Revealed: Unveiling Lucrative Investment Opportunities in the Merchandising Market

Networking |

2026-07-02 08:01:16

As a rapidly maturing segment of the photovoltaics ecosystem, dye-sensitized solar cells (DSSCs) are transitioning from niche demonstrations to commercially viable modules across a small-but-critical set of use cases. PW Consulting’s new market study — anchored on a 2025 base year and a 2026–2032 forecast horizon — quantifies that transition and translates it into decision-grade intelligence for C-suite and investment teams preparing strategies in 2026.

Dye Sensitized Solar Cell Market

This preview outlines the study’s directional findings and strategic implications while deliberately withholding detailed segment-level allocations to preserve the report’s commercial value. What follows is a synthesis designed to equip executives with the right questions, risk lenses, and strategic levers to act in 2026 — and to show why full access to the PW Consulting dataset is a high-leverage input for capital allocation, partnership choices, and go-to-market sequencing.

Dye Sensitized Solar Cell Market

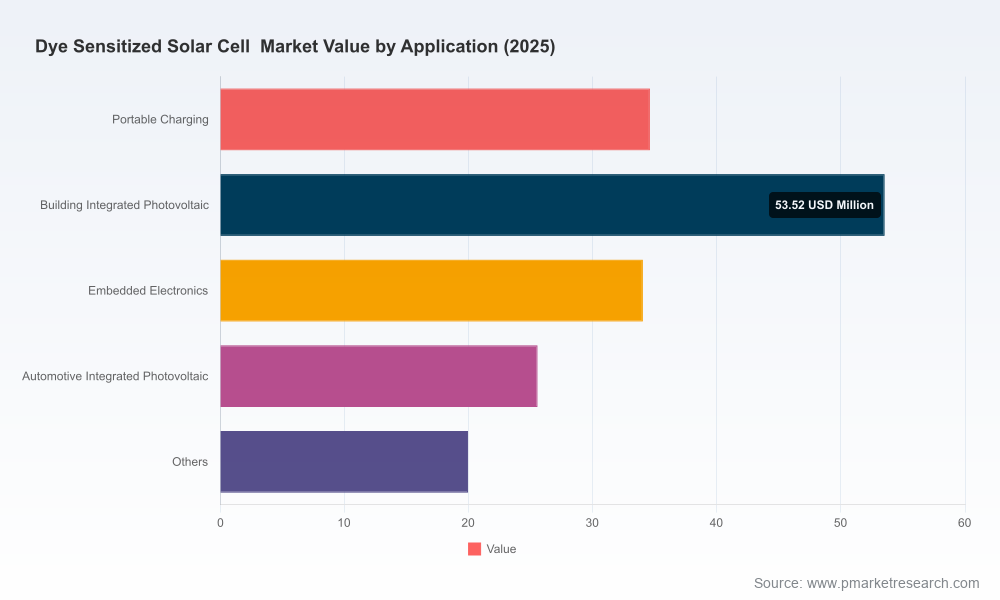

Historical growth and scale: DSSC market value rose materially during 2020–2025 as lab innovations converged with early commercial deployments. PW Consulting models the market expanding from ~USD 99.4 million in 2020 to USD 167.7 million in 2025, reflecting accumulated validation in targeted applications such as ambient-light power for IoT and building-integrated photovoltaics (BIPV).

Dye Sensitized Solar Cell Market

Forecast and growth rate: From a 2026 base outlook, the market is projected to grow at a compound annual growth rate (CAGR) of approximately 12.44% through 2032, reaching an estimated USD 378.8 million by 2032. This pace implies a multi-year window of durable opportunity for suppliers, integrators, and downstream adopters to lock in differentiated positions.

Competition intensity: Market concentration metrics show moderate aggregation at the top — with the three largest firms capturing a meaningful share and the top five firms accounting for just over half of the market — signaling room for new entrants and specialist incumbents to scale through focused innovations and channel strategies.

2026 is a pivotal inflection point for DSSC stakeholders because technology maturity, manufacturing readiness, and policy tailwinds are aligning. Executives should treat 2026 as the year to convert exploratory investments into repeatable commercial experiments. Key decision imperatives include:

Prioritizing use cases with clear unit economics: Small-format, indoor/ambient-light power for sensors and standalone devices continues to yield early revenue and margin upside; concurrently, BIPV and semi-transparent façades are moving into pilot-to-scale phases. The choice of prioritized use cases will determine manufacturing scale, materials sourcing, and sales channels.

Sequencing capital investments: Given the expected double-digit CAGR, staged capital allocation that ties capacity expansion to validated yield improvements and signing of anchor customers reduces execution risk. Technology-agnostic CAPEX models in the report allow CFOs to compare payback periods under multiple throughput and efficiency scenarios.

Orchestrating partnerships: Vertical integration is not always optimal. Strategic partners—material suppliers, construction integrators, and electronics OEMs—can compress time-to-revenue. The report identifies partner archetypes and critical selection criteria to accelerate adoption while mitigating integration risks.

Robust demand modeling: Scenario-based demand stacks for 2026–2032 with sensitivity to efficiency improvements, module pricing, and adoption rates for primary use cases.

Commercial sizing and TAM/SAM/SOM frameworks: Practitioner-ready segmentation (region, type, application) and a reproducible approach to translate technical performance into addressable revenue potential — note: detailed segment shares are available in the full report.

Techno-economic assessments: Module-level levelized-cost-of-energy (LCOE) comparisons, manufacturing cost curves, and margin waterfall models built on material, process, and yield inputs.

Supply-chain diagnostics: Critical supplier mapping for dyes, electrolytes, and substrates; risk heat maps for single-source dependencies and commodity price volatility.

Investment and M&A playbooks: Deal-screening criteria, valuation comparables, and integration checklists calibrated to the DSSC landscape and to firms seeking to bootstrap capabilities via acquisition.

Regulatory & policy tracker: Rolling assessment of subsidies, standards, and procurement programs that materially affect adoption economics for BIPV and building retrofits.

Competitive intelligence toolkit: Company profiles, capability matrices, and capability-roadmap overlays that reveal competitive white space and plausible defensible positions.

The industry exhibits a mix of specialized module manufacturers, dye and electrolyte chemists, and integrators focused on application-specific solutions. Three archetypal players illustrate patterns you should monitor:

Ricoh Company, Ltd. — moving from imaging and electronics into ambient-light DSSC modules optimized for IoT: Ricoh’s strength lies in tailoring solid-state DSSCs for indoor harvesting in sensor ecosystems, offering modules tuned to low-light outputs and compact form factors. Their route-to-market emphasizes OEM supply to electronics assemblers rather than large-scale rooftop installations.

Solaronix SA — chemistry and module engineering at scale: Solaronix blends ionic-liquid electrolyte expertise with practical large-format module development. Their recent strategic moves indicate a push to shorten time-to-efficiency gains through upstream control of dye and electrolyte chemistries, accelerating technology transfer into larger panels.

G24 Power Ltd. — commercial module production for flexible and semi-transparent use cases: G24’s experience in commercial GCell-brand modules demonstrates a viable path to market for flexible, lightweight, and semi-transparent products that serve BIPV and embedded-electronics segments.

Recent market developments underline practical innovation and consolidation pressures:

Advanced encapsulation techniques (e.g., laser-assisted hermetic sealing) are emerging to improve durability and lifetime — a material enabler for deployment in challenging climates.

M&A and partnerships focused on dye chemistry and BIPV integration reflect two parallel plays: securing core materials innovation and accelerating route-to-market through construction and façade partners.

Policy initiatives, including European smart-glass and building-integration programs, are reducing commercialization friction for BIPV solutions while increasing demand visibility for suppliers who can meet building code and lifecycle requirements.

Material inputs — specifically dyes, electrolytes, and semiconductor oxides — remain the primary cost drivers. Two structural trends are worth flagging for procurement and R&D teams:

Shift toward organic and metal-free dyes is reducing dependency on scarce or expensive rare-metal complexes; this has a direct bearing on per-watt material costs and long-term sourcing flexibility.

Electrolyte innovation and encapsulation improvements materially affect module lifetime and therefore the total cost of ownership for building-integrated installations; firms that internalize or secure preferential access to advanced encapsulation technologies can extract durable margin advantages.

Executives should incorporate three interlocking frameworks into 2026 planning cycles:

Stage-gated investment: Tie capacity expansion and process automation investments to technical milestones (e.g., module efficiency, encapsulation lifetime, and yield thresholds) to de-risk scale-up.

Use-case-first commercialization: Force prioritization by IRR and strategic fit — favor channels that accelerate payback and create reference projects (e.g., IoT OEMs, façade partnerships, and specialty consumer electronics).

Supply de-risking playbook: Combine near-term spot sourcing with secured forward contracts for critical dyes and electrolytes, plus contingency plans for substitution with validated alternatives.

This preview is intended to equip you with a rigorous, strategy-focused orientation ahead of 2026 decisions. It surfacing the core market dynamics, company strategies, and cost levers that will determine winners and laggards over the next investment cycle. For teams preparing capital budgets, partnership roadmaps, or product roadmaps, the full PW Consulting report provides the granular segmentation, regional and application-level forecasts, supplier scorecards, and downloadable financial models required to operationalize the high-level recommendations presented here.

To convert directional insight into executable plans, request full access to the report to obtain: the detailed regional and application breakdowns, scenario-specific revenue tables, supplier lead-time analytics, and the set of ready-to-use models that enable board-ready investment cases.

DSSC is no longer only a laboratory curiosity; it is an emergent commercial technology with a clear scaling pathway and differentiated routes to revenue. With a projected market trajectory showing sustained double-digit growth through 2032, 2026 is the inflection year to move from pilots to repeatable commercialization. Use this brief to sharpen hypotheses and structure your next moves — and consult PW Consulting’s full dataset to convert strategy into contracts, capacity, and customers.

For detailed analysis of this topic, please visit the official page:Dye Sensitized Solar Cell Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com