Autoimmune Disease Diagnostics Market Insights 2034: Share, Demand and Innovation Outlook

Health |

2026-05-25 15:20:57

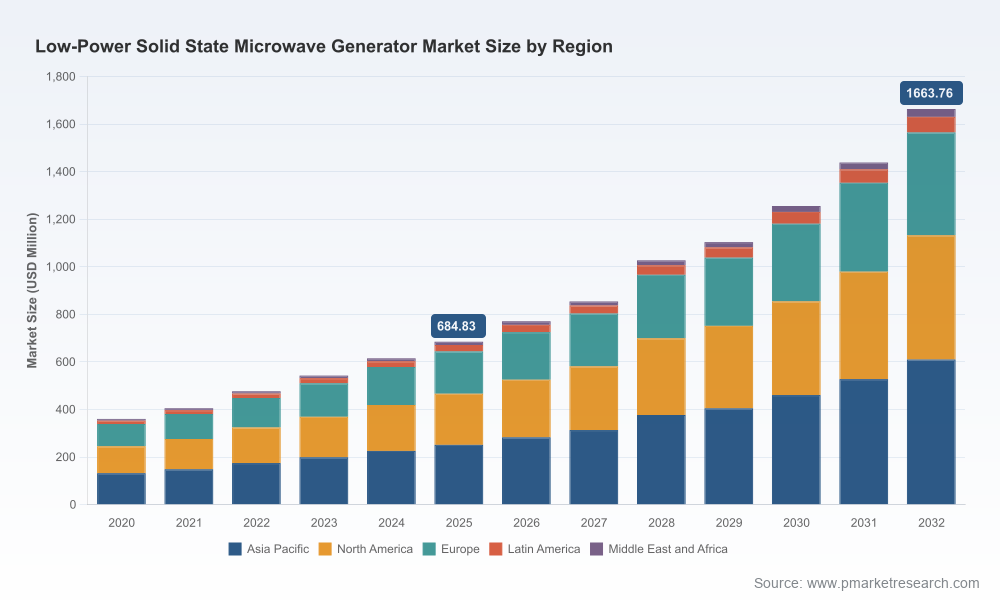

PW Consulting today releases an executive briefing based on our forthcoming comprehensive market study, Worldwide Low-Power Solid State Microwave Generator Market (base year 2025, historical series 2020–2025, forecast 2026–2032). The market reached approximately USD 684.83 Million (revenue unit: Million) in 2025 and is projected to expand rapidly underpinned by a compound annual growth rate (CAGR) of 13.52% through the 2026–2032 forecast horizon, reaching a modeled market size in excess of USD 1.6 Billion by 2032. This briefing distills the strategic implications of that trajectory for corporates, investors, and technology leaders planning decisions in 2026.

Worldwide Low-Power Solid State Microwave Generator Market

Technology-led efficiency gains: The transition from legacy vacuum-tube magnetrons to solid-state architectures (notably GaN-enabled designs) is unlocking tighter frequency control, higher energy efficiency and more predictable heating profiles. These attributes convert into superior process control for applications ranging from plasma generation to precision medical therapies.

Worldwide Low-Power Solid State Microwave Generator Market

Regulatory and standards momentum: Recent regulatory scrutiny—such as requirements for predictable heating patterns in food applications—and advances in standardization are increasing the value of narrow-band, frequency-stable solid-state generators. This creates a structural preference for solid-state over magnetron-based systems in regulated verticals.

Worldwide Low-Power Solid State Microwave Generator Market

Commercial pull from decarbonization and productivity objectives: Industrial and laboratory customers increasingly value energy-saving, frequency-agile solutions that reduce lifecycle carbon intensity and support more repeatable, automated processes.

Consolidation and market concentration: The market demonstrates meaningful concentration among a handful of incumbents (our model places three-firm concentration and five-firm concentration at material levels), which both raises barriers and creates targeted opportunities for M&A, distribution alliances and white-label OEM partnerships.

Product strategy: Prioritize GaN-capable platforms where footprint, efficiency and frequency agility deliver downstream value. At the same time, retain LDMOS options for legacy compatibility in specific industrial segments. Modular, field-serviceable designs will accelerate adoption in production environments where uptime and mean-time-to-repair matter.

Go-to-market focus: Segmentation is shifting from purely power-centric selling to solution-based value propositions that combine generator hardware, control software and process expertise. Companies that package predictive maintenance, frequency shaping and process recipes will secure premium positioning.

Supply chain and sourcing: GaN raw materials and specialized subcomponents are a critical bottleneck risk. Dual sourcing and strategic supplier relationships (and, where viable, equity investment into strategic suppliers) will be essential to maintain product roadmaps and margin stability.

M&A and partnerships: Given the market’s measured concentration, targeted acquisitions of complementary module makers, control software houses, or regional systems integrators can accelerate time-to-market and defensibility. Alternate routes include exclusive distribution agreements or co-development with OEMs serving adjacent industrial segments.

Regulatory readiness: For companies targeting food, medical or aerospace-adjacent applications, investing early in validation programs and in demonstrating compliance with narrow-band stability and repeatable heating profiles reduces commercialization risk and shortens sales cycles.

Transparent market-sizing methodology with reconciled historicals (2020–2025) and company-validated forecasts for 2026–2032, including scenario sensitivity to component lead times and technology substitution rates.

Proprietary vendor scorecards assessing engineering depth, product breadth, service footprint and go-to-market capability for the leading and emerging suppliers in the space.

Use-case value maps that translate technical attributes (frequency stability, power density, cooling architecture) into measurable customer KPIs (throughput, yield, energy consumption, OPEX impact).

Commercial playbooks for OEMs, integrators and system providers: pricing guidelines, bundling strategies, resale channel recommendations and warranty/service models.

Regulatory and compliance checklists tailored to food, medical and laboratory applications—covering FDA-style heating predictability requirements, country-specific certification pathways and environmental reporting obligations.

Investment and M&A framework: candidate screening criteria, valuation sensitivity to tech adoption curves, and integration blueprints designed for both strategic acquirers and private equity sponsors.

Hands-on implementation tools: pilot test protocols, bill-of-materials examples, and a six-to-twelve-month go-to-pilot roadmap for customers validating solid-state transitions.

Note: this briefing intentionally omits segment-level revenue splits and granular regional/application percentages to preserve the unabridged value proposition of the full report. Subscribers receive the complete tables, vendor revenue breakdowns, and model files required for board-level decisioning.

Incumbent specialists: Several established players offer mature, water-cooled rack-mount and modular units with field-proven reliability tailored for R&D and industrial labs. These vendors emphasize ruggedness, precise power control and full-system protections—attributes favored by process engineers and systems integrators.

GaN pioneers and agile innovators: A cohort of newer and mid-sized vendors has moved aggressively to GaN-based architectures, marketing higher efficiency, smaller footprint and better frequency agility. Their propositions are attractive for integrators pursuing compact or mobile systems and for high-mix R&D environments.

OEM module suppliers: Companies offering scalable modules and distributed architectures appeal to OEMs seeking to embed RF capability into broader systems. These players often enable faster productization for medical and ISM-market customers by delivering tested, serviceable modules.

Regional manufacturers and system houses: Localized suppliers—particularly those with strong cost competitiveness and fast lead times—are important partners for regionally regulated markets and high-volume OEM channels. Their presence increases the need for global vendors to refine service and warranty promises.

Recent industry moves are illustrative: new product expansions by GaN-focused entrants, module launches from established OEM suppliers, and academic/industry reviews advancing control techniques for uniform heating. These developments accelerate the technology adoption curve and compress the window for differentiation based purely on hardware specs.

Laboratory and R&D customers: Prioritize frequency agility, fine-grain power control and modularity for iterative development workflows.

Precision medical and scientific instruments: Require high reliability, repeatability, and certification-ready documentation to support clinical use and regulatory filings.

Industrial heating, plasma and small-scale processing: Demand robust cooling, serviceability and predictable energy consumption to integrate into automated production lines.

Systems integrators and OEMs: Seek module-level solutions and software toolchains to minimize integration risk and accelerate time-to-market.

Importantly, “low-power” in this market context typically refers to generators below multi-kilowatt industrial systems; applications tend to be laboratory, R&D, plasma and precision-process oriented rather than large-scale bulk food processing.

Component supply risk (GaN substrates and specialized RF components): mitigate via multi-sourcing, long-term purchase agreements, and strategic inventory buffers.

Regulatory divergence across jurisdictions: invest in modular compliance documentation and early engagement with certification bodies for prioritized verticals.

Price and feature commoditization: move up the value chain with software-enabled differentiation (process recipes, analytics, predictive maintenance) and service contracts.

Integration complexity: standardize interfaces and provide certified integration kits for key OEM partners to reduce time-to-deploy.

Run a fast product-roadmap audit: assess which platforms can be GaN-enabled within 12 months and quantify the margin/OPEX impact.

Initiate two pilot customer engagements—one in a regulated vertical (medical or food lab) and one in an industrial process—to validate use-case value and collect real-world performance data.

Reassess supplier strategy: secure critical RF component supply through dual-source agreements or strategic supplier investments.

Prepare a targeted M&A shortlist using PW Consulting’s vendor scorecards—prioritize module providers, control-software specialists and regional service providers.

Establish a regulatory-compliance fast track: map certification gates for prioritized markets and allocate resources to close documentation and test gaps.

PW Consulting’s full market report contains the complete dataset, including reconciled historicals (2020–2025), detailed forecasts (2026–2032) by region, technology and application, vendor revenue splits, price decks, and downloadable financial models. For executive briefings, corporate workshops, bespoke scenario modeling or access to the full report and its appendices, contact PW Consulting to schedule a briefing. The full deliverable is designed to enable the specific 2026 investment, product and M&A choices that boards and executive teams must finalize this year.

For detailed analysis of this topic, please visit the official page:Worldwide Low-Power Solid State Microwave Generator Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com