Holographic Optical Component Market Expands with Rising Demand for Advanced Photonics and Imaging Technologies

Film |

2026-06-18 07:51:25

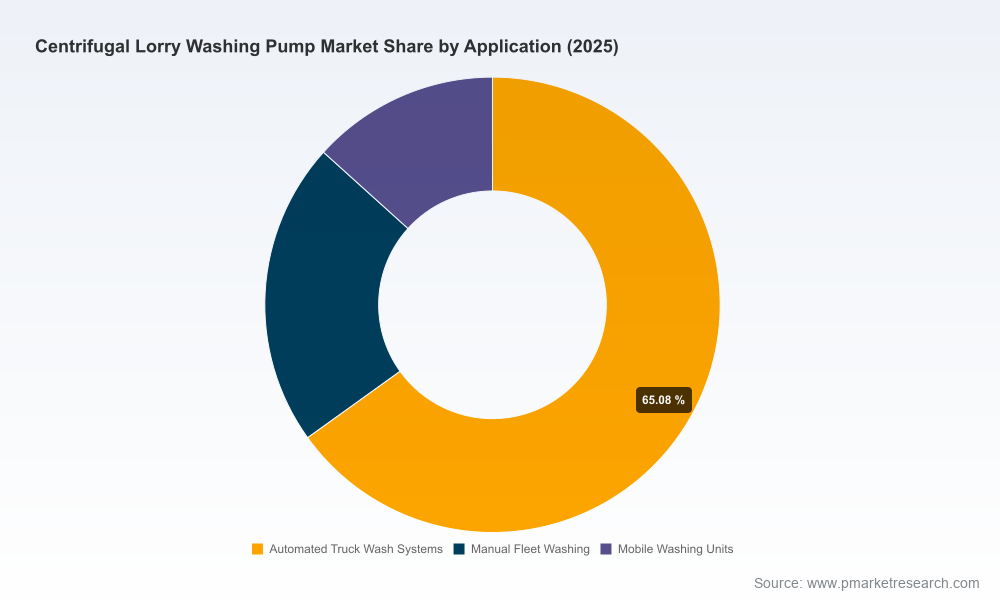

PW Consulting’s latest market study on the Worldwide Centrifugal Lorry Washing Pump Market synthesizes five years of historical performance (2020–2025) and delivers a practical seven‑year forecast (2026–2032). At a high level, the industry is on a steady growth trajectory: the market base stood at USD 442.5 Million in 2025 and is projected to expand to roughly USD 626.8 Million by 2032, reflecting a compound annual growth rate (CAGR) of 5.14% across the forecast horizon. For executives planning product roadmaps, procurement cycles, M&A activity, or technology investments in 2026, the report focuses on actionable insights and deployment-ready scenarios rather than abstract projections.

Worldwide Centrifugal Lorry Washing Pump Market

Regulatory pressure and water‑stewardship are reshaping buyer requirements. Modern vehicle wash systems are increasingly evaluated not only on cleaning performance but on their ability to reclaim and treat wash water. Leading systems demonstrate dramatic water savings through filtration and recycling, forcing pump suppliers to factor compatibility with closed‑loop water treatment into product design and go‑to‑market propositions.

Worldwide Centrifugal Lorry Washing Pump Market

Energy efficiency mandates and operating‑cost scrutiny are accelerating the adoption of Variable Frequency Drives (VFDs). In field and plant deployments, VFD‑equipped pump systems enable demand‑driven operation and, under many practical configurations, deliver payback periods often quoted at under a year — turning energy management into a near‑term commercial lever.

Worldwide Centrifugal Lorry Washing Pump Market

Labor cost inflation and workforce constraints are driving automation across commercial vehicle washing. OEMs and fleet operators increasingly prioritize touch‑free or gantry‑based systems; pumps that support modular automation, integrated sensing, and predictive maintenance win faster acceptance.

Material selection is a recurring procurement constraint: stainless steels (e.g., 304/316) and high‑performance thermoplastics remain the core materials for corrosion and abrasion resistance when handling chemically treated wash water and road salts. Supply‑chain and raw‑material swings therefore have immediate product and warranty implications.

The PW Consulting study is explicitly constructed as a decision‑support toolkit for 2026 initiatives. Key deliverables include:

Market sizing and validated forecast models (2020–2032) with scenario layers (conservative, baseline, accelerated) and sensitivity levers to stress‑test investment cases.

Buyer segmentation and purchasing‑journey mapping that reveal where specification decisions are made (OEMs vs. systems integrators vs. end‑fleets), what triggers procurement cycles, and how service contracts influence lifetime value.

Technology adoption curves for single‑stage versus multistage centrifugal architectures, and a practical VFD adoption model that quantifies payback under a range of duty cycles.

Supply‑chain risk maps and raw‑material cost exposure analyses (stainless steel and thermoplastics), including mitigation playbooks for procurement and inventory strategies.

Competitive vendor scorecards based on product breadth, service network, pricing transparency, and aftermarket capabilities — structured to support vendor shortlists without revealing confidential appendices in this press summary.

Implementation checklists and CapEx/Opex calculators that allow procurement and operations teams to turn strategic choices into tangible 12–24 month roadmaps.

The market is neither a pure commodity nor a tightly consolidated oligopoly. Top vendors combine global engineering footprints with regional specialists that compete on materials, service, and integration capabilities. PW Consulting’s analysis highlights a few representative provider archetypes and their strategic positioning:

Cat Pumps (Minneapolis, USA) — a leader for high‑pressure cleaning solutions, offering rugged pump platforms operating in the 1,000–2,000 PSI range with flow options and VFD compatibility. Their emphasis on energy‑efficient central systems targets automatic and self‑serve truck wash configurations where serviceability and uptime matter.

MP Pumps (Detroit, USA) — focused on centrifugal and self‑priming designs with corrosion‑resistant materials. Product durability in chemically harsh wash environments positions them well for fleet maintenance depots and vehicle service centers where reliability reduces operational disruption.

Pacer Pumps (USA) — builds thermoplastic centrifugal pumps that are lightweight and highly resistant to corrosion and abrasion. These products are attractive for mobile and chemically aggressive applications where total cost of ownership (TCO) balances capital and replacement cycles.

Ampco Pumps (Wisconsin, USA) — offers centrifugal ranges explicitly engineered for semi‑truck and heavy‑duty wash stations, including wastewater and gray‑water handling series. Recent product introductions signal an emphasis on capacity and robustness for industrial‑scale operations.

Xylem / Goulds Water Technology (New York, USA) and Grundfos (Denmark) — global OEMs providing stainless steel end‑suction and multistage pumps, booster solutions, and circulation architectures suitable for integrated wash systems that demand certified components and global service footprints.

Kärcher (Germany) — a systems integrator whose commercial truck‑wash solutions combine pumps, high‑pressure cleaning modules, and integrated water treatment. Their bundled approach represents the competitive threat that pump‑only manufacturers must address through partnerships or extended service offerings.

Recent industry activity — trade show participation and product launches by several vendors — underscores a near‑term push into channel development and specification influence. Market concentration is moderate: the leading three and five suppliers together command meaningful shares of industry aftermarket and original‑equipment specification lists, leaving room for regional specialists and new entrants that can exploit service, materials, or digital differentiation.

OEMs & product managers: Prioritize modular pump platforms that support both single‑ and multi‑stage configurations, VFD integration, and material variants (stainless vs. thermoplastic). Lock in supplier agreements that include spare parts lead‑time clauses and lifecycle pricing to protect gross margins against raw material volatility.

Systems integrators & wash operators: Treat water treatment compatibility as a minimum spec. Negotiate bundled service SLAs and remote‑monitoring agreements that shift value from one‑time sales to recurring revenue models. Pilot VFD retrofits in high‑utilization sites to validate ROI with live data before scaling.

Procurement & supply‑chain leaders: Build dual‑sourcing pathways for critical materials and consider consignment stocking for high‑turn spares. Use the report’s CapEx/Opex calculators to compare lifecycle costs across material and drive configurations rather than relying on purchase price alone.

Private equity & corporate development teams: Look for tuck‑in targets that add service density (field technicians, rapid‑exchange programs) or niche product capabilities (e.g., thermoplastic expertise or integrated water‑recovery modules). The combination of product and service creates defensible recurring revenue streams.

Our research recommends building three core scenarios into 2026 planning cycles: a conservative scenario where efficiency upgrades are incremental and fleet spend is delayed; a baseline case aligned to the report’s central forecast and efficiency adoption assumptions; and an aggressive adoption scenario that assumes rapid roll‑outs of automated, recycled‑water systems across large fleet operators. Each scenario materially changes spare‑parts demand, service economics, and supplier bargaining power — and the full report includes the underlying sensitivity matrices needed to quantify these shifts.

Custom vendor due diligence and scorecarding to validate technology claims (VFD savings, materials durability, field reliability).

Commercial‑model optimization (pricing, aftermarket contracts, P&L impact) and integration roadmaps for pump vendors seeking to move up the value chain into systems and services.

Supply‑chain resilience planning, including raw‑material hedging strategies and regional sourcing blueprints.

M&A target screening and diligence tailored to add‑on service networks, materials expertise, or water‑treatment capabilities.

This release highlights the strategic takeaways from PW Consulting’s full market study and outlines the near‑term actions that materially affect competitiveness in 2026. The detailed regional and application breakdowns, vendor scorecards, Excel‑based CapEx/Opex models, and proprietary datasets that power our forecasts are intentionally withheld from this summary to protect client value. For access to the complete report, bespoke scenario builds, or to commission a tailored advisory engagement, please contact your PW Consulting representative or visit our reports page to request the full dataset and executive toolkit.

For detailed analysis of this topic, please visit the official page:Worldwide Centrifugal Lorry Washing Pump Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com