Best Indian Restaurant In Cincinnati Ohio – A Flavorful Experience at Shaan Indian Cuisine

Food |

2026-06-23 22:13:39

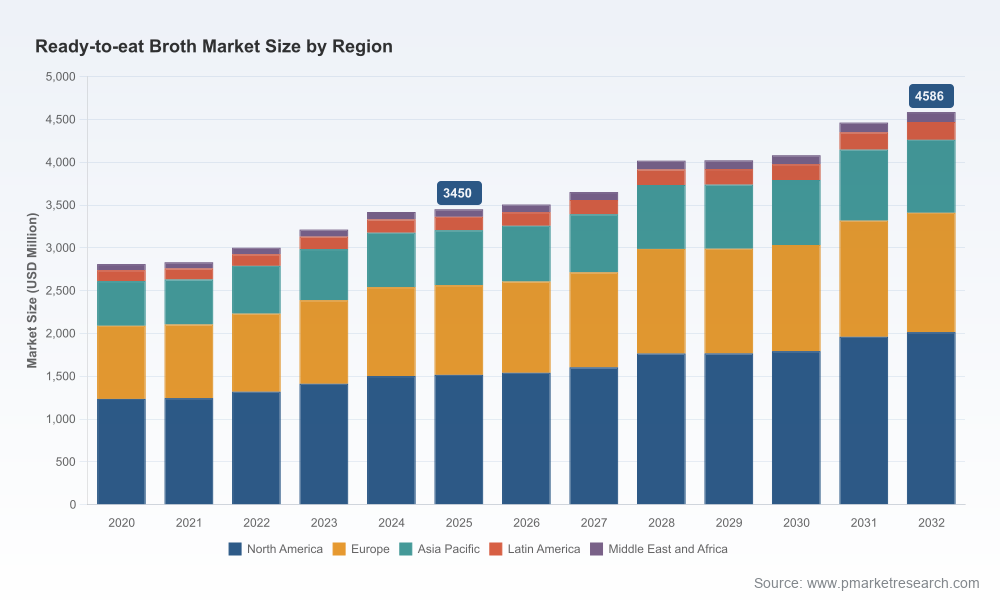

PW Consulting’s latest Ready To Eat Broth Market report synthesizes five years of historical performance and a seven‑year forecast window to deliver a decision‑grade intelligence package tailored for executives, investors, and category managers planning for 2026. The market has demonstrated steady expansion from the early 2020s and, under our baseline model, is projected to grow at a compound annual growth rate (CAGR) of approximately 4.15% through the forecast horizon. This release is designed as a directional trailer: it surfaces high‑conviction implications, frameworks, and action checklists while reserving proprietary segment tables and granular scenario outputs for the full report.

Ready To Eat Broth Market

Timing: 2026 is a turning point — cost dynamics, nutrition regulation, and evolving consumer routines converge to change margin and assortment calculus. Our market model brings these variables together so leaders can test investment cases against a calibrated baseline growth trajectory.

Ready To Eat Broth Market

Clarity: The category is no longer niche. Anchored by growing consumer demand for convenience and functional sipping broths, the category’s total addressable revenue has expanded meaningfully since 2020, creating both scale opportunities and competitive pressure.

Ready To Eat Broth Market

Decision focus: The report is structured to move organizations from descriptive analytics to prescriptive choices — SKU rationalization, private‑label positioning, pricing architecture, and supply hedging are covered with executable next steps.

Integrated demand and supply model: A calibrated baseline (2026–2032) built on historical volumes, price elasticities, and recent commodity forecasts. The model is easy to re‑parameterize for custom assumptions — useful for M&A due diligence and capex planning.

Scenario playbooks: Three credible futures (base, downside, upside) that isolate the impact of raw material cost swings, packaging mix shifts, and new labeling requirements on revenues and margins.

Competitive diagnostics: Profiled playbooks for the leading national and specialist brands, including go‑to‑market vectors, SKU and innovation strategies, and implied margins — enabling rapid benchmarking against peers.

Retail and channel tactics: Actionable assortment maps for brick‑and‑mortar, club, convenience, and digital channels, plus trade promotion templates calibrated to maximize velocity while protecting margin.

Supply chain and input risk register: A prioritized list of supplier exposure points, recommended contract terms, and a hedging guide reflecting current poultry and beef market signals.

Regulatory readiness checklist: Practical implementation steps for upcoming nutrition labeling changes, including front‑of‑package indicators and updated serving size declarations.

M&A and partnership screen: A scored universe of mid‑market targets and co‑pack opportunities with likely synergy levers and integration risks.

Input cost divergence: Recent commodity intelligence points to divergent pressures across animal proteins. Expanding chicken supplies are tempering broiler price growth in the near term, while wholesale beef prices are expected to move higher. These differential trends change relative gross margins between poultry‑based and beef‑based products and should inform sourcing and pricing strategies.

Regulatory evolution: The FDA’s proposed front‑of‑package nutrition labeling (Low/Med/High indicators for saturated fat, sodium, and added sugars) and ongoing Nutrition Facts adjustments increase the cost and time required for packaging changes. Brands that anticipate these requirements can convert regulatory compliance into a competitive advantage through clearer claims and reformulations.

Consumer positioning: Health‑adjacent narratives (low‑sodium, clean‑label, collagen/bone‑broth benefits) remain powerful but are fragmenting into micro‑niches. Premiumization around provenance and production method sits alongside value demand for multipurpose cooking bases.

Channel evolution: E‑commerce and subscription models are expanding repeat purchase opportunities, while club and mass channels continue to drive scale. Packaging formats that balance pourability and shelf stability will win cross‑channel adoption.

The category is characterized by a mix of large CPG incumbents and specialist challengers. Leading multinational and national food companies maintain broad distribution and multi‑format portfolios, while smaller, purpose‑driven brands often command premium price points and claim health‑oriented credentials. Our competitive review includes strategic profiles for legacy players, mainstream CPG brands, and emerging premium specialists, with attention to:

Portfolio breadth vs. depth: National brands leverage scale to offer multiple formats (from concentrated bases to ready‑to‑eat cartons), while niche players double down on single‑product excellence such as bone broths.

Channel and brand amplification: Incumbents are defending shelf space and expanding e‑commerce, while smaller brands exploit direct‑to‑consumer and specialty retail to bootstrap growth.

Innovation cadence: New flavors, functional fortifications, and clean‑label reformulations are the primary vectors for NPD. Recent launches demonstrate that flavor innovation and no‑salt or low‑sodium variants continue to generate retailer interest.

Market concentration: The top three and five firms account for a meaningful share of category revenue, indicating moderate concentration and opportunity for scale advantages; however, there remains room for disruption through differentiation and channel specialization.

1) Re‑architect SKU and price ladders: Rationalize SKUs that underperform unit economics and redeploy shelf space to formats and flavors with higher velocity or margin potential. Use our elasticity matrices to model trade promotion ROI before committing to large resets.

2) Hedge input exposure: Secure forward contracts where possible for beef inputs while optimizing poultry sourcing protocols to capture near‑term supply slack. Our supply risk matrix ranks suppliers by exposure and contingency cost.

3) Accelerate labeling and reformulation roadmaps: Lock in packaging designs that accommodate potential “Low/Med/High” FOP labels and validate reformulations for sodium reduction without sacrificing taste—an area where work with culinary R&D pays disproportionate returns.

4) Differentiate via format and functionality: Invest selectively in premium functional formats (e.g., collagen/bone broth variants) for higher ASPs, while protecting core cooking‑use SKUs for broad consumption occasions.

5) Target M&A and co‑pack partnerships with clarity: Pursue bolt‑ons that fill capability gaps (e.g., organic certification, co‑packing capacity, cold‑chain expertise) and use our M&A scorecard to quantify synergies and integration risks.

Our baseline projection for the market is informed by a 4.15% CAGR through the forecast window and reflects reasonable assumptions on consumer adoption and price realignment. Within the full report we provide downloadable financial models that translate those top‑line scenarios into P&L, cash‑flow, and sensitivity tables for product line extensions and channel investments. In keeping with the “trailer” approach, we intentionally withhold detailed segmented revenue tables and the full sensitivity matrices in this summary — these are included in the premium deliverable to preserve the tactical value of the data for subscribing clients.

Rapid diagnostic: A condensed engagement to map your portfolio against our category heatmap and identify three immediate margin capture initiatives.

Full strategy sprint: End‑to‑end commercialization planning, from reformulation experiments and packaging pilots to retailer negotiations and launch economics.

M&A advisory: Target shortlist generation, financial diligence templates, and integration playbooks for bolt‑on consolidation within the ready‑to‑eat and broth adjacent categories.

For commercial teams, investors, and category leaders preparing 2026 budgets, this report provides the frameworks and tactical roadmaps needed to convert market expansion into sustained profitability. The public summary above highlights core themes, competitive dynamics, and high‑probability moves; the full report unlocks the granular segment tables, regional splits, SKU‑level forecasts, and downloadable models necessary to execute. To review the complete methodology, segmented forecasts, and the full set of competitor profiles and M&A screens, please access the full report on our website.

PW Consulting’s Ready To Eat Broth Market report positions you to move beyond intuition and into measurable action as you plan for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Ready To Eat Broth Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com