Worldwide Hip Orthosis Market: Strategic Imperatives for 2026 — PW Consulting Insights

PW Consulting’s latest market study on the Worldwide Hip Orthosis Market (base year 2025, historical window 2020–2025, forecast 2026–2032) delivers a focused, decision-ready view for manufacturers, payors, distributors and investors planning execution in 2026. Grounded in primary interviews, claims-level reimbursement mapping and a transparent forecasting methodology, the report synthesizes market trajectories and competitive dynamics while preserving the granular intelligence that subscribers need to act—this release is a preview crafted to show the depth of our analysis while pointing readers to the full report for the underlying segmentation and proprietary tables.

Worldwide Hip Orthosis Market

Market snapshot — what the headline numbers say

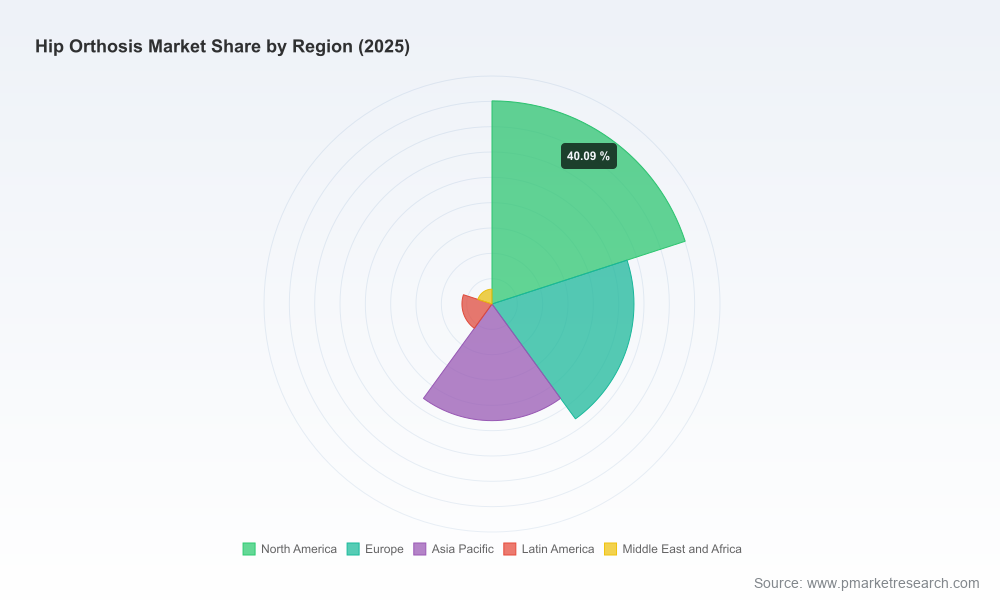

- Market scale and trajectory: the hip orthosis market reached USD 542.4 Million in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 5.25% through our forecast period, reflecting steady recovery and expansion across care pathways.

- Forward momentum: our model forecasts durable expansion to a materially larger market by 2032, driven by a blend of post-operative care demand, chronic disease management, and incremental adoption of prefabricated and adjustable solutions.

- Concentration: the market shows a measurable degree of consolidation—our concentration metrics (CR3 ≈ 38.5%, CR5 ≈ 52.4%) indicate that a small set of incumbent manufacturers capture a meaningful share, while a healthy mid-tier remains available for challengers and niche specialists.

Why this report matters for 2026 decision-making

- Prioritize capital: Our scenario-based valuation and volume-price models identify which levers—R&D vs. sales coverage vs. channel partnerships—deliver the highest ROI under 2026 reimbursement realities.

- Navigate reimbursement complexity: Practical guidance on HCPCS mapping, PDAC considerations and procurement tactics helps commercial teams convert clinical value into reimbursable codes and predictable revenue.

- Design a product roadmap that wins: We translate clinical needs and payer sensitivities into feature-priority lists and development sprints to accelerate adoption in early-adopter sites.

- De-risk M&A and alliances: The report’s integration playbooks and diligence checklists help acquirers and strategic partners quantify synergies without overpaying for duplicative manufacturing or distribution footprints.

Dynamics shaping the market

Our analysis identifies a convergent set of forces that will determine winners and losers in 2026:

Worldwide Hip Orthosis Market

- Clinical demand drivers: Increasing hip preservation procedures, refinements in arthroscopy, and a growing body of outpatient post-operative pathways continue to underpin prosthetic and orthotic support needs. At the same time, chronic degenerative conditions are increasing long-term orthotic use, shifting product mixes toward comfort- and compliance-focused designs.

- Regulatory and reimbursement environment: The HCPCS coding framework remains the operational backbone for U.S. commercial access. Notably, HCPCS code L1686 explicitly describes a prefabricated postoperative hip abduction orthosis and is PDAC-approved for that use—this is a practical lever that manufacturers must incorporate into product labeling and clinical evidence generation. More broadly, hip orthoses continue to be managed within the L1600–L1690 HCPCS range, which covers a variety of abduction-control and adjustable designs. Our 2025 regulatory scan found no new discrete hip-orthosis codes finalized beyond current mappings, but ongoing public discussions leave the door open for future off-the-shelf coding refinements.

- Procurement and pricing pressure: Payer scrutiny of orthotic cost-effectiveness is increasing. The ability to demonstrate measurable outcomes—shorter recovery times, reduced readmissions, improved function scores—translates into stronger contract terms and preferred-lists access.

- Supply chain and manufacturing shifts: Demand is rising for modular prefabricated solutions that reduce fitting time and logistics costs. This creates pressure on legacy custom-manufacturing players to adapt or partner with prefabricated specialists and 3D-fitting technology providers.

Competitive landscape — how incumbents are positioned

The market’s leading firms blend clinical specialization, channel presence and manufacturing scale. Our competitive profiles assess product breadth, clinical evidence, distribution coverage and commercialization rigor.

Worldwide Hip Orthosis Market

- Össur (Reykjavik, Iceland | https://www.ossur.com) — Strong in load-redistribution and proprioceptive-support solutions. Their Unloader Hip and post-op support products are positioned around biomechanical optimization and user comfort, a strategy that targets osteoarthritis and early post-op rehabilitation.

- Ottobock (Duderstadt, Germany | https://www.ottobock.com) — Well-capitalized global player with solutions spanning abduction, dysplasia treatment and activity-support orthoses. Product design emphasizes ease-of-use and breathable materials—attributes that directly address adherence in outpatient settings.

- Orthomerica (Orlando, FL, USA | https://orthomerica.com) — Focuses on total-contact, postoperative dislocation-prevention designs. Their portfolio and custom-fit capability remain relevant for hospitals and high-acuity post-op protocols.

- Breg (Carlsbad, CA, USA | https://www.breg.com) — Patient-centric post-op bracing specialist; their T Scope and other post-operative braces emphasize simplicity and comfort, which supports stronger acceptance in bundled-payment and outpatient bundles.

- Becker Orthopedic, Thuasne, Restorative Care of America (RCAI), Fillauer and Aspen Medical Products — These mid-tier and specialist firms compete on prefabrication speed, cost-efficiency and niche clinical applications (e.g., pediatric dysplasia or trauma immobilization), offering acquisition targets or partnership opportunities for larger players seeking fill-in capabilities.

Our scorecards evaluate each firm across product innovation, clinical data depth, channel coverage and reimbursement readiness—insights that supply-side leaders use to calibrate partnership and M&A strategies.

What’s inside the full PW Consulting report (practical deliverables)

- Market sizing and forecast models (2020–2032) with transparent assumptions and sensitivity analyses tailored for board-level scenario planning.

- Channel and go-to-market playbooks for OEMs and distributors, including contract negotiation templates and tender-response checklists.

- Reimbursement navigator: HCPCS mapping matrix, PDAC guidance, and payer engagement playbook for converting clinical endpoints into covered line items.

- Competitive scorecards and supplier capability matrices, with acquisition target shortlists and integration-risk heatmaps.

- Clinical and product innovation benchmark: evidence requirements by clinical use case and a prioritized R&D roadmap aligned to near-term payer expectations.

- Operational readiness checklists for scaling prefabricated production, digital-fitting implementation and returns/repairs management.

Recommended strategic moves to consider in 2026

Based on our findings, we recommend that executive teams consider a combination of the following tactical moves, sequenced to deliver measurable impact within 12–18 months:

- Reimbursement-first product labeling: Align new product claims and clinical trials explicitly with HCPCS descriptors that drive coverage (e.g., mapping to existing abduction control codes and ensuring PDAC-friendly documentation).

- Clinical evidence play: Prioritize pragmatic trials and real-world evidence generation that show reduced recovery time, improved function, or lower total episode costs to strengthen payer negotiations.

- Channel-focused investments: For OEMs, selectively expand distribution in outpatient surgical hubs and orthopedic specialty networks where adoption velocity is highest; for distributors, deepen clinical training and fitting services to lock in loyalty.

- Modular-manufacturing partnerships: Seal partnerships or bolt-on acquisitions to acquire prefabrication capabilities, digital-fitting platforms, or rapid customization technologies aimed at reducing time-to-fit and returns.

- Pricing and contracting refresh: Move from list-price-based sales to outcome-value contracts in pilot markets—this accelerates uptake in bundled-payment environments and strengthens long-term pricing defensibility.

How to get the full intelligence

This briefing intentionally surfaces the strategic findings and the practical value of our work while withholding the granular regional, product-type and application-level splits that are the most commercially actionable elements of the report. Subscribers to the full PW Consulting Worldwide Hip Orthosis Market report receive access to the underlying datasets, interactive forecast models, detailed company profiles, and downloadable procurement and clinical engagement templates designed to be deployed in Q1–Q2 2026.

For Boards, corporate strategy teams, M&A advisors and commercial leaders preparing for 2026, the complete report provides the decision-support package you need: validated numbers, executable tactics, and the scenario tools to convert a predictable growth runway into measurable share gains. To explore subscription options and receive a sample executive summary, please contact PW Consulting through our corporate website.

For detailed analysis of this topic, please visit the official page:Worldwide Hip Orthosis Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com