Is the Carsicko Hoodie on Crepslocker Actually Authentic

Shopping |

2026-06-27 11:41:58

PW Consulting’s Toilet Partitions Market briefing synthesizes the market intelligence that executive teams, product leaders, and investors will need to act decisively in 2026. Built on a detailed historical base (2020–2025) and a forward-looking modeling window (2026–2032), the study blends end-market sizing, supplier benchmarking, regulatory impact analysis, and transaction-grade commercial playbooks. The market continues to expand steadily: from a multi-year baseline anchored in 2025 (base year) the global market grows at a steady compound annual growth rate of 4.5% through our forecast horizon, with projected scale rising materially by 2032. This introduction explains why this research is strategically valuable, what we deliver, and how to use our insights to shape near-term decisions while preserving the full granularity for subscribers to the full report.

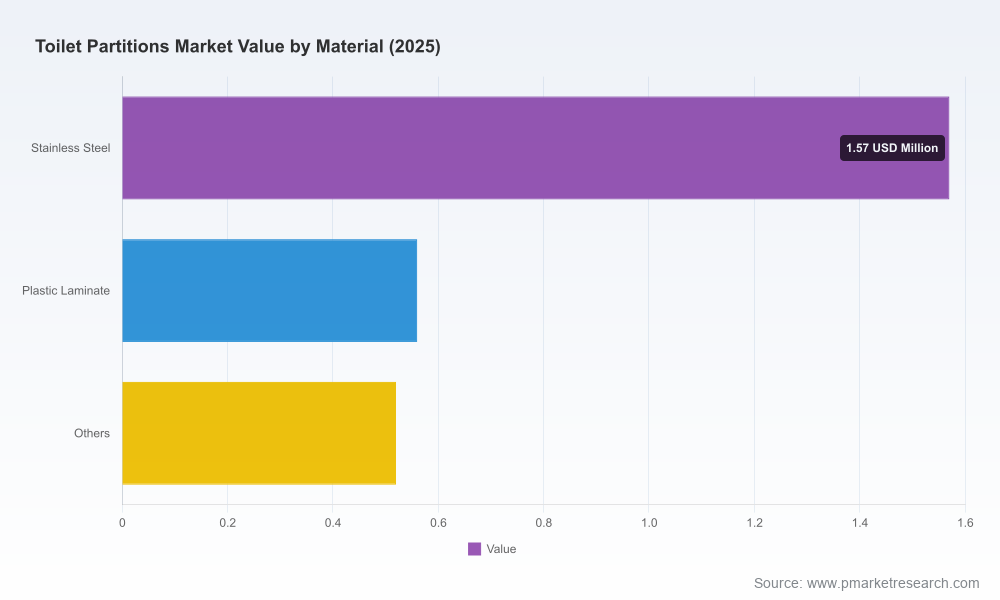

Toilet Partitions Market

Actionable visibility in a stable-growth market — The sector is not hypercyclical, but directionally positive. Modest compound growth reflects continuing investment in institutional and commercial facilities, renewed public construction programs, and retrofit cycles driven by accessibility and hygiene requirements. For companies planning capacity investments, product launches, or M&A in 2026, the measured growth profile supports disciplined, targeted expansion rather than aggressive scale-up.

Toilet Partitions Market

Regulation and public spend are near-term tailwinds — Accessibility regulations and public construction budgets are tangible demand drivers for institutional partitions. Recent public construction activity at elevated levels supports project pipelines for K–12, higher education, healthcare, and municipal facilities — all core buyers of partition systems.

Toilet Partitions Market

Input-cost and labor dynamics require tactical agility — Raw material availability, recycled-content mandates, and manufacturing labor costs are increasing pressure on list prices and lead times. Suppliers that can manage supply chains, offer quick-ship programs, or provide value-engineered solutions will protect margins and win specification votes.

Consolidation and concentration shape competitive options — The market exhibits meaningful concentration among a handful of industrial players. That structure creates differentiated opportunities: for incumbents to defend margins via product breadth and service, and for specialized entrants to capture niches through speed, sustainability credentials, or installation-focused offerings.

Comprehensive market model (2020–2032) in downloadable spreadsheet form — scenario-ready, with base, upside, and downside demand paths, sensitivity toggles for raw-material prices, labor-cost escalation, and public-construction spending assumptions.

Segment coverage that supports commercial prioritization — regional demand curves, material and product-type demand matrices, and downstream channel analysis designed for go-to-market planning (note: detailed segmental tables and percentage splits are available in the subscriber-only model).

Procurement & specification playbook — contracting templates, value-engineering checklists, and specification language optimized for durability, sustainability certifications, and accessibility compliance.

Pricing and margin toolkit — historical list-price tracking, cost pass-through levers, and benchmark ranges to inform negotiations and price-list resets.

Supplier heatmaps and risk dashboards — supplier concentration metrics, geographic exposure, lead-time fragility assessments, and recommended mitigation levers for manufacturers and large buyers.

Competitive scorecards and transaction support — vendor profiles, M&A screening criteria, and a short-list of strategic targets for bolt-on plays aligned to product, channel, or geographic gaps.

Case studies — implementation examples covering quick-ship programs, institutional retrofit campaigns, and sustainability-driven specification wins that illustrate execution trade-offs.

The market is shaped by a set of established manufacturers with complementary capabilities. Our competitive review emphasizes product-platform strengths, go-to-market posture, and recent corporate moves that change the competitive map.

Bobrick Washroom Equipment, Inc. — A legacy U.S. supplier focused on comprehensive restroom accessory portfolios and custom partition systems. Bobrick’s strength lies in specification relationships and ADA compliance expertise. Its April 2026 catalog update signals continued investment in engineered selections and new cubicle ranges, reinforcing its position with architects and facility managers.

Hadrian Inc. — Noted for powder-coated, phenolic and recycled-content offerings, Hadrian competes on LEED-aligned solutions and institutional durability. Their product set is positioned for buyers with sustainability mandates and large-scale procurement cycles.

Bradley Corporation — Differentiates through a diverse product mix including floor-to-ceiling and aesthetic options such as glass and Euro-style partitions, and material variants with antimicrobial or sustainable finishes—an advantage in healthcare and premium commercial projects.

General Partitions Manufacturing Corp. — A recognized provider of HDPE partitions and quick-ship privacy solutions. Its April 2026 catalog reiterates focus on fast-turn channels and modular offerings attractive to contractors and specifiers managing tight schedules.

Inpro Corporation — Emphasizes institutional-grade durability, with metal, laminate and phenolic product lines that suit heavy-use applications in healthcare and education.

ASI Global Partitions — Canadian-based supplier with design options in HDPE and phenolic, including integrated privacy and high-height systems; appeals to projects where installation footprint and aesthetics are priorities.

Scranton Products — A market leader in HDPE and customization with extensive finish and configuration options. The December 2025 asset acquisition broadened its product breadth and is material for competitors and investors evaluating consolidation or bolt-on strategies.

Collectively, the top-tier firms control a substantial portion of market revenue, creating meaningful barriers for small-volume entrants but also opening pockets for focused specialists—especially those that can execute rapid delivery, certified sustainable materials, or installation services.

Manufacturers — Prioritize quick-ship assortments and value-engineered product lines to offset labor and material cost volatility. Preserve specification relationships through enhanced digital spec tools, updated catalog content, and performance-backed warranty offerings. Consider selective investments in recycled-content processes and certification pathways to maintain preferential access to public and institutional tenders.

Distributors and contractors — Lock in supplier agreements that balance price stability with lead-time guarantees. Build differentiated installation services (bundled design + install) to raise switching costs and improve margin capture, particularly for retrofit projects where logistics are complex.

Specifiers and facility owners — Re-evaluate total cost of ownership rather than unit price: material longevity, maintenance cadence, and hygiene features materially affect lifecycle cost. Leverage our procurement playbook to drive better outcomes in public bids and large-scale rollouts.

Investors and M&A teams — Focus on targets that expand quick-ship capabilities, proprietary finishes, or channel access. Our model identifies where moderate growth and concentrated supply create arbitrage for scale-driven margin improvement or bolt-on consolidation.

The analysis is rooted in an audited historical time series (2020–2025), a base year of 2025, and a transparent forecast period covering 2026–2032. We combine bottom-up shipment and revenue models with macro overlays for public construction activity, regulation-driven retrofit cycles, and raw-material cost paths. Scenario branches incorporate upside and downside public-capex assumptions and stress-test outcomes against labor and input-price shocks. Our confidence is highest in near-term demand drivers (next 18 months) where project pipelines and procurement cycles are visible; longer-term outcomes are more sensitive to infrastructure-policy shifts and material innovation cycles.

This introduction gives the strategic frame and executive takeaways. The full PW Consulting Toilet Partitions Market report contains the granular segmentation, company-level market shares, price and cost curves, and downloadable models you need to operationalize the recommendations herein. For commercial teams, the Excel model becomes a near-term action tool: rerun scenarios with your procurement assumptions, model the impact of a supplier price increase, and evaluate the ROI from a quick-ship capability investment. For corporate development teams, our scorecards and target short-lists accelerate screening and valuation calibrations.

To access detailed segment splits, region- and material-level forecasts, company market shares and the full suite of commercial tools and templates, please consult the complete PW Consulting report and dataset.

For detailed analysis of this topic, please visit the official page:Toilet Partitions Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com