilicon within a broader ferroalloy portfolio and often adopt portfolio optimization tactics—adjusting supply into milled or coarser forms based on margin signals.

Representative firms profiled in our competitive analysis include established names across geographies (Europe, China, India, Africa, North America and beyond). The profiles combine operational footprints, product portfolios, and go-to-market differentiation. We also map capability gaps and potential partnering vectors for market entrants. Notably, the top-tier concentration metrics underscore that the largest producers retain a dominant position, while a mosaic of regional and specialized suppliers represents the balance of competitive intensity.

Report contents — the operational intelligence you’ll use in 2026

The full PW Consulting report moves beyond high-level trends to deliver actionable modules for strategy teams and commercial leaders. Highlights include:

- Validated historical market sizing for 2020–2025 and a rigorous scenario-based forecast through 2032, enabling five decision-making horizons (short-term 12 months, medium-term 24–36 months, and long-term up to 2032).

- Trade-flow sensitivity and tariff-impact modeling that simulates the commercial effect of tariff-rate quotas and anti-dumping measures on landed costs and margin across major trading corridors.

- Practical procurement templates and contractual language options (indexation, collars, force majeure) tailored to mitigate input-price and duty risk.

- Competitive-advantage heatmaps and M&A candidate shortlists, scored by technical capability, geographic fit, and regulatory accessibility.

- Go-to-market playbooks for premiumization (specialty particle-size grades, technical services) and cost plays (logistics optimization, feedstock integration), complete with implementation KPIs.

- Operational checklists for producers and buyers to prepare for sudden shifts in feedstock availability and policy changes, including rapid scenario-response roadmaps.

Data integrity, methodology, and what’s intentionally withheld

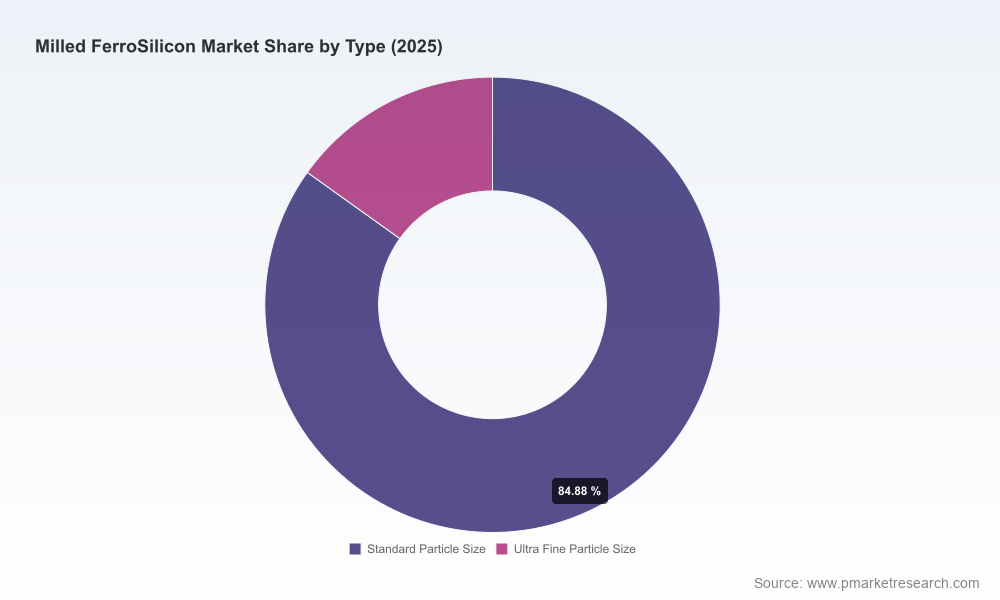

We built our market model on a combination of primary interviews, company financials, trade statistics, and price-monitoring datasets. The study’s base year is 2025 (reported in USD Million), and the forecast horizon is 2026–2032. To preserve competitive advantage for clients and to adhere to our “trailer” approach, the public preview avoids publishing granular, disaggregated subsegment values and region/application percentage breakdowns. The full dataset, available in the comprehensive report, contains detailed subsegment revenue splits, regional demand curves, and customer-tier analyses necessary for execution-level decisions.

Recent industry signals you can’t ignore

The market is already reacting to a few observable shocks that will matter in 2026:

- Benchmark ferrosilicon prices in several production hubs softened through 2025, creating margin pressure for sellers and opportunistic procurement windows for buyers.

- The European Commission introduced country-specific tariff-rate quotas on ferro-silicon imports late in 2025, altering import economics in a way that will affect commercial routing decisions and landed-cost calculus.

- The United States concluded an anti-dumping determination relating to certain incoming supplies, and average U.S. import prices showed a notable year-on-year decline—both developments that shift competitive advantage and could prompt short-term inventory rebalancing.

Next steps for executives preparing 2026 plans

Organizations should treat the coming planning cycle as an optimization opportunity rather than a pure growth bet. We recommend a three-track approach for 2026:

- Protect margins: Implement procurement hedges and update commercial contracts to reduce exposure to short-term price and duty swings.

- Create optionality: Build logistics and sourcing optionality to reroute volumes when regulatory measures or localized price dislocations arise.

- Invest selectively: Prioritize investments that improve product differentiation, lower unit cost through efficiency gains, or open higher-margin application channels.

For strategic teams, the full PW Consulting report is built as a playbook: it provides the scenario models, contractual templates, competitor dossiers, and implementation KPIs you need to move from planning to action. If you are preparing budgets or revising market-entry plans in 2026, accessing that full intelligence will materially shorten your path from insight to execution.

How to access the full study

This preview demonstrates the depth of our modeling and the practical orientation of our recommendations. For the full market dataset (including detailed regional and application splits, supplier-level revenue, and the scenario model used to generate our 3.3% CAGR baseline), please consult the complete Milled FerroSilicon Market report on the PW Consulting publication page.

For detailed analysis of this topic, please visit the official page:Milled FerroSilicon Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com