PW Consulting: Vanilla Market to reach USD 5.81 Million by 2032, 5.69% CAGR

Other |

2026-07-12 08:30:08

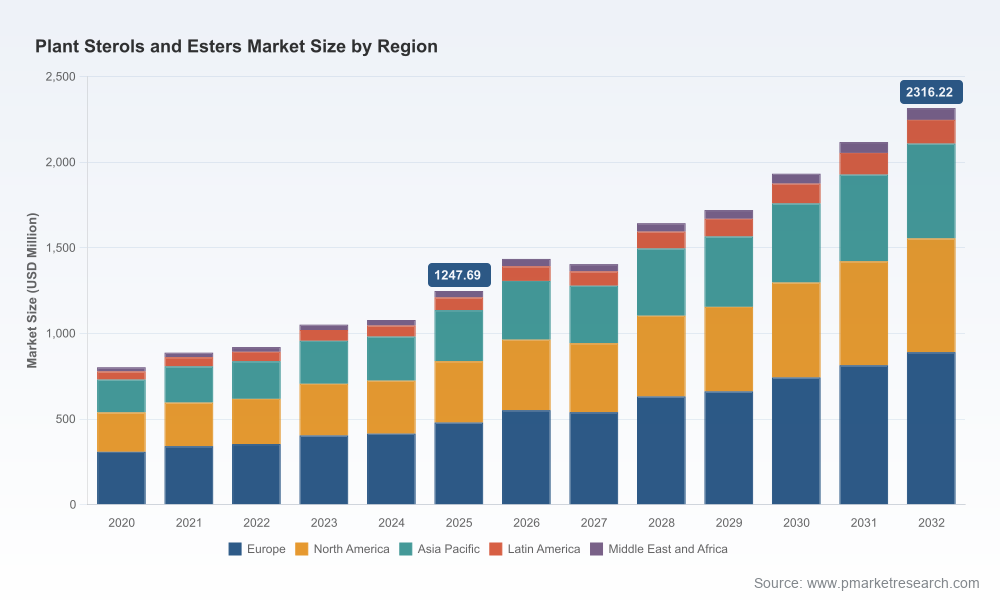

PW Consulting’s latest market study on Worldwide Plant Sterols and Esters provides a data-driven strategic playbook tailored for executive teams preparing for the critical planning horizon beginning in 2026. The study synthesizes a complete market system view — from demand drivers and raw-material dynamics to regulatory constraints and competitive positioning — and quantifies the commercial implications in a forward-looking model. At the aggregate level, the market reached roughly USD 1.25 billion in 2025 and is modeled to expand at a compound annual growth rate (CAGR) of 9.24% through the 2026–2032 forecast period, with top-line scenarios projecting a near-term doubling to just over USD 2.3 billion by 2032 under the base case. These headline figures frame the strategic urgency facing manufacturing, ingredient sourcing, and commercialization choices for 2026 and beyond.

Worldwide Plant Sterols and Esters Market

Three strategic imperatives emerge from our analysis and should shape boardroom conversations in 2026:

Worldwide Plant Sterols and Esters Market

Our proprietary market model uses 2025 as the base year and incorporates a detailed historical reconstruction from 2020–2025. The projected 9.24% CAGR over the 2026–2032 forecast period reflects the convergence of three support vectors: rising consumer interest in cardiovascular and metabolic wellness, broader fortification across food & beverage categories, and uptake in nutraceutical and pharmaceutical applications where sterol purity and regulatory compliance command premium valuations.

Worldwide Plant Sterols and Esters Market

For commercial teams, the model translates top-line growth into actionable revenue, margin, and cash-flow scenarios under multiple pricing and raw-material assumptions. This enables prioritized investment roadmaps (capex timing, scale, location) and contract strategies (fixed-price vs. pass-through, offtake terms) that preserve margin under downside commodity conditions.

Feedstock availability and pricing are the most immediate operational risks. Recent agricultural and trade developments have created a tougher procurement landscape: vegetable oil feedstocks experienced notable price pressure in late 2025 driven by supply disruptions, and trade policy shifts have increased duty costs for some cross-border flows. These cost dynamics materially affect manufacturers that rely on low-cost vegetable oil inputs.

Practical steps that the report recommends for 2026 include:

Regulatory constraints and guidance remain central to commercial positioning. Leading jurisdictions maintain explicit boundaries for allowable daily intakes and health claims; concurrently, regulatory agencies in major markets have reaffirmed acceptable use levels for plant sterol esters in conventional foods. For product teams, the implication is clear: claim architecture is both a compliance and a go-to-market instrument.

Our regulatory matrix in the report maps permissible claims, labeling requirements, and country-by-country enforcement tendencies. It also provides a tactical checklist for 2026 new-product launches and reformulations that seeks to maximize claim utility while minimizing regulatory friction.

The market exhibits moderate concentration: the largest three players account for a meaningful share of organized supply, and the top five consolidate the majority of formalized capacity. This concentration has practical implications for bargaining dynamics, pricing, and the design of commercial partnerships.

Key incumbent players analyzed in the report include major ingredient houses, specialty chemical suppliers, and regional manufacturers. Their strategic postures vary:

For corporate strategists, the recommended approach in 2026 is to combine selective capability investments (e.g., purification, formulation science) with go-to-market partnerships that leverage established distribution in target channels. M&A targets are likely to be transaction-light bolt-ons that add formulation expertise, specialized purification, or access to regulated markets, rather than broad capacity buys that risk overpaying into a cyclical commodity cycle.

Innovation is converging around three technical themes: bioavailability enhancement, sensory-neutral delivery matrices for mainstream foods, and high-purity extracts for regulated pharmaceuticals. The most valuable R&D investments are those that reduce dosage requirements through improved absorption or that enable incorporation into new matrices (e.g., fermented dairy analogs, shelf-stable beverage systems) without compromising organoleptic properties.

Our benchmarking work provides comparative metrics on formulation lift and incremental pricing power for enhanced-bioavailability claims — enabling product teams to calculate expected ROI on reformulation projects versus premium pricing strategies.

PW Consulting’s study is organized to support immediate 2026 planning and execution. Key deliverables include:

Selected market events illustrate the dynamics at play: a major ingredient supplier secured non-GMO certification to reinforce premium positioning; a leading brand extended its product family with improved-bioavailability variants; and a global processor expanded capacity to meet surging regional demand. These moves underscore two realities: brand-driven premiumization and the necessity for supply-side responsiveness. Our report includes case-level analysis on each of these developments and prescriptive guidance on how to counter or emulate them.

Executives should use the report as a short-to-medium-term decision support tool in three specific ways:

This briefing intentionally conveys the strategic contours and operational implications of our findings while withholding granular segment shares, regional revenue breakdowns, and detailed pricing tables — these are core report assets reserved for subscribers. The contained insights are designed to establish trust in our methodology and to stimulate high-value strategic conversations in 2026. For teams ready to translate these perspectives into executable plans, the full report provides all segment-level detail, downloadable models, and the granular tables necessary to operationalize the recommendations.

PW Consulting is available to support bespoke workshops that translate the report’s scenarios into board-ready investment cases, pricing playbooks, and supply-chain transition plans. For companies evaluating acquisition opportunities or negotiating supply contracts in 2026, we offer targeted diligence packages that apply the report’s model to live counterparty data.

Contact our industry team to request the full report, the underlying model, and advisory support options. In a market growing rapidly yet bounded by tight regulatory and feedstock realities, informed, timely decision-making will be the decisive competitive advantage in 2026.

For detailed analysis of this topic, please visit the official page:Worldwide Plant Sterols and Esters Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com