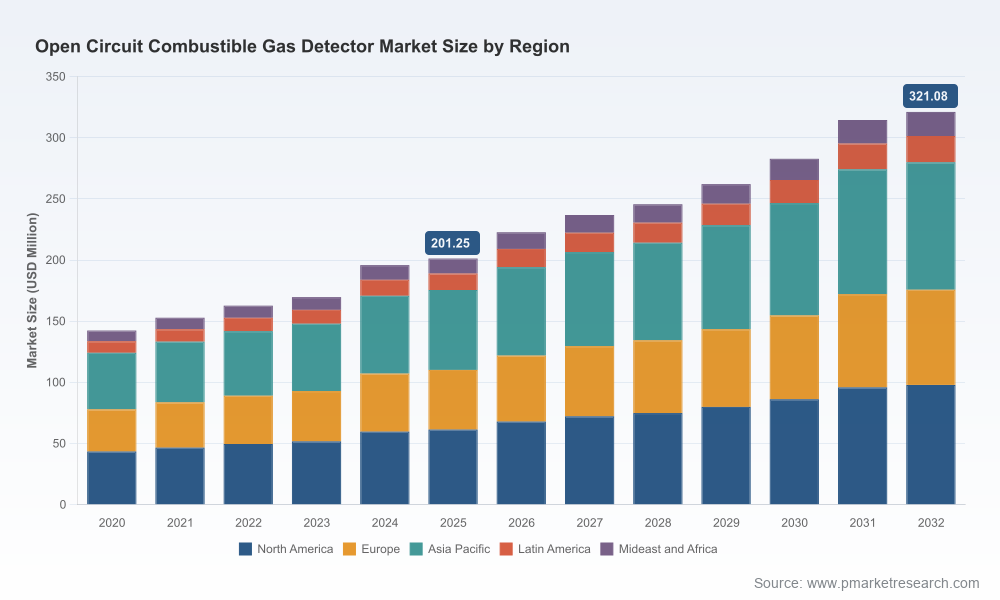

PW Consulting: Open Circuit Combustible Gas Detector Market valued at USD 201.25 Million in 2025, forecast to hit USD 321.08 Million by 2032 at a 6.85% CAGR

Other |

2026-07-02 05:48:51

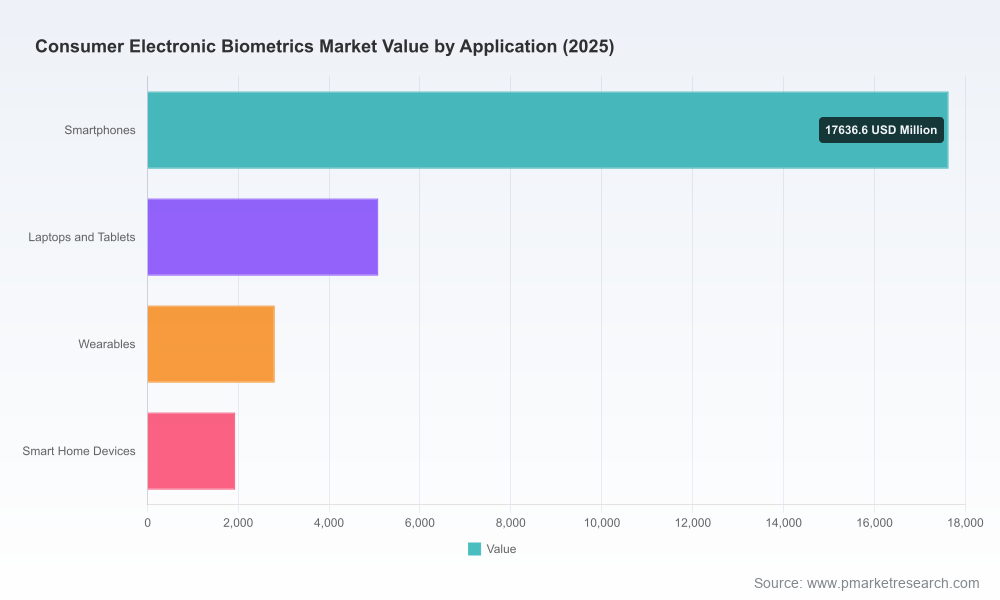

PW Consulting’s latest market study, Worldwide Consumer Electronic Biometrics Market (Base year: 2025; Forecast: 2026–2032), provides enterprise leaders with the forward-looking intelligence required to make high-stakes product, supply-chain, and M&A decisions in 2026. The market has expanded rapidly from an estimated USD 13.4 billion in 2020 to roughly USD 27.5 billion in 2025. Our model projects continued acceleration into 2026 and beyond — the market is on course to exceed USD 32.0 billion in 2026 and approach more than USD 76.2 billion by 2032, reflecting a compound annual growth rate (CAGR) of 15.7% across the forecast horizon. This briefing outlines why 2026 is a strategic inflection point, how competitive dynamics are evolving, and the practical actions executives should prioritize this year.

Worldwide Consumer Electronic Biometrics Market

Convergence of hardware and ML: Improvements in miniaturized optics, sensor integration, and on-device AI are enabling higher-accuracy, lower-power biometric modalities in a wider range of consumer electronics. This technical momentum shifts competitive advantage toward players that can combine sensor IP with optimized on-device inference stacks.

Worldwide Consumer Electronic Biometrics Market

Standards and payments integration: Industry initiatives (for example, EMVCo’s Biometric on Card workstream) are maturing, creating near-term interoperability and certification paths that will unlock biometric-enabled payment and identity experiences. Companies that align early with emerging performance and security criteria will gain fast access to commercial rollouts.

Worldwide Consumer Electronic Biometrics Market

Supply-chain and geopolitical risk: Biometric sensor production remains concentrated around a narrow set of wafer and module suppliers. Recent export-control revisions affecting advanced ICs and AI model assets have already altered procurement timelines. Risk-aware sourcing, design redundancy, and long-term supplier commitments will be required to avoid costly disruptions.

Mass-market adoption continues: High-volume smartphone adoption of fingerprint sensors and expanding use-cases in wearables, notebooks, and smart-home devices create durable demand for modules and authentication services. Volume economics are therefore realistic for new entrants that achieve integration-readiness and certification.

Product roadmaps: Prioritize modality-agnostic architectures. Companies should design authentication frameworks that allow plug-and-play integration of multiple biometric modalities (fingerprint, facial, iris, voice/behavioral) to future-proof devices against rapid shifts in user preference and regulatory requirements.

Component sourcing and dual-sourcing: Establish multi-tiered supplier strategies for critical components (sensor chips, wafers, optics). Insist on traceable supply chains and qualified second-source partners to mitigate export-control and geopolitical concentration risks.

Standards and certification investment: Allocate budget and executive attention to participation in standards bodies and performance certification programs. Early conformance to EMVCo and industry biometric benchmarks will materially shorten time-to-revenue for payment and identity use cases.

M&A and ecosystem plays: Expect consolidation around vertically integrated capabilities — sensor IP, secure enclave integration, and robust middleware/SDK ecosystems. Strategic M&A can accelerate entry into adjacent use-cases (payment cards, wearables) or shore up access to manufacturing capacity.

Monetization models: Beyond hardware sales, monetize authentication through recurring services (continuous authentication, identity verification, fraud analytics) and platform licensing. Early pilots should validate both technical feasibility and willingness-to-pay among OEMs and platform partners.

The market is characterized by a mix of vertically integrated platform companies, specialized sensor vendors, and systems/integration providers. Competitive intensity is high, and the top vendors exert significant influence over technology roadmaps and ecosystem access.

Apple Inc. — Leverages deep vertical integration of proprietary biometric stacks (e.g., structured-light 3D facial systems and capacitive fingerprint integration). Apple’s control of hardware, OS, and secure enclaves creates a high barrier for others seeking equivalent security and UX parity in the premium segment.

Samsung Electronics — Deploys a broad set of sensor formats (including ultrasonic and in-display optical) across product tiers. Samsung’s advantage is platform breadth and manufacturing scale, enabling rapid iteration on sensor form-factor and system integration.

Qualcomm — Acts as an important enabler for Android OEMs through Snapdragon biometric platforms. Its role in delivering reference designs and IP licensing makes it a pivotal partner for chipset-level biometric capabilities.

Goodix, Synaptics, Fingerprint Cards, Egis, IDEX — These specialized vendors drive much of the sensor module innovation and cost optimization. Their competitiveness depends on sensor performance, integration support, and relationships with smartphone OEMs and module integrators.

IDEMIA, NEC, Suprema — Offer advanced software, algorithmic differentiation, and system-level offerings that map well to identity-anchored use cases, including secure authentication for payments and consumer access control.

Recent industry moves underline two adjacent phenomena: (1) continued product innovation in module form factors (for example, metalens-based or ultra-compact 3D fingerprint assemblies) that reduce BOM and integration friction; and (2) industry consolidation and strategic acquisition activity that aggregates biometric IP and system capabilities — illustrated by large-scale transactions and targeted product launches in early 2026. These developments are accelerating time-to-market for qualified solutions and shifting bargaining power in favor of suppliers that combine IP with scale.

Export-control compliance: Reassess sourcing and design assumptions in light of tightened controls on advanced computing ICs and certain AI assets. Map component supply-chains to jurisdictional risk and update contracts to include compliance covenants and contingency provisions.

Standards engagement: Obtain early certification readiness for payment and identity standards — not just as a compliance checkbox but as a commercial accelerator. Certification can be a market-access requirement for payment partnerships and some OEM channels.

Supply resilience: Prioritize long-lead procurement, strategic inventory buffers for wafers and packaged modules, and investment in multi-source qualification programs. Consider nearshoring or contract manufacturing arrangements where it reduces systemic risk.

Our research is designed to be a working tool for corporate strategy teams. Highlights of the deliverables include:

Proprietary market model (base year 2025, forecast 2026–2032) with scenario simulations and sensitivity analysis to test pricing, adoption velocity, and policy shock assumptions.

Vendor scorecards and go-to-market profiles mapping technology, IP posture, OEM relationships, and manufacturability readiness for all major suppliers and emerging challengers.

Supply-chain heatmaps identifying concentration risks at wafer, module, and assembly tiers, with recommended mitigation roadmaps for sourcing, inventory, and contract terms.

Practical playbooks for product teams — integration checklists, certification pathways, and SDK/secure-enclave templates to accelerate OEM acceptance.

M&A and partnership target lists with high-level valuations under multiple scenarios, including quick-screen diligence frameworks and integration risk assessments.

Regulatory tracker and compliance checklist tailored to payment, identity, and cross-border export-control regimes relevant to biometric components and models.

CEOs and board members: Use the market model to stress-test capital allocation decisions and validate strategic acquisitions or factory commitments under multiple geopolitical scenarios.

Product and engineering leaders: Adopt modality-agnostic design patterns and accelerate integration pilots that demonstrate compliance and performance against EMVCo and other emerging benchmarks.

Procurement and supply-chain teams: Implement multi-sourcing and supplier audit programs; secure long-lead components and negotiate export-compliance clauses.

Corporate development teams: Prioritize targets that close capability gaps (sensor IP, secure middleware, certification experience) rather than those that simply add revenue. Look for sellers with repeatable OEM relationships and proven manufacturing readiness.

This briefing communicates the strategic contours and the high-level financial trajectory of the consumer electronic biometrics market through 2032. In line with our “trailer” approach, detailed sub-segment allocations, granular regional splits, and customer-level forecasts are reserved for the full report and interactive dashboards. That deeper dataset contains the transaction-level intelligence, supplier-level pricing curves, and integration-level performance matrices that operational teams need to execute with confidence.

For executives preparing budgets, product roadmaps, or corporate-development plans in 2026, PW Consulting’s report offers a practical decision-engine: an analytically robust forecast, vendor-level diagnostics, and the actionable playbooks required to convert biometric opportunity into sustained revenue and defensible differentiation.

Contact PW Consulting to access the full Worldwide Consumer Electronic Biometrics Market report, the interactive forecast model, and advisory services tailored to your strategic priorities in 2026.

For detailed analysis of this topic, please visit the official page:Worldwide Consumer Electronic Biometrics Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com