Flexible Heater Market Growth Driven by Industrial Automation and Smart Heating Solutions

Technology |

2026-07-06 11:40:16

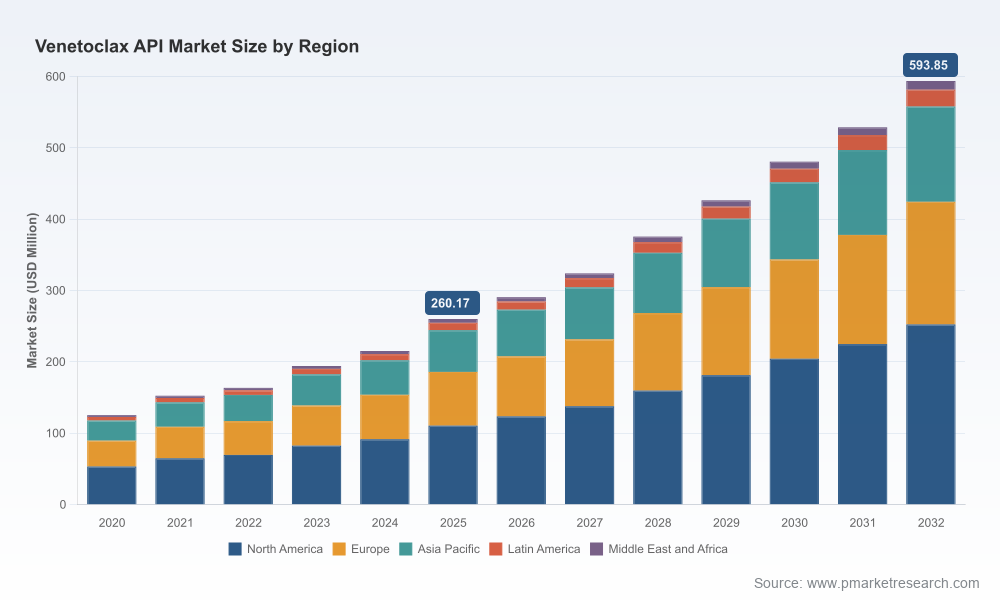

PW Consulting’s latest market study on the Worldwide Venetoclax API market positions this sector as one of the faster-growing specialized oncology API segments. The global market has more than doubled in size since 2020, reaching approximately USD 260.17 Million in our 2025 base year, and our scenario-driven forecasts point to continued expansion through the 2026–2032 outlook period, achieving roughly USD 593.85 Million by 2032 at a compound annual growth rate (CAGR) of 12.51% for the forecast window. This trajectory reflects a confluence of late-stage branded dynamics, accelerating generic readiness among contract manufacturers, and evolving treatment adoption curves in hematologic oncology.

Worldwide Venetoclax API Market

This press release highlights the strategic value of the full report for corporate planning cycles in 2026. Think of this as the executive trailer: we surface high-conviction trends, risks and playbooks that matter for procurement, manufacturing investments and partner selection—while directing decision-makers to the full report for granular segmentation, pricing scenarios and operational tools.

Worldwide Venetoclax API Market

Timing and market access: The interplay between intellectual property timelines and commercial settlements has created a narrow window in which API suppliers and finished-dose manufacturers must position capacity, secure intermediates and lock in offtake agreements. Early movers who align capacity with realistic regulatory milestones can capture outsized share as branded-to-generic transitions accelerate.

Worldwide Venetoclax API Market

Concentration and supplier economics: The market exhibits significant concentration at the top. The top three API suppliers account for roughly two-thirds of the market, and the top five capture an even higher share—providing scale advantages to incumbents while signaling opportunity and barriers for new entrants. Strategic buyers should model counterparty concentration when stress-testing their supply strategies.

High-margin, high-complexity chemistry: Venetoclax synthesis requires specialized heterocyclic intermediates and multi-step processes that drive capital intensity and per-batch cost in small-scale production. These technical characteristics sustain a premium for validated, regulatory-compliant suppliers and raise the value of DMF/CEP filings and FDA-validated manufacturing footprints.

Regulatory and IP signals: An important patent timeline anchors multiple commercial scenarios. While corporate settlements and litigation timelines have created openings for potential market entry prior to some patent expiries, composition-of-matter protections and pediatric exclusivities remain determinative for the magnitude and pace of generic roll-out. Decision-makers must therefore layer legal scenario analysis on top of capacity planning.

Concentration of manufacturing capacity: A majority of API capacity is produced by manufacturers in South Asia and East Asia. This geographic concentration increases exposure to oversight from importing regulators and to localized operational disruptions; import alerts or facility-level compliance issues can ripple rapidly through global supply chains.

Intermediates and input constraints: The supply of critical indole and pyrazole intermediates remains a chokepoint in the value chain. High complexity and limited multi-sourcing options push lead times and create discontinuity risk, especially for players without backward integration or secured long-term contracts.

Commercial dynamics between branded and generic channels: The branded therapy’s unit economics continue to underpin a sizeable commercial market for clinicians and payers. That pricing environment, coupled with anticipated generic introductions, frames two distinct demand waves for API: near-term demand from finished-dose suppliers preparing for market entry, and mid-term demand shifts driven by reimbursement and formulary changes.

Our competitive analysis concentrates on suppliers that have demonstrable global supply capabilities, regulatory filings and manufacturing footprints. Key findings about representative players:

MSN Laboratories Pvt. Ltd. — A Hyderabad-based player that has invested in high-purity Venetoclax API production and holds multiple regulatory filings with major authorities. Their posture suggests a readiness to scale for generic supply when commercial windows open; they are also a focal point in recent IP settlement activity that market participants must account for.

Hetero Drugs Ltd. — Also headquartered in Hyderabad, Hetero’s strengths include CEP certification and commercial-scale supply relationships with finished-dose manufacturers. Their profile underscores the value of European pharmacopeial conformity for global finished-dose customers.

Aurobindo Pharma Ltd. — With US FDA-approved facilities and an export-oriented oncology API strategy, Aurobindo’s capabilities illustrate how capacity and audited quality systems can unlock large-volume contracts with western finished-dose customers.

Senova Technology Co., Ltd. — A Tianjin-based manufacturer that emphasizes strict GMP compliance and regulatory filings. Senova’s presence highlights the competitive axis of Chinese manufacturers in supplying technically demanding oncology APIs for global markets.

Collectively, these firms exemplify the dominant model in this market: technically capable, regulatory-filed manufacturers concentrated in cost-competitive regions. The market’s top tier offers scale and regulatory confidence, while a longer tail of smaller firms provides niche capacity—creating a bifurcated supplier landscape that informs procurement strategy and M&A interest.

Patents and settlements: Several settlements and litigation outcomes have signaled earlier-than-expected generic moves in narrowly defined channels; however, composition-of-matter patent and pediatric exclusivities will continue to shape broad-market generic launch timelines. Financial planners and sourcing teams should implement weighted scenarios that combine settlement-driven early entry and full patent expiry pathways.

Import compliance and audits: Import alerts and facility audits can materially affect trade flows and the viability of supply contracts. Companies should augment supplier evaluation with historical compliance tracking and contingency capacity modeling.

Procurement and contracting: Negotiate staged offtakes and flex clauses tied to regulatory milestones rather than fixed-volume commitments. Include audit rights, secondary-source triggers and price reset mechanisms that reflect the fast-changing branded-to-generic economics.

Capacity and capital allocation: For API manufacturers, prioritize investments that reduce dependence on single-source intermediates and that rationalize batch scale for economies of scale. For finished-dose players, weigh toll-manufacturing vs. in-house API integration by modeling time-to-market under alternate IP scenarios.

M&A and partnerships: The concentration metrics and technical entry barriers favor inorganic routes for rapid capability acquisition. Target assets with validated regulatory filings (DMFs/CEPs), audited facilities and secured intermediates, and structure deals to preserve optionality across branded and generic timelines.

Risk management: Build multi-layer contingency plans that include buffer inventories of critical intermediates, second-source qualified suppliers, and rapid switching playbooks that can be executed within regulatory constraints.

Commercial positioning: Payers and finished-dose manufacturers should prepare differentiated market access strategies for branded versus generic pathways—using formulary intelligence to forecast realized pricing and demand migration curves for the forecast period.

The full Worldwide Venetoclax API Market report was designed as a decision-support toolkit for 2026 planning cycles. It contains:

Top-down and bottom-up market sizing with scenario bands that reconcile historical consumption, clinical adoption and anticipated generic entries across the 2026–2032 forecast horizon.

Supply chain heatmaps that identify single-source intermediates, regional concentration points and regulatory risk nodes—accompanied by supplier scorecards and an audit checklist for procurement teams.

Commercial scenario models tying IP timelines, reimbursement dynamics and competitive launches to plausible price and volume outcomes—deployed in downloadable spreadsheets for client-specific sensitivity testing.

Regulatory and DMF/CEP tracker: a continuously updated registry of public filings, facility certifications and known audit actions, enabling legal and regulatory teams to time compliance and market-entry actions.

Manufacturing cost and margin models that isolate the drivers of per-kilogram economics and identify where scale or process innovation yields the biggest leverage.

M&A and partnership playbook: templated deal structures, earn-out mechanisms keyed to regulatory milestones, and integration checklists oriented to rapid capacity absorption.

Operational leaders: Execute supplier qualification sprints for at least two alternate API sources and secure critical intermediate supply agreements with dual-sourcing clauses.

Commercial leaders: Update pricing and access models to reflect potential generic volume ramps and prepare segmented launch plans for regions where regulatory headroom is greatest.

Strategy and corporate development: Fast-track target screens for M&A candidates that hold DMFs/CEPs and validated facilities, and run rapid integration stress tests to estimate time-to-revenue under conservative regulatory timelines.

The Venetoclax API market represents a technically demanding, highly concentrated, and strategically time-sensitive opportunity for suppliers, finished-dose manufacturers and investors. With a base-year market size of approximately USD 260.17 Million (2025) and a forecast path to roughly USD 593.85 Million by 2032 at a 12.51% CAGR (2026–2032), the choices organizations make in 2026 about capacity, contracts and regulatory positioning will disproportionately determine their outcomes over the next six years.

PW Consulting’s full report equips leaders with the granular segmentation, supplier-level dossiers, regulatory timelines and scenario models needed to move from strategic intent to executable plans. For executives who must balance speed, compliance and capital efficiency in 2026, the report is designed to shorten time-to-decision and to reduce downside from mis-timed investments.

This release is a strategic preview. The full Worldwide Venetoclax API Market report includes the granular regional and application splits, supplier scorecards with filings and facility details, downloadable financial models and a step-by-step implementation playbook. Contact PW Consulting or visit our report page to access the complete intelligence package and data workbooks that enable 2026-ready decision-making.

For detailed analysis of this topic, please visit the official page:Worldwide Venetoclax API Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com