North America Automotive Rain Sensor Market Trends and Future Opportunities

Art |

2026-06-17 17:50:12

As companies plan product roadmaps, partnerships, and capital allocations for 2026, the Automotive Head‑up Display (HUD) market presents a high‑growth, strategically consequential frontier. PW Consulting’s latest research (base year 2025, historical 2020–2025, forecast 2026–2032) synthesizes hard market sizing, technology trajectories, regulatory drivers, and competitive reality into an operationally focused guide for executives. This preview surfaces the research’s most actionable perspectives while intentionally withholding the granular segment-level tables and split analytics that are reserved for subscribers and clients.

Automotive Head-up Display (HUD) Market

The HUD market has moved from an emerging premium option to a mainstream instrument for vehicle human‑machine interface and ADAS augmentation. Our model, which uses 2025 as the base year, quantifies this shift: the global market reached a robust level in 2025 and is forecasted to continue expanding through 2032 at a compounded annual growth rate (CAGR) of 13.5% (USD, revenue unit: Million). This is not a linear uptick—the profile shows step changes tied to regulatory inflections, new OEM platform launches, and the commercial roll‑out of AR‑capable systems.

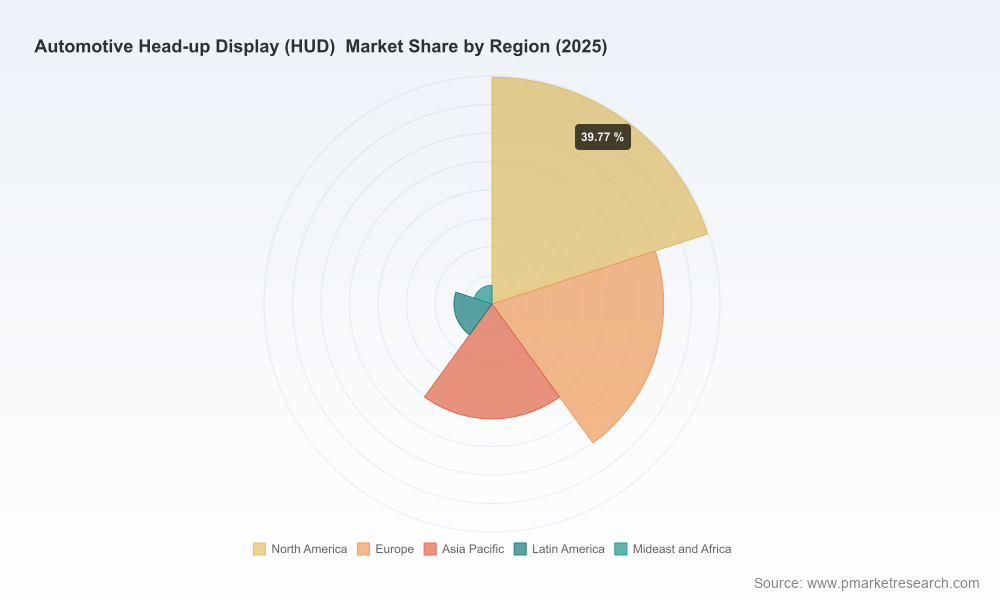

Automotive Head-up Display (HUD) Market

Two strategic takeaways flow directly from the numbers. First, absolute market growth and the high CAGR make HUD a compelling target for R&D and supply‑chain investment: returns on features that materially improve driver safety and reduce cognitive load will compound as install bases broaden. Second, growth is uneven across adoption triggers (regulation, ADAS bundling, premium vehicle feature diffusion), which validates a portfolio approach to product and GTM (go‑to‑market) strategy rather than a single‑track bet.

Automotive Head-up Display (HUD) Market

Regulation crystallizes industry incentives: With recent policy moves—such as strengthened EU safety standards and evolving NHTSA guidance—automakers will increasingly mandate safety‑critical in‑vehicle displays. These regulatory vectors accelerate adoption cycles in the near term and create procurement windows for suppliers in 2026.

Technical inflection toward AR and driver‑centric features: AR‑capable HUDs and local dimming/light management are moving from demonstration to production readiness. Suppliers who resolve optical, software, and driver‑monitoring integration by 2026 will secure the most valuable OEM design slots.

Supply‑chain and cost inflection: Component standardization, maturation of projection and eye‑tracking subassemblies, and potential commoditization of some modules mean companies must decide in 2026 whether to vertically integrate, outsource to specialist optics firms, or form strategic alliances.

Recent regulatory developments are not peripheral: they are catalytic. Newer vehicle safety protocols emphasize how HUDs can reduce driver distraction and deliver safety‑critical cues. Industry standards bodies and safety assessment programs are now explicitly acknowledging head displays as acceptable channels for ADAS alerts and speed/warning information. For decision‑makers this creates a dual mandate: product teams must demonstrate safety and usability compliance, while commercial teams must align offerings with certification timelines. Missing a regulatory compliance milestone in 2026 can mean exclusion from important OEM platform opportunities through the 2027–2028 product cycles.

The market sits at a mid‑consolidation stage: a handful of established tier‑ones and several highly specialized tech challengers are jockeying for design wins. Market concentration metrics indicate a competitive but not monopolized environment—leading players capture significant share, but there is still room for disruptive entrants and OEM captive units to carve niches.

Panasonic Automotive Systems (Osaka): Strength lies in optical engineering and integration of high‑intensity, distortion‑controlled projection systems. Recent achievements around cybersecurity and functional safety (notably certifications in 2025) position them well for OEMs that prioritize compliance and system assurance.

SOLUM (Seoul): A classic example of a focused AR specialist. Their modular, vehicle‑integrated AR HUD designs—incorporating eye‑tracking and flexible FOV—are attractive for OEMs looking to differentiate user experience without entirely re‑architecting the cockpit.

Visteon (Michigan): Plays to strength in cockpit electronics integration and strategic co‑development partnerships. Their public collaboration to co‑develop advanced HUD systems signals a play for scale across global OEM platforms and accelerated software/hardware co‑development.

Nippon Seiki, Continental, DENSO, Yazaki: These incumbents combine deep OEM relationships, manufacturing scale, and system‑level integration capabilities. The incumbents’ competitive advantage is less about a single technological surprise and more about predictable delivery, cost control, and multi‑system integration (wiring, ADAS, cockpit E/E).

What this competitive matrix means for potential entrants and investors: look for white spaces at the intersection of optics, software (perception/UI), and validated safety workflows. Strategic partnerships—rather than unilateral vertical integration—are likely the fastest route to design wins on global platforms.

Prioritize modular AR roadmaps: Invest selectively in AR capabilities that solve clear safety or UX problems (e.g., lane‑level navigation cues, collision overlays) rather than pursuing maximal FOV at all costs.

Lock down harmonized interfaces: Standardize software APIs and calibration procedures to reduce OEM integration friction. Faster validation cycles will convert into earlier production ramp slots.

Certify early for safety standards: Align development timelines with safety certification roadmaps and pursue pre‑certification audits. Certification is a purchasing filter for many OEMs; early certification is a differentiator.

Design for manufacturability and cost decline: Focus on optical component sourcing strategies and supplier agreements that can sustainably reduce BOM cost by the second half of the decade.

Use partnerships to de‑risk tech delivery: Co‑development agreements with optics firms, AR software houses, and driver‑monitoring specialists accelerate system readiness while preserving capital.

Prepare flexible commercial models: Offer bundled solutions, subscription updates for software/over‑the‑air features, and differentiated feature tiers to capture both premium and volume segments.

The full advisory package goes well beyond this strategic preview. Clients receive:

Detailed market sizing and validated forecasts (2026–2032) with scenario analysis under conservative, base, and accelerated adoption paths;

Granular segmentation (by region, HUD type, and technology) with TAM/SAM/SOM frameworks, elasticity analysis, and inflection‑point timing—(note: these granular tables are intentionally omitted from this public preview);

Competitive benchmarking and supplier heatmaps that evaluate technical capability, manufacturing readiness, pricing posture, and OEM relationship strength;

Commercial and product playbooks: go‑to‑market sequencing, pricing models, partner archetypes, and a 24‑month tactical roadmap for securing platform‑level design wins;

Procurement and supply‑chain checklists with risk assessment, suggested dual‑sourcing strategies, and component cost curves to support negotiation scenarios;

Regulatory compliance matrix tying product features to applicable testing and certification milestones across major markets.

For C‑suite and board agendas, HUDs should now appear in three actionable buckets: (1) product differentiation for premium vehicles, (2) safety compliance and ADAS bundling for mid‑market platforms, and (3) cost‑efficient, scalable HUD options for volume models. Capital allocation, M&A, and partnership decisions should be stress‑tested against the market growth profile and the timing of regulatory milestones highlighted earlier. Tactical procurement and R&D spend should prioritize software ecosystems and safety certification streams that unlock the largest OEM opportunities within the 2026–2028 window.

The HUD market is a textbook example of a technology that moves from luxury to safety‑critical utility within a single regulatory cycle. Our forecast and strategic framework quantify that transition and translate it into executable moves for 2026. This preview is designed to establish confidence in PW Consulting’s methodology and to surface the high‑value implications; the full report contains the granular, transaction‑grade detail that boards and procurement teams will use to finalize budgets and design win pursuits.

To access the complete segment breakdowns, vendor scorecards, and the 24‑month tactical playbook, clients and partners may request the full Automotive Head‑up Display (HUD) Market report and advisory engagement from PW Consulting.

For detailed analysis of this topic, please visit the official page:Automotive Head-up Display (HUD) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com