Panchit: The Ultimate Bhartiya Bharat social media app for Modern Indians

Technology |

2026-06-03 05:06:25

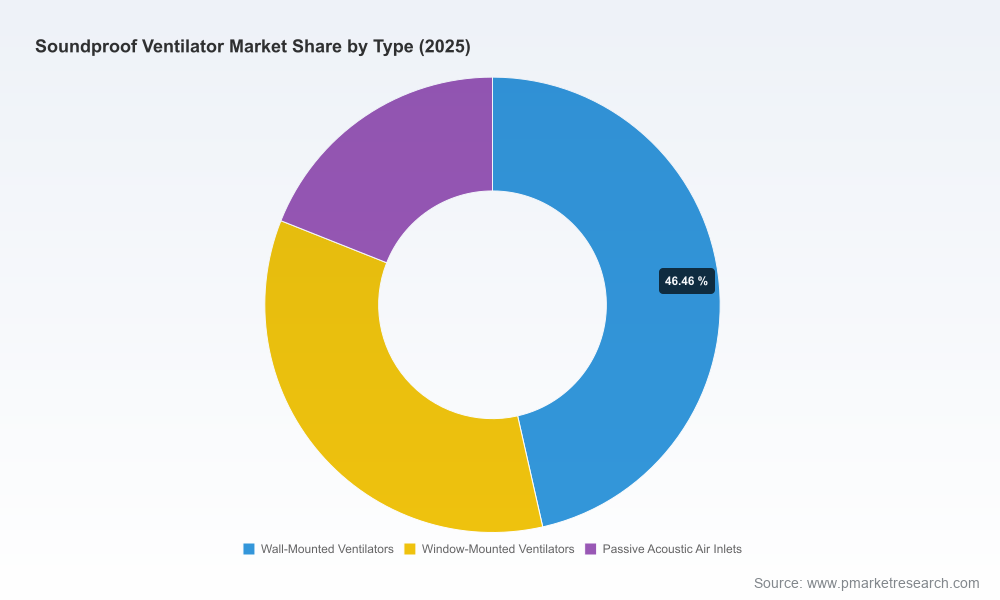

As noise-aware building design and stricter ventilation standards converge, the global soundproof ventilator market has entered a sustained growth phase. PW Consulting’s new market study — anchored on a 2025 base year, covering historical performance from 2020–2025 and projecting through 2026–2032 — quantifies this transformation and translates it into actionable strategy. The market rose materially over the past five years and is forecast to continue expanding at a compound annual growth rate (CAGR) of 6.18% over the forecast horizon. By isolating demand drivers, regulatory inflection points and supplier economics, the study is designed to inform capital allocation, product roadmaps, and channel strategies in 2026 and beyond.

Worldwide Soundproof Ventilator Market

Decision-makers face two concurrent dynamics: rising baseline demand as urbanization and retrofit cycles accelerate, and heightened technical thresholds driven by acoustic and energy-efficiency regulation. PW Consulting’s topline market model documents steady growth from the early 2020s into 2025 and projects continued expansion through 2032. This trajectory means that 2026 is not merely another year of incremental sales — it is a pivotal planning window in which investments in R&D, manufacturing flexibility, and compliance-ready product lines will compound value over the entire forecast period.

Worldwide Soundproof Ventilator Market

Our study translates market dynamics into a practical operational checklist for 2026 decision cycles:

Worldwide Soundproof Ventilator Market

The competitive picture is best described as moderately concentrated: the top three firms account for roughly one-third of market revenue, while the top five approach just under half. That structure creates both entry opportunities for focused innovators and sustainment challenges for incumbents facing margin pressure and technical parity.

Strengths: Deep specialization in decentralized soundproof ventilation with models offering high sound insulation and options with and without heat recovery. Market positioning benefits from strong brand recognition in residential retrofits and new builds where decentralized solutions are preferred.

Strengths: Broad portfolio of wall-mounted and window-mounted sound-absorbing ventilators with integrated filtration and CO₂ regulation. Competitive edge is in product breadth and the ability to address noise-polluted urban use cases through whisper-quiet designs.

Strengths: Technical leadership in both passive and active decentralized units designed for full compliance with stringent acoustic standards. Hybrid concepts and compliance orientation make Ventomaxx a go-to for projects demanding DIN-level performance.

Strengths: Specialization in acoustic trickle ventilators and slot vents with high laboratory-rated sound attenuation, tailored for window and door systems in noise-sensitive installations.

Strengths: Niche focus on trickle ventilators with humidity control and compact form factors; recognized for sound reduction performance in retrofit settings.

Strengths: Strong systems capability in acoustic silencers and low-noise fans suited to commercial and industrial integration — an advantage for large HVAC projects where acoustics are one of many system constraints.

Strengths: Leading provider of certified sound attenuators and ventilation components; competitive where certified performance and system-level integration are procurement requirements.

Strengths: Strength in acoustical louvers and sound curbs for air intake/exhaust applications, serving commercial and industrial markets with heavy-duty products and wide distribution.

Strengths: Materials-led value proposition, focusing on advanced acoustic vent materials and cost-competitive manufacturing for export-oriented players.

Two streams of signals are shaping near-term adoption:

The full study is intentionally practical and structured for executive use. Key deliverables include:

Note: To preserve the investigatory value and encourage direct engagement, this press briefing intentionally omits the granular segment-level breakdowns and proprietary company scorecards included in the full report. Those datasets and interactive models are available only through the PW Consulting distribution channel.

For corporate leaders, 2026 represents a strategic inflection: investments made this year in product architecture, supply chain resilience, and certification readiness will determine market share trajectories across the coming growth cycle. PW Consulting’s Worldwide Soundproof Ventilator Market report equips executives with the market sizing, scenario analyses, and operational playbooks necessary to make those choices with confidence. The release is intentionally a “trailer” of our full analysis: it demonstrates methodological rigor and practical relevance while reserving the proprietary segment-level intelligence and supplier scorecards for licensed clients and report purchasers.

Executives and strategy teams seeking the full dataset, company scorecards and interactive forecast models should consult the PW Consulting report page to arrange access. The complete report contains the granular segmentation and benchmarking data required for procurement specifications, capital budgeting and M&A diligence in 2026.

For detailed analysis of this topic, please visit the official page:Worldwide Soundproof Ventilator Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com