Blood Glucose Testing Market — Strategic Outlook for 2026 Decision-Makers

Executive synopsis

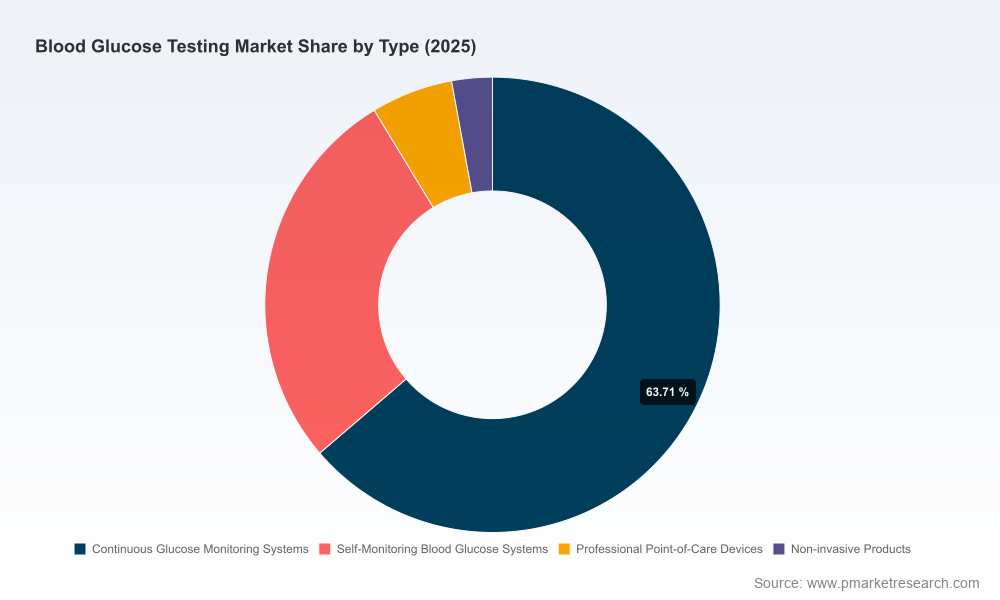

The blood glucose testing market sits at a critical inflection point for corporate strategy in 2026. After steady expansion through the first half of the decade, the sector reached an estimated market size of USD 177.0 Million in the base year (2025) and is projected to grow at a compound annual growth rate (CAGR) of 6.98% over the forecast window, reaching a materially larger market by 2032. This trajectory reflects a confluence of technology adoption (notably continuous glucose monitoring), shifting reimbursement frameworks, and renewed commercial activity from both incumbent device manufacturers and new market entrants.

Blood Glucose Testing Market

PW Consulting’s latest research synthesizes these forces into an operationally actionable perspective for executives, investors, and product leaders who must make high-stakes 2026 decisions — from capital allocation and M&A to regulatory strategy and supply-chain resilience. This preview highlights the strategic value of the report without disclosing the granular segment tables and competitive shares that sit behind our recommendations.

Blood Glucose Testing Market

Why this study matters for 2026 planning

- Decision timing: The market’s mid-decade momentum and the near-term regulatory shifts create windows for first-mover advantage (product launches, CPT code capture, geographic approvals).

- Risk calibration: New reimbursement policies and heightened payer scrutiny mean product success will depend as much on coding, claims strategy and commercial controls as on sensor accuracy or cost of goods.

- Portfolio prioritization: Device roadmaps that deprioritize connectivity, ketone sensing, or bundled remote monitoring services risk losing differentiated value to competitors who package clinical outcomes with reimbursement-ready workflows.

- Capital deployment: Investors and corporate development teams need a clear view of which subsegments and commercialization models deliver defensible margins at scale — the full report provides scenario-level IRR and payback timelines.

Market dynamics: drivers, headwinds and regulatory inflection points

Three structural drivers underlie the market’s projected mid-to-high single-digit CAGR:

Blood Glucose Testing Market

- Technological evolution: The shift from episodic self-monitoring to continuous glucose monitoring (CGM) platforms is changing consumption patterns, product lifecycles and service opportunities (data analytics, software-as-a-medical-device, and subscription models).

- Expanded use cases: Beyond conventional diabetes management, testing hardware and software are being repositioned toward chronic care management and broader health-and-wellness monitoring, expanding addressable markets but also complicating regulatory and reimbursement pathways.

- Commercial maturation: As payers increasingly require outcome-based justification for higher-priced monitoring modalities, vendors are building evidence generation plans and stakeholder engagement strategies to protect reimbursement and margin.

At the same time, material headwinds are shaping near-term execution risk:

- Reimbursement scrutiny — CMS has signaled tighter oversight of glucose monitor payments, increasing audit and recoupment exposure for suppliers and providers. New remote patient monitoring codes and updates to national conversion factors alter the economics of bundled RPM offerings and manufacturer support models.

- Coding and valuation shifts — Specific ambulatory CGM reimbursement inputs have been resized in the latest payment schedules, which changes provider incentives and the unit economics of device-supported monitoring programs.

- Supply constraints — Reports of enzymatic raw material bottlenecks in key markets have introduced input-cost volatility and potential fulfillment delays for test-strip-dependent platforms.

Competitive landscape — what the incumbents are doing

The market’s concentration indicates a competitive environment where a small group of global players hold meaningful share, yet there remains room for targeted innovation and geographic expansion. PW Consulting closely monitors the strategic moves from leading firms; the full report contains granular battlecards, share-by-channel modelling and scenarios for competitive response.

- Abbott Laboratories — Building on its FreeStyle Libre franchise, Abbott is advancing sensor capability with integrated glucose-ketone sensing. Recent regulatory progress for dual-sensing systems positions Abbott at the intersection of clinical innovation and expanded care pathways. Strategic implications: expect Abbott to press on platform differentiation and payer evidence to justify premium positioning.

- Roche Diagnostics — Roche continues investment in its Accu-Chek line with product submissions and approvals to reinforce presence in core markets. Its playbook emphasizes clinical accuracy and provider workflows. Strategic implications: Roche is likely to pursue tighter integration with provider systems and channel partnerships to defend its installed base.

- Ascensia Diabetes Care — Focused on metering accuracy and affordability, Ascensia’s meter-and-strip strategy appeals to established self-monitoring users. Strategic implications: Ascensia competes on price-performance and channel penetration, particularly where payers favor lower-cost monitoring models.

- Ypsomed — With recent regulatory clearances, Ypsomed is pushing further into markets that value interoperability and device ecosystem play. Strategic implications: Ypsomed’s approvals open short-term revenue pathways but will require scale-up of distribution and recall readiness.

- Trividia Health — Trividia’s product family serves value-sensitive segments; recent labeling remediation activity underscores the operational and reputational risks of quality and compliance lapses. Strategic implications: brand resilience and quality governance are essential for sustained access to aggregated channels.

Across these players, common strategic themes emerge: platform convergence (hardware + software + services), payer-first evidence generation, and supply-chain diversification. The competitive tilt in 2026 will favor organizations that can align clinical value with reimbursement pathways while managing operational complexity.

What PW Consulting’s full report delivers (operational highlights)

The full study translates market dynamics into executable intelligence. Key deliverables include:

- TAM and multi-scenario forecasts rooted in clinical adoption curves and reimbursement regimes (2026–2032 projection sets and sensitivity analyses).

- Revenue modeling by product archetype and commercial channel with configurable assumptions for pricing, reimbursement and adoption velocity (note: detailed segment tables are accessible only in the full report).

- Competitive battlecards for the leading global players, including product roadmaps, regulatory timelines, pricing strategies and distribution strategies.

- Reimbursement playbooks that map CPT and payer-code opportunities to go-to-market tactics, including RPM bundling and provider contracting templates.

- Supply-chain risk assessments with supplier concentration mapping and mitigation levers for enzymatic input shortages.

- Investor-ready appendices: deal comparables, accretion/dilution scenarios for M&A, and private-equity investment due diligence checklists.

- Actionable go-to-market scenarios for incumbents and new entrants across three archetypal strategies: platform expansion, value-cost leadership, and localized partnership roll-outs.

We intentionally withhold the detailed segment-level revenue splits in this preview to preserve the report’s commercial integrity; however, the full workbench includes downloadable datasets and model logic to run custom scenarios.

Strategic imperatives for 2026

- Integrate outcomes into product value propositions. Device claims without payer-linked health-economic narratives will face compression in reimbursement and margin.

- Secure supplier diversification for biochemical inputs and build inventory buffers where feasible; contract clauses for priority allocation should be part of procurement playbooks.

- Design commercial models that align with new CMS and private-payer requirements: think bundled revenue streams, RPM code capture, and shared-savings pilots rather than single-device sales.

- Prioritize regulatory filings that create clinical differentiation (e.g., dual analyte sensing, longer wear profiles) while maintaining rigorous label management and post-market surveillance to avoid compliance-driven market disruptions.

- Deploy targeted M&A and partnership scouting to acquire capabilities in digital coaching, data analytics, or regional distribution where organic build-out would be too slow or capital-intensive.

How to use this intelligence in 90 days

- Immediate: Run a friction-point audit of coding and reimbursement exposure for your highest-volume SKUs and adjust contracting/legal terms to mitigate recoupment risk.

- Near-term (30–60 days): Initiate supplier contingency dialogues and scenario-planning workshops to quantify cost and time-to-fulfill impacts of enzyme shortages.

- Quarterly: Re-baseline product roadmaps to incorporate payer evidence-generation milestones and pursue CE/FDA filings that align with market window opportunities.

Conclusion and next steps

For leaders making decisions in 2026, the blood glucose testing market offers both durable growth and actionable inflection points — provided strategy is anchored in reimbursement realities, supply-chain resilience, and platform-driven differentiation. PW Consulting’s full report equips executives with the quantitative models, competitive diagnostics, and tactical playbooks necessary to convert market opportunity into sustainable advantage.

To access the full dataset, scenario models and company battlecards that underpin this preview — including downloadable model files and tailored advisory options — please visit the PW Consulting report page or contact our advisory desk to schedule a briefing tailored to your organization’s strategic priorities.

For detailed analysis of this topic, please visit the official page:Blood Glucose Testing Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com