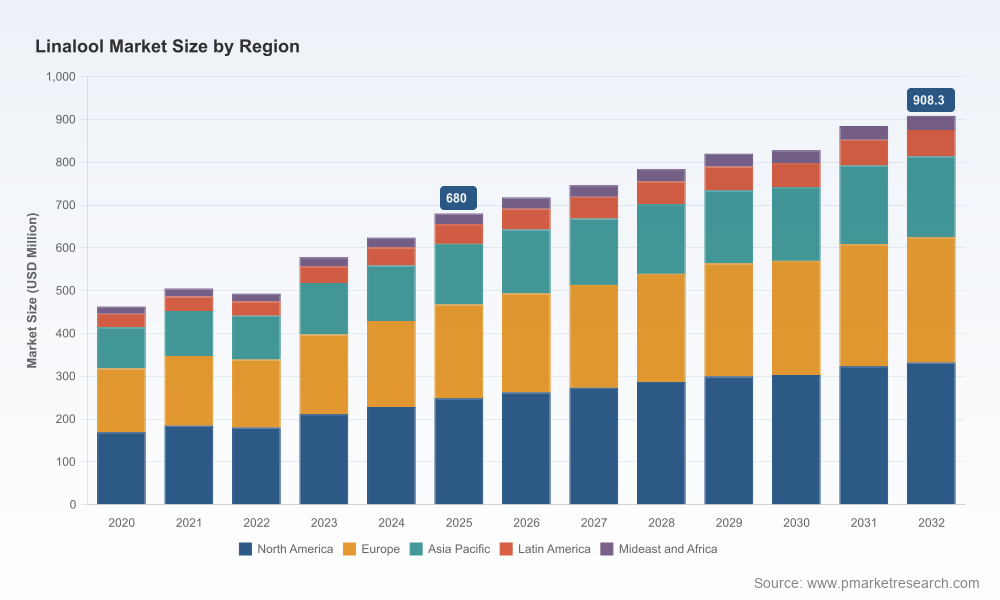

Linalool Market — Strategic Outlook for 2026 Decision-Makers

PW Consulting’s latest Linalool Market study reframes how executives should think about a mature yet dynamically shifting aroma-chemicals sub-sector as they set budgets, supply strategies, and product roadmaps in 2026. Anchored to a 2025 base year and spanning a detailed historical review (2020–2025) and a forward-looking forecast window (2026–2032), the study combines bottom‑up market sizing, supplier intelligence, regulatory mapping, and scenario-driven playbooks to translate market signals into executable decisions. Our modelling shows the global linalool market growing at a compound annual growth rate (CAGR) of 4.3% across the forecast horizon; after registering meaningful recovery and expansion through 2024–2025, the market continues to expand into the early 2030s with clear implications for sourcing, pricing and product differentiation.

Linalool Market

Why this research matters for 2026 decisions

For C-suite teams—procurement, R&D, corporate strategy and M&A—the linalool market represents a classic strategic tradeoff: a relatively concentrated supply base and a diverse demand profile (from fragrances and personal care to detergents and select food applications) that rewards firms who can manage cost, compliance and claim differentiation at the same time. Our report converts market-level growth signals into business-level choices. In plain terms: the market is expanding from a midsized base (with a pronounced uptick after 2022) toward a larger annualized value by the end of the forecast window, and these dynamics will impact raw-material negotiations, formulation strategies and go-to-market positioning.

Linalool Market

What we cover — practical intelligence, not theory

- Robust market sizing and mid-term forecasts (2026–2032) with transparent methodology rooted in trade flows, product-level demand drivers, and price modelling.

- Segment-level demand diagnostics across application groups and product types, with a focus on margin-sensitive customers and high-growth niches.

- Supplier scorecards, production capacities, and a risk-weighted view of the supply chain (including forward scenarios for new capacity coming online).

- Regulatory and standards matrix (IFRA, REACH and region-specific compliance issues) that maps to procurement actions and reformulation pathways.

- Actionable 90-day and 18-month playbooks for procurement, R&D and corporate development teams—templates that leaders can put to work immediately.

The goal is to give managers the intelligence they can act upon in 2026—prioritised, time-bound, and tied to measurable KPIs—without overwhelming them with unverifiable minutiae. (For those seeking the full granular splits and supplier-by-supplier volume estimates, the complete dataset and interactive dashboards are available on our report page.)

Linalool Market

Key dynamics shaping the next five years

- Supply-side evolution: Recent capacity additions by major chemical houses are already altering regional price spreads and contract leverage. A notable example is BASF’s Aroma Ingredients expansion, which included new world-scale units that began commercial linalool production in April 2026—an event that materially affects nearby feedstock flows and merchant availability.

- Raw material pathways: Feedstock markets underpinning terpene-derived aroma chemicals remain a source of volatility. For context, the adjacent Europe crude sulfate turpentine market—one of the relevant upstream pools—was valued at a multi‑hundred million USD level in 2024 and projects steady growth toward the end of the decade, reflecting structural demand for pine-derived streams used across aroma chemistries.

- Regulatory and standards convergence: Hybrid product formulations that reconcile natural claims with cost and compliance have moved from niche to mainstream. One notable development is the introduction of hybrid natural-synthetic linalool blends that meet IFRA and REACH requirements, enabling lower‑cost inclusion in high‑volume detergent and shampoo lines without compromising label claims.

- Innovation in functionality: Suppliers increasingly compete on application-level efficacy rather than commodity pricing alone. Recent commercial introductions—such as dual‑function blends pairing linalool with menthol for consumer diffusers and topical gels—demonstrate how formulation-led claims can create adjacent value pools (for example, in wellbeing and sleep-aid categories).

- Geographic manufacturing shifts: Export-oriented producers in Asia continue to scale, focusing on quality certifications and compliance to gain access to European and North American buyers. These dynamics tighten the interplay between cost advantage and regulatory acceptance for multinational buyers.

Competitive landscape — who matters and why

The market combines global aroma-chemicals majors with specialized regional producers. Market concentration metrics show a moderate-to-high degree of clustering among the top suppliers—an important fact for negotiating teams. Established multinational fragrance houses and chemical companies hold scale, downstream integration and customer relationships; regional producers bring flexibility, lower cost structures and scale in natural-sourcing.

- BASF SE (Ludwigshafen, Germany): A leading synthetic linalool producer with recent world-scale capacity additions. BASF’s new production trains (commissioned in 2026) increase its leverage over merchant volumes and provide an outsize influence on European spot dynamics and formulations where synthetic grades are preferred for cost and consistency.

- Symrise AG (Holzminden, Germany): A major supplier in Europe with strong positions in renewable grades and fragrance ingredient portfolios. Symrise’s breadth in tailored grades makes it a go‑to partner for CPG customers seeking traceable, renewable claims backed by supply security.

- Givaudan and Firmenich: As integrated fragrance and flavor houses, these companies offer linalool and derivative molecules as part of broader formulation services, prioritizing application performance and regulatory stewardship.

- China-based players (e.g., Zhejiang NHU, Jiangxi East, Tianxiang, Jiaxing Sunlong, Purong): These firms supply both natural and synthetic derivatives, with strengths in export volume, cost competitiveness and rapidly improving quality and compliance credentials. Jiangxi East and other exporters have established significant shares in global natural linalool flows, while innovators like Tianxiang are commercializing compliant hybrid blends that unlock large detergent and personal care segments.

These strategic positions mean different buying approaches: large CPG customers will prioritize integrated suppliers for co‑development, while cost-sensitive formulators may source from export-oriented manufacturers under rigorous quality and audit programs. Firms with the right hedging and contract architecture can translate concentration into preferential supply without overpaying for security.

Strategic plays for 2026—what to do now

- Adopt a dual-path procurement strategy: secure core supply via long-term contracts with tier‑1 integrated suppliers while keeping a vetted roster of flexible regional suppliers for volume swings and price arbitrage.

- Re-examine formulation intensity: invest in R&D to reduce active linalool loadings where sensory trade-offs are acceptable, and validate substitutions or synergists that protect sensory profiles while lowering exposure.

- Lock in sustainability narratives: prioritize suppliers with documented traceability and certified renewable options to capture the “green premium” in personal care and premium fragrance segments.

- Scenario-test price and supply shocks: use our forward scenario models (supply expansion, feedstock shock, regulatory tightening) to stress-test margins and develop contingency sourcing playbooks.

- Consider targeted partnerships or minority investments in specialist producers—especially those offering compliant hybrid blends or novel functional formats that open new application niches.

- Leverage supplier competition: with a moderate market concentration among top players, structured RFPs can be used to secure favorable terms post-capacity additions, but expect winners to demand volume and term commitments.

What the full PW Consulting report delivers

- Interactive dashboards with scenario-adjustable forecasts at product, application and regional layers (transparent methodology, ready for board-level presentation).

- Supplier scorecards and an auditable risk index covering capacity, compliance, track record and ESG metrics.

- Price and margin models with raw-material forward curves and cost-build exercises tied to alternative feedstock assumptions.

- Regulatory compliance playbooks (IFRA, REACH and regional registration guidance) and reformulation checklists to accelerate go-to-market.

- M&A and partnership target shortlists with valuation bench-marks and integration risks.

- A 90-day tactical supplier playbook and an 18‑month strategic roadmap calibrated for procurement, R&D and corporate development teams.

We intentionally present the strategic contours and actionable implications here while withholding the granular segment-level datapacks that corporate teams use to execute contracts and capital allocations. That granular intelligence—down to buyer archetypes, supplier lane maps and per-application demand curves—is included in the full study and its companion datasets.

Conclusion — act with precision, not speed

The linalool market in 2026 sits in the classic window where growth is steady, new capacity and product innovation are altering economics, and regulation is redefining what “natural” means in commercial contexts. With a forecast path that implies continued expansion from a 2025 base and a mid-single-digit CAGR into the early 2030s, the next 12–18 months are decisive: procurement and R&D moves made now will lock in margins and end‑product positioning for years.

PW Consulting’s Linalool Market study is designed to convert these sector-level dynamics into corporate advantage—identifying the supplier levers, regulatory pivots and product innovations that executives must act on in 2026. For the full dataset, supplier-level insights and the operational playbooks you can deploy this quarter, please visit our report page to access the complete intelligence package and interactive model suite.

For detailed analysis of this topic, please visit the official page:Linalool Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com