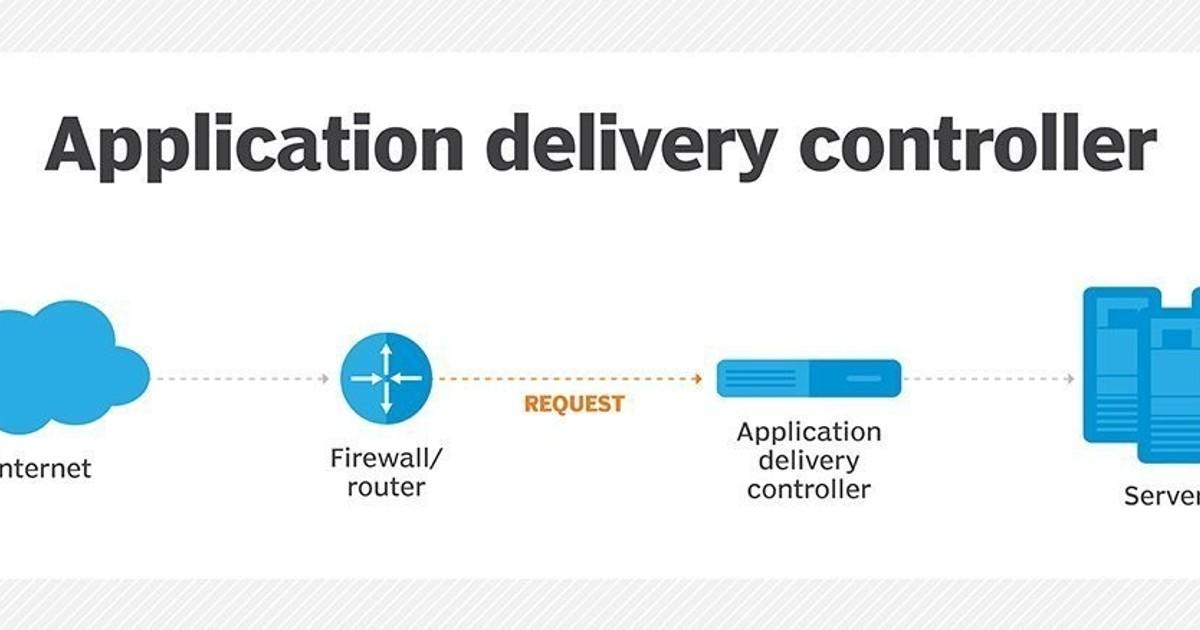

In-Depth Analysis of the Application Delivery Controller Market Amid Rising Application Complexity

Networking |

2026-01-05 08:53:13

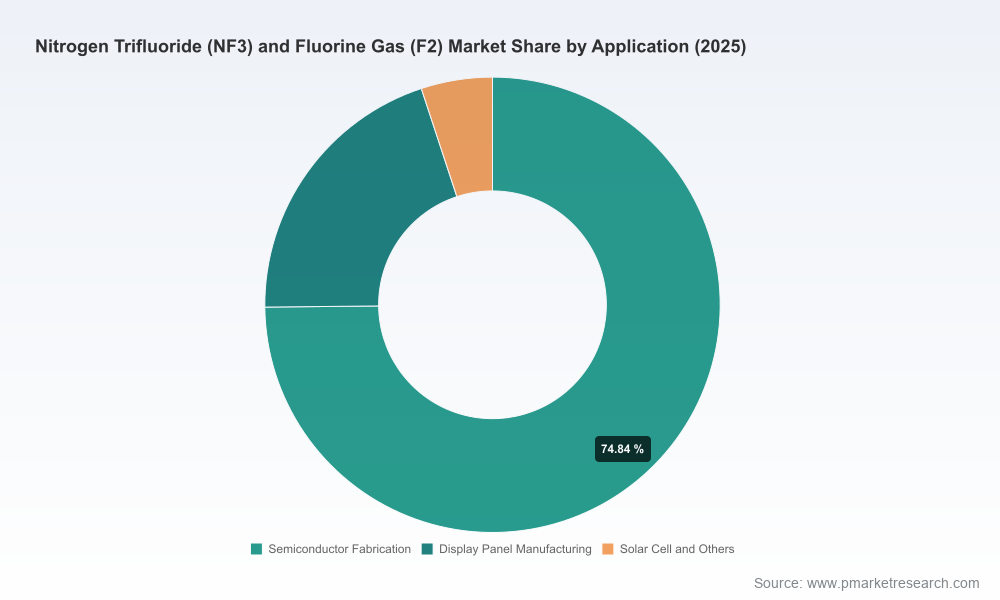

PW Consulting’s new market study on Nitrogen Trifluoride (NF3) and Fluorine Gas (F2) provides a focused, decision-ready perspective for corporate leaders planning capital allocation, sourcing, regulatory compliance, and M&A through 2026 and beyond. The market reached USD 1,520 Million (base year 2025) and is forecast to expand at a compound annual growth rate (CAGR) of 7.15% over our 2026–2032 forecast horizon, reaching approximately USD 2,465 Million by 2032. The market remains materially concentrated (top‑3 firms ≈68.4%; top‑5 ≈82.15%), which creates both stability and structural barriers that buyers, suppliers and investors must navigate.

Worldwide Nitrogen Trifluoride (NF3) and Fluorine Gas (F2) Market

Capex cycles in electronics and displays are aligning with technology transitions (next‑gen nodes and panel technologies), making 2026 a crossroads for capacity investment and long‑term offtake agreements.

Worldwide Nitrogen Trifluoride (NF3) and Fluorine Gas (F2) Market

Regulatory tightening in major markets and evolving export controls are creating new compliance costs and demand friction — decisions made in 2026 about local manufacturing, inventory policy and contractual safeguards will materially affect P&L through the next cycle.

Worldwide Nitrogen Trifluoride (NF3) and Fluorine Gas (F2) Market

Supply‑chain stressors (raw material volatility and specialized transport constraints) are compressing lead times and raising the cost of service; 2026 offers a window to redesign supplier networks before shortages become entrenched.

The NF3 and F2 market is on a steady growth trajectory: our bottom‑up modeling shows a mid‑single digit to high‑single digit CAGR (7.15%) driven by continued electronics manufacturing growth and incremental use in specialty chemical syntheses. At the same time, concentration metrics indicate a structurally consolidated supply base. That dynamic delivers reliable scale providers but also increases the strategic value of supply diversification and the bargaining power of incumbent producers.

Key structural dynamics to factor into 2026 planning include:

Demand stickiness from semiconductor etch and cleaning cycles and from display panel manufacturing, with secondary demand from solar and specialty chemicals.

Raw material and logistics sensitivities: recent supply disruptions pushed anhydrous hydrogen fluoride (AHF) pricing materially higher, while UN classification and handling requirements for F2 impose specialized transport and handling that elevate logistics costs by a low double‑digit percentage.

Regulatory and trade policy risks: chemical emissions reporting requirements and tightened export controls have already altered trade flows and supplier risk profiles in 2024–2025.

Market concentration is high and incumbents are actively shaping the next phase of the value chain. The report's corporate briefs triangulate public disclosures, site footprints and recent moves to create an actionable view of competitor intent.

Solvay (Belgium) — A global NF3 and F2 producer with manufacturing capacity across Europe and Asia. Recent product upgrades for high‑purity F2 signal a push into higher‑margin pharmaceutical and advanced fluorination markets. Strategic implication: incumbents are pursuing product differentiation beyond commodity supply.

Air Products (USA) — A major supplier to electronics, with expanded NF3 capacity in Taiwan to support semiconductor demand. Their capacity moves underscore the importance of proximity to fabs and the economics of localized supply partnerships.

Linde (Germany) — Offers NF3 and F2 with a global supply chain; recent certification updates illustrate investment in operational risk controls and compliance as a competitive advantage.

Kanto Denka Kogyo and Morita Chemical Industries (Japan) — Focused on ultra‑high purity grades for Japanese and regional customers; their specialization highlights opportunity for niche premium positioning.

Hyundai Steel (Green Gas) — Regional supplier with a vertical integration angle for display manufacturing customers in South Korea.

Pelchem (Peltzer Group) — Serves specialty and nuclear segments from South Africa, demonstrating that geographic diversification can sustain niche export opportunities.

Together, these players illustrate two clear competitive plays: (1) scale + proximity to electronics demand centers, and (2) technical differentiation via higher‑purity grades and compliance credentials. Both are relevant to buyers deciding whether to pursue short‑term spot sourcing, contract manufacturing, or strategic investments.

Regulatory compliance: Recent tightening in emissions reporting in major jurisdictions increases monitoring and disclosure obligations for both producers and users. This shifts some operational cost to OEMs and may necessitate supplier audits and revised indemnities in 2026 contracts.

Export controls and trade policy: Expanded export controls and related permit regimes in 2024 have already redirected portions of established trade flows; firms should model permit lead times into their mid‑term sourcing plans.

Logistics and handling: UN classification for F2 requires specialized cryogenic and pressure‑rated equipment, elevating both capex for logistics partners and unit transport costs — a persistent margin pressure point for low‑distance suppliers.

Raw material shocks: AHF supply interruptions have demonstrated how upstream commodity swings transmit quickly into production economics for NF3 and F2 manufacturers.

This study is intentionally structured as a strategic playbook for 2026 decisions. Key deliverables include:

Transparent forecasting engine with downside, base and upside scenarios to stress‑test capex and procurement plans against demand and policy shocks.

Supplier heat‑maps and capability matrices that combine capacity, compliance standing, and geographic exposure to identify concentration risk and diversification paths.

Contract and commercial templates: recommended clauses for long‑term offtake agreements, force majeure, price pass‑throughs linked to AHF indices, and export/compliance warranties.

Regulatory impact models showing cost and timeline sensitivity to emissions reporting and export control changes, with mitigation levers and expected P&L impacts under different policy outcomes.

M&A and JV decision framework — playbooks for target screening, valuation adjustments for regulatory exposure, and integration checklists for technical assets (e.g., cryogenic handling, high‑purity packaging).

Commercial go‑to‑market options for specialty players: premiumization paths, co‑development with OEMs, and service models (managed inventories/consignment) to capture more value.

To honor the “trailer” principle: while we present the forecasting skeleton and strategic implications here, the report retains detailed regional and application‑level splits, supplier financials and full numerical scenarios behind an interactive data pack — access to the source page unlocks that proprietary dataset.

Secure dual‑track sourcing for at‑risk chemistries. Implement a primary/secondary supplier structure; negotiate conditional capacity reservations with performance incentives to protect critical nodes during demand peaks.

Re‑engineer inventory policy into a hybrid model. Shift from thin‑inventory to strategic buffer holdings for critical inputs and finished gas volumes, calibrated by scenario stress tests in the report’s forecast engine.

Embed regulatory clauses and certification checks into procurement. Make supplier REACH compliance, export license readiness, and safety certifications explicit gating criteria for approvals and pricing arrangements.

Assess selective verticalization. For system integrators and larger OEMs, evaluate co‑located or captive supply as a hedge against export controls and logistics premiums; model break‑even under different demand trajectories.

Pursue differentiation via higher‑purity grades and service offerings. For mid‑tier producers, invest selectively in purification and pack‑out capabilities to capture premium niches with less price sensitivity.

Prepare contingency M&A playbooks. Target transactions that add regional hub capabilities, specialized purification assets, or compliance‑ready operations to accelerate market entry without long lead‑time capex.

Executives should treat the report as both a forecasting tool and a tactical manual. Use the scenarios to size and time capital commitments; deploy the supplier heat‑maps to renegotiate or diversify contracts; and iterate procurement clauses with legal teams using the contract templates we provide. The report is structured so that commercial, procurement, regulatory and corporate development teams can extract role‑specific action items without re‑running core analysis.

If your team needs an accelerated briefing, PW Consulting offers tailored executive workshops that translate the report’s scenarios into bespoke decision matrices and implementation roadmaps for supplier negotiations, capex sequencing and M&A prioritization.

The synopsis above highlights the strategic contours that will matter most in 2026. For the full dataset, granular regional and application breakouts, supplier financial trenches and downloadable modeling tools — including the interactive scenario engine and procurement templates — please visit the report landing page to request access and licensing options. PW Consulting’s analysts are available to walk through the data and co‑develop the 90‑day action plan best suited to your organization’s risk appetite and growth objectives.

For detailed analysis of this topic, please visit the official page:Worldwide Nitrogen Trifluoride (NF3) and Fluorine Gas (F2) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com